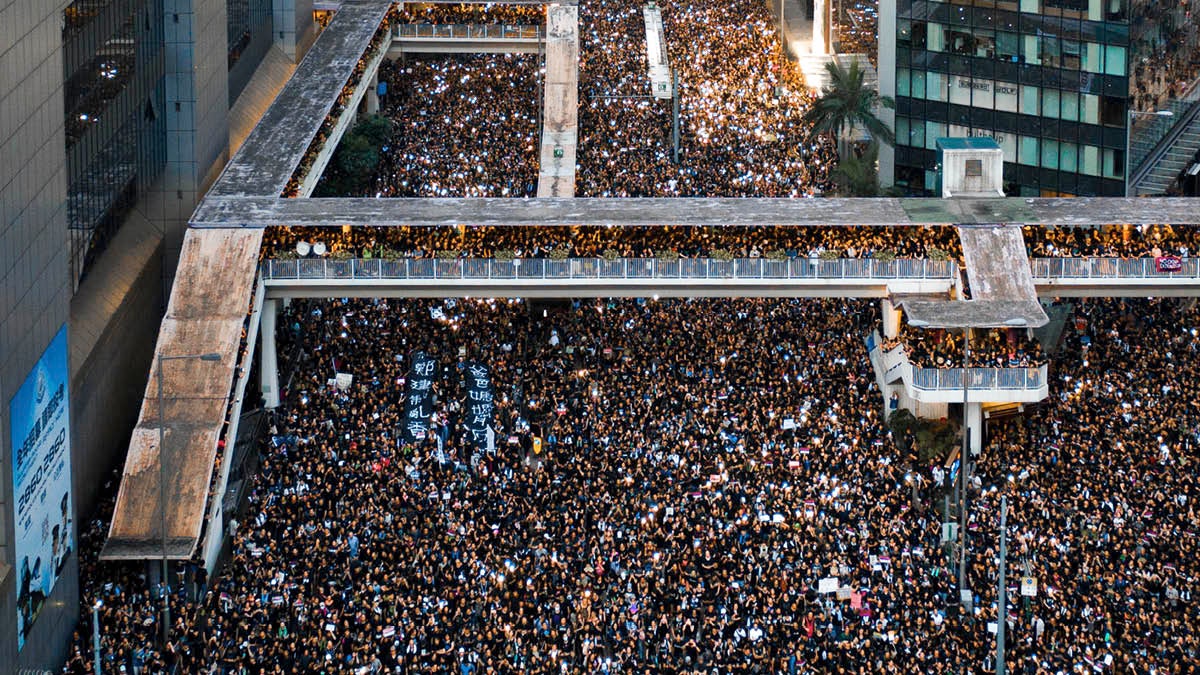

Boarded-up stores and angry crowds in Philadelphia, Paris, Hong Kong and Santiago mean one thing: the threat of civil unrest. Incidents such as riots and protests are now challenging terrorism as the main political risk globally. It’s leading to more insurance claims and businesses gobbling up policies for so-called strikes, riots and civil commotion (SRCC) insurance.

As the economic fallout from coronavirus mounts, protests look set to multiply. There are millions of newly unemployed, unpaid and unsatisfied people around the world posing new threats. Some 37 countries now face major spikes in unrest, according to global risk analysts Verisk Maplecroft. The outlook is particularly concerning for emerging markets.

The Black Lives Matter protests have also sparked a global chain reaction in civil unrest, as well as issues for the insurance industry. Losses to businesses due to property damage, disruption and slashed revenues in at least 40 urban areas in 20 US states alone may amount to the costliest civil unrest in American history.

“Disorder after the death of George Floyd is expected to have caused losses of more than $1 billion in US cities,” says Björn Reusswig, head of global political violence at Allianz. “SRCC is now the number-one contender for being the primary peril to be insured and underwritten.”

Civil unrest and its coverage in policies is rapidly topping many a company agenda, with businesses looking closely at the coverage they have. The main challenge lies within policy wording and definitions.

“Within an all-risk property policy, SRCC is not always defined as a named peril, which can result in difficulty in adjusting and even paying claims,” says Sandy Warne, international head of political risk at The Hartford.

Insurance firms have offered SRCC cover, either as part of an all-risk property insurance policy or as stand-alone cover for some time, yet because of recent events, sales of policies in the United States covering businesses specifically for civil unrest doubled in October from September levels.

“It’s viewed as nice to have for clients and nothing to be overly concerned about by the insurance industry. However, this has changed significantly since 2018 as both the frequency and severity of events has increased,” says Reusswig.

Time for separate SRCC insurance cover

Some insurers, notably at Lloyd’s of London, have stopped including SRCC cover within general property policies for businesses that have been hit hard by civil unrest. This has forced them to buy separate SRCC insurance.

“A recent example of this is Chile where up until the autumn last year SRCC was a standard coverage within all-risk policies. After the nationwide unrest and subsequent large losses within the property insurance market, SRCC perils were excluded from all-risk policies at renewal,” explains Marie Biggas, vice president, terrorism at Arch Insurance.

Since civil unrest in Chile came with a $2-billion price tag, it’s no wonder there was concern within the sector. This type of risk category is now under a lot more scrutiny. However, calculating risks associated with civil unrest isn’t easy. SRCC incidents resulting in industry-wide insured losses are infrequent.

“We’ve reported on fewer than 15 incidents in the past 70 years, with more than half coming before 1980. Large riots with significant industry impact can be difficult to understand, because historically there haven’t been many. The last riot, before Mexico in 2017, of any insurance industry significance was likely to be the Tottenham riot in the UK in 2011,” says Tom Johansmeyer, head of property claim services at Verisk.

SRCC insurance has become an essential product for many businesses due to the rapidly changing political landscape

However, thanks to social media and the speed of the internet, news that sparks events can now travel across continents in seconds. This can accelerate civil commotion in ways that didn’t exist a decade ago. Look at how Black Lives Matter protests went global. The socio-economic factors that have led to several instances of unrest throughout 2020 may be around for a while, including the COVID-induced economic recession.

“There’s no doubt SRCC insurance has now become an essential product for many businesses due to the rapidly changing political landscape,” says Andrew Bauckham, deputy practice head for property and political violence at Chaucer and chairman of the Lloyd’s Terrorism and Political Violence Panel.

The evolving market is less predictable

While the timing, location and fallout from civil unrest is very unpredictable, SRCC cover itself is fairly straightforward. Important additional coverage that’s also coming to the fore is that of business interruption insurance, which can help in the wake of civil unrest.

“There are also steps a business can take to mitigate risk, which may then reduce the premium for SRCC insurance. For instance, installing protection for storefronts and business windows and doors, and having contingency plans in place. This may reduce premiums for SRCC cover,” explains Rich Dodge, partner for commercial litigation at Dentons.

There is no doubt the market for SRCC insurance policies is evolving. The insurance industry is also getting better at gauging this risk category. It certainly will not be a free-of-charge add-on like it was some years ago. Those who insure property are now looking to separately define and limit SRCC cover. This could leave businesses with limited protection.

“The capacity and appetite may now be limited within the terrorism and political violence market, where this insurance sits, and it may prove difficult for clients to be able to afford or even be able to purchase cover at previous levels,” Warne at The Hartford concludes.

Boarded-up stores and angry crowds in Philadelphia, Paris, Hong Kong and Santiago mean one thing: the threat of civil unrest. Incidents such as riots and protests are now challenging terrorism as the main political risk globally. It’s leading to more insurance claims and businesses gobbling up policies for so-called strikes, riots and civil commotion (SRCC) insurance.

As the economic fallout from coronavirus mounts, protests look set to multiply. There are millions of newly unemployed, unpaid and unsatisfied people around the world posing new threats. Some 37 countries now face major spikes in unrest, according to global risk analysts Verisk Maplecroft. The outlook is particularly concerning for emerging markets.