Strong mergers and acquisitions (M&A) activity over the past two years has stimulated demand for insurance covering transactional risks.

In its July report, Transactional Risk 2017: Year in Review, insurance broker Marsh reveals it placed 28 per cent more transactional risk policies in 2017, compared with 2016, driven by a rise in M&A and an increase in the size of deals.

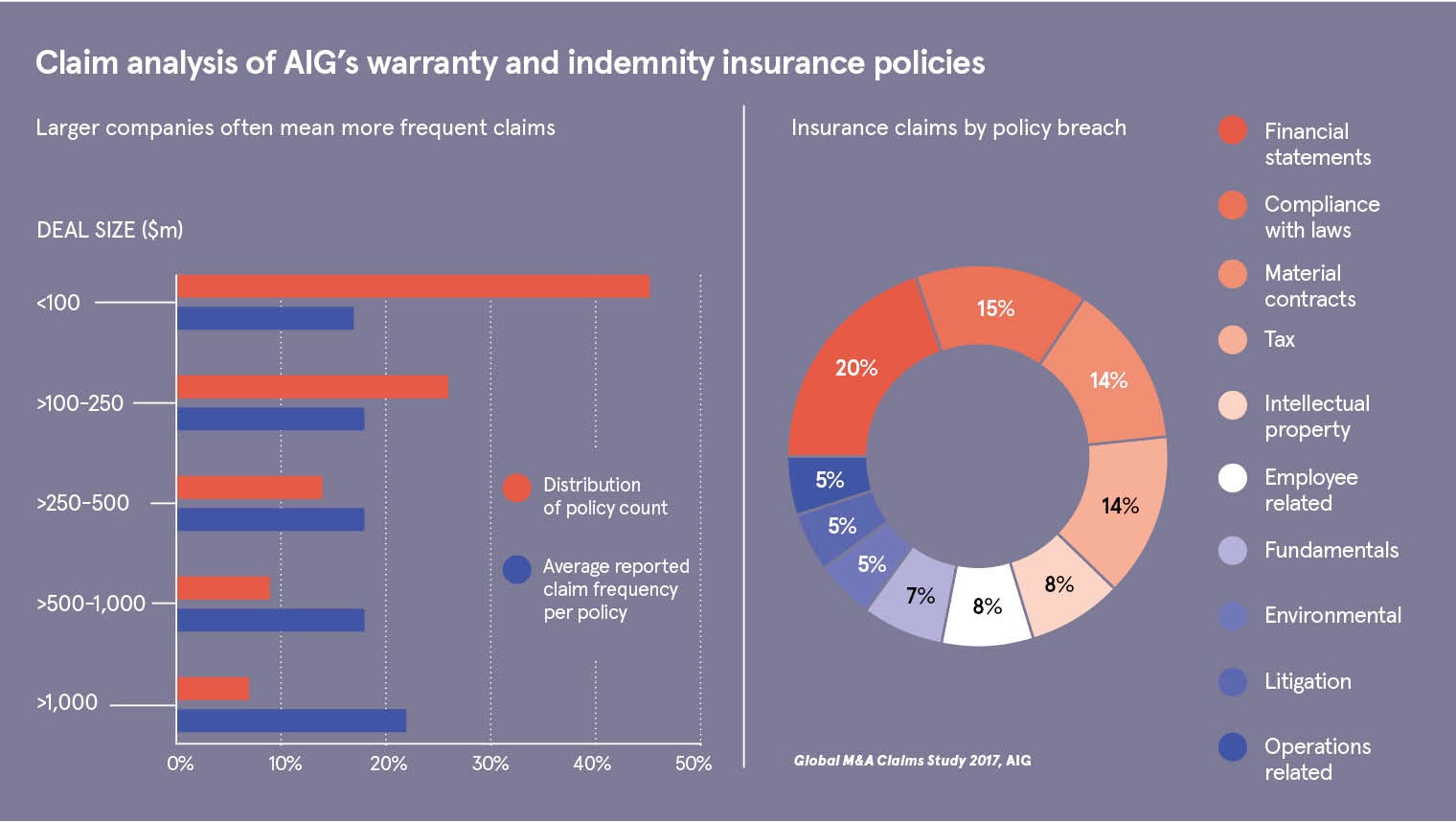

The use of W&I insurance in M&A transactions has offered stability to one facet of the sale process in what is a period of considerable economic uncertainty

The analysis looks at sales of all insurance policies that cover risks related to M&A, including warranty and indemnity (W&I), tax indemnity and contingent liability insurance.

Significantly, the group noted increased appetite for W&I insurance, a bespoke insurance product which offers cover for breaches of warranties, covenants and indemnities in an M&A transaction.

Number of firms offering W&I insurance has shot up

According to Leo Flindall, co-head of UK transactional risk in Marsh’s Private Equity and M&A Practice, the growing interest in W&I insurance has led to an explosion in the number of insurers now offering policies.

He says: “Six years ago, there were six insurers offering this product; today we have over 25. This supply-and-demand dynamic has meant each of those carriers are competing with each other.

“Coverage of policies has become broader, driven by the work brokers are doing with insurers to meet clients’ needs.”

The Marsh report reveals that sustained interest in these policies throughout 2017 and the subsequent increase in competition that followed has led to a reduction in the cost of the cover.

Sam Pennington, partner in the corporate team at law firm Lewis Silkin, says certain sectors have been keener than others in embracing these policies.

“While the use of W&I insurance in M&A transactions has been available for some time, its use has increased dramatically in the past few years, particularly in the technology, real estate and manufacturing sectors,” he says.

“The use of W&I insurance in M&A transactions has offered stability to one facet of the sale process in what is a period of considerable economic uncertainty. Simultaneously, we have seen premium rates falling and average insurance limits increasing year on year.”

W&I insurance can be a strategic way of transferring risk

Peace of mind is the number-one reason for the growing popularity of these products, for all parties involved in the deal.

According to insurance broker JLT Specialty, the most common policy limit is between 10 and 30 per cent of a company’s total value, known as the enterprise value or EV. The cost of the premium is then calculated as a percentage of the policy limit.

Therefore, on a £200-million deal, a 10 per cent policy limit would be £20 million and would cost in the region of between 0.8 to 1.5 per cent or between £160,000 and £300,000, depending on jurisdiction, industry sector, excess levels and complexity of the transaction.

“W&I insurance has been growing in use over the past decade as a strategic way of transferring risk on a transaction,” explains Hayley Tennant, a partner in the M&A team at JLT Specialty. “Sellers now have record levels of capital at their disposal, leading to an increase in auction sale processes where the seller requires the buyer to purchase W&I in lieu of indemnity protection.

“There has also been a rise in nil-recourse deals, particularly within the real estate sector. In such scenarios, the seller desires a clean exit enabling return of funds to investors and the buyer must rely on the insurer’s security.”

Bringing peace of mind and alleviating threat of litigation

Ms Tennant notes that interest has also been stimulated by recurrent scenarios where buyers have struggled to secure acceptable levels of indemnity protection in their transaction documents. “Buyers then use the W&I insurance policy to ‘top up’ their protection,” she says.

Interest in W&I insurance has not purely been from parties involved in M&A transactions, however. The product is also used by administrators and liquidators of private equity funds who want reassurance that contingent liabilities are covered after funds have been closed.

Marsh’s Mr Flindall explains that using a W&I insurance policy can help assist with any tax or legal issues which arise after these funds have closed.

“A common example is where there is a historical tax exposure because of a fund’s structure or because of some of the actions that the fund has taken as part of its disposals,” he says.

Mr Flindall adds that W&I insurance may also alleviate the threat of litigation, which has been paused, but where the liquidator is seeking reassurance the liabilities will be covered should legal action recommence.

Falling premiums could see market penetration for W&I insurance grow

The growing versatility and popularity of these products will drive continued innovation in the months ahead, but falling premiums may also play a part in shaping the W&I insurance market.

“I do think we will see more carriers coming into the market,” says Mr Flindall. “There are two or three that are in the process of doing so and other carriers will look to this market.

“For carriers looking for growth, this is one of the markets where there is a strong growth profile. But over time, a number of carriers may step away from the market as we start to go through an insurance cycle where premium rates have been eroded due to competition.”

Mr Flindall explains that market penetration for W&I insurance is still relatively low globally, despite it having become better known in the UK, but highlights the rapid growth of the product, particularly in the United States, in recent months.

Number of firms offering W&I insurance has shot up