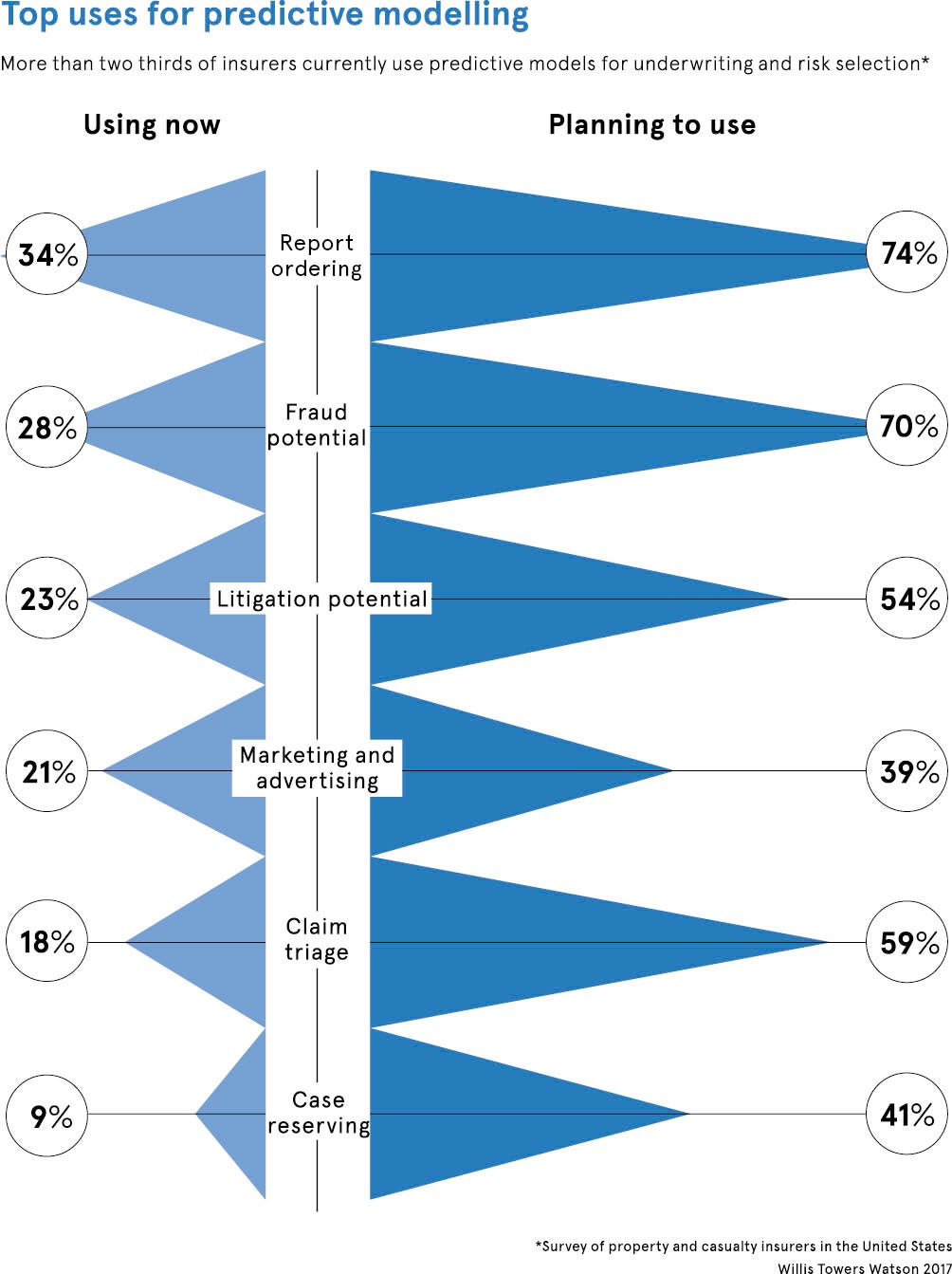

Dramatic advances in artificial intelligence and machine-learning technologies have accelerated the ability of insurers to predict risk. Algorithms can find trends and patterns that help forecast the probability of a risk situation occurring again.

By utilising internal and external data sources, algorithms are selected according to how a specific model fits with the insurer’s data. This model is applied to predict or detect the likelihood of an event happening, such as a person needing medical attention abroad for travel insurance or a house flooding for home insurance.

Insurance and assistance provider The Collinson Group uses a variety of predictive analytical tools to flash through terabytes of data to find variables, some of which it hadn’t considered, to help predict customer risk and purchasing behaviour.

With this technology, the company is able to identify fraud and the different networks of fraudsters acting in the market, as well as increase its understanding of customers, and ultimately tailor its offering to provide them with better products and services.

“Predictive analytics has enabled a more scientific approach to analysis, allowing us to analyse more data in little or no time, and to explore parameters and factors we could not have identified with the human eye,” says Jean Ortiz-Perez, the company’s head of analytics. “The concept and objective of what we do have not changed, but the mechanisms and techniques are now much more sophisticated.”

The role of predictive analytics in insurance can actually be traced back two or three decades in the area of natural catastrophes and climate. Analysis of 50 years of data on hurricanes, for example, has proven extremely powerful in terms of helping insurers to predict future hurricane behaviour and its likely impact.

However, this has required a large amount of human input and oversight. More recently property and liability insurers have been playing catch-up with the life insurance sector, where a rich trove of available data, including longevity, gender, country and quality of life, has allowed for clearer analysis and confident predictive outputs.

The rapid evolution of machine-learning capability and the wider availability of data through connected devices are now set to make the use of predictive analytics ubiquitous across the industry. And to accelerate the necessary collection of data, new health insurance models are emerging that actively link premiums to analytics.

In the automotive sector, for example, telemetry and driving apps are not only encouraging people to drive safely by incentivising them with reduced premiums, but they’re also arming insurers with the necessary data to power predictive analytics. Healthcare insurers, such as Vitality, reward members with a free Apple Watch if they commit to trackable daily exercise goals.

The potential of these technologies is huge, with scope for insurers to change their business models as compensators of accidents to preventers

“The potential of these technologies is huge, with scope for insurers to change their business models as compensators of accidents to preventers,” says Roy Jubraj, UK insurance strategy and innovation lead at Accenture. “Insurers can even use analytics, with data pulled in from smart homes and connected devices, to intervene before an incident happens in the first place. It’ll see insurers plugging into their consumers’ lives and wider eco-system to look after the asset or risk they want to protect.”

Matthew Grimwade, senior partner at insurance broker JLT Specialty, adds: “The next and very exciting chapter, driven by artificial intelligence and ever-improving technological capability, will drive down costs and continue to improve the quality of the predictive outputs, and enable the industry to deliver insights and predict risks even faster.”

Insurance companies are operating in a difficult market, facing disruption from startups shaking up the status quo, while having to transform their operations to meet the increasing demands of a real-time digital world. They need to innovate to survive.

The sophistication of predictive analytics will increase rapidly over the next few years, as truly data-driven insurers emerge that are able to make better decisions faster. Such innovation will improve predictions of loss and enhance consumer response to new products, driving positive business results that boost both the top and bottom lines.

One large global insurer, which manages a motor insurance portfolio of a million policies through 200 large agencies, implemented demand-based predictive models through technology from analytics firm Earnix. The insurer saw a profit improvement of 2.8 per cent, while maintaining existing customer retention levels.

“As more insurers operationalise these new methods, current insurance product offerings will be revolutionised,” says Udi Ziv, chief executive at Earnix. “Already new products are appearing in the marketplace, such as car insurance by the hour or temporary home insurance. Combine these with customer expectations for more personalised levels of service and it’s clear insurers need to adapt to this changing market. They will need to harness predictive analytics to become customer centric at levels previously unseen.”

Done responsibly, with consideration for concerns over the use of personal data, insurers can shift their relationship with customers from a grudge purchase to one of value. But this approach hinges on maintaining consumers’ trust. Using analytics to identify which customers will value this capability and service is beneficial, but insurers must always use these new methods and algorithms responsibly.