The coronavirus pandemic was a major event that no one saw coming. Known as a black swan, after Nassim Nicholas Taleb’s theory, it was an unforeseen event with devastating consequences.

In an increasingly uncertain world where pandemics, cyber and terrorist attacks, as well as extreme weather events, are becoming commonplace, businesses are finding it harder to anticipate such risks and, therefore, protect their supply chain and operations.

Traditionally, companies have mitigated against risk by taking out an insurance policy. Underwriters would spend hours poring over reams of historical data to determine the likelihood of the risk occurring before giving a quote.

Using AI to predict unforeseen events

But that is all changing now with the adoption of artificial intelligence (AI) and machine-learning to try and predict major events, including black swans. The key benefit of AI in insurance is that it can quickly process large data sets and identify significant trends, and every time it becomes smarter at pre-empting these risks. This enables underwriters to assess and price risk much more accurately.

“AI will fundamentally disrupt and transform insurance underwriting,” says Ari Libarikian, senior partner at McKinsey & Company. “Carriers are now able to better predict losses, provide advice and help customers prevent risks. AI is allowing that in a much bigger way than was ever possible before.”

Heavy investments have already been made in AI in insurance, with 37 per cent more machine-learning patents filed year on year in 2017, according to law firm RPC. At the adoption stage, Accenture found 53 per cent of insurance executives are already using intelligent technologies in one or more of their business processes.

The move towards AI in insurance is being driven by a wider availability of data from multiple sources, facilitated by several factors, including cloud storage, open-source technology and the digitalisation of operations. It’s also being used to evaluate newer risks such as cyberattacks.

“AI is used for forecasting the frequency and severity of certain cyber-perils, such as predicting the probability of experiencing a data breach or ransomware attack,” says Erin Kenneally, director of cyber-risk analytics at Guidewire. “It can also understand and predict where there are risk concentrations across a portfolio of policies, where multiple insureds may be exposed to common IT suppliers and technologies.”

How insurers can protect against cyber-risks

Cyber-risk is further complicated by a general lack of data and the absence of an adequate modelling framework, as well as constantly new and evolving threats. That’s where AI comes in, enabling underwriters to infer information where gaps in the data remain.

“AI can generate probability distributions for the frequency and severity of losses companies are likely to suffer, what coverage areas are going to be hit, who the actor will be, what method they will use and what type of data they will target,” says John Kelly, chief technology officer at Envelop Risk. “That all comes together to allow you to run a simulation that can give an effective view of what the risk looks like.”

Dr Marcus Schmalbach created the VUCA (volatility, uncertainty, complexity and ambiguity) World Risk Index, a parametric index that uses machine-learning to gather data from a range of trusted and verifiable sources, many of which aren’t considered in traditional underwriting. That data is then rigorously analysed alongside information the technology has gathered from previous experiences to look for patterns and links between events, and determine the likelihood of a major event occurring.

“This technology has, for example, enabled us to calculate and successfully price the probability of a share price slump in the event of a cyberattack for a client from the high-tech sector,” says Schmalbach. “We have also created a product aimed at covering business interruption loss in the event of a pandemic, based on the data we gather.”

Can AI foresee floods and forest fires?

Risk-modelling companies also use AI to improve their natural catastrophe prediction models. AIR Worldwide, for example, is using AI to simulate how water flows through reservoirs and rivers, and how dams operate, to forecast different flooding scenarios.

“By blending these climate models and machine-learning algorithms in areas such as rainfall and weather patterns to run hundreds of thousands of simulations, we can work out the potential for different outcomes,” says Dr Milan Simic, executive vice president at AIR Worldwide’s parent Verisk. “We have used this to great effect in the United States and Japan to forecast the extent of hurricanes and tropical cyclones.”

As well as more accurately predicting and pricing risk, AI in insurance can reduce paperwork and the time taken to receive a quote or claim. Using parametrics, AI can also establish if an event has happened, thereby triggering payouts and avoiding any disputes.

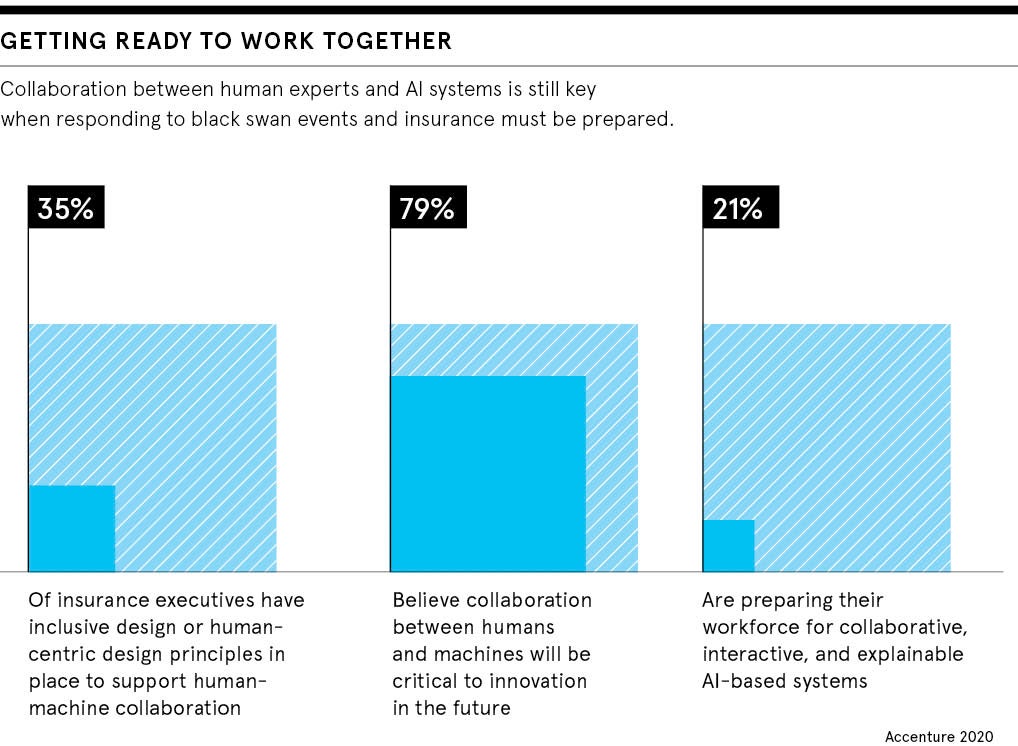

However, AI has its limitations, with human underwriters still required to handle more complex and specialist risks. Those underwriters will have to equip themselves with the data-science skills needed to work effectively with the new technology.

It may not be there just yet, but had AI been able to detect COVID-19 at the outset, countries and organisations may have been better equipped to prepare for it. Without a doubt though, AI in insurance has a vital role in helping to anticipate future events, even black swans.

As Jacopo Credi, vice president of AI at Axyon AI, concludes: “Nobody can predict the unpredictable. However, sophisticated AI models can detect anomalies and this is a powerful way of anticipating future events, which can have a very different impact than anything else we’ve seen in the past, just like the impact of COVID-19.”

The coronavirus pandemic was a major event that no one saw coming. Known as a black swan, after Nassim Nicholas Taleb’s theory, it was an unforeseen event with devastating consequences.

In an increasingly uncertain world where pandemics, cyber and terrorist attacks, as well as extreme weather events, are becoming commonplace, businesses are finding it harder to anticipate such risks and, therefore, protect their supply chain and operations.