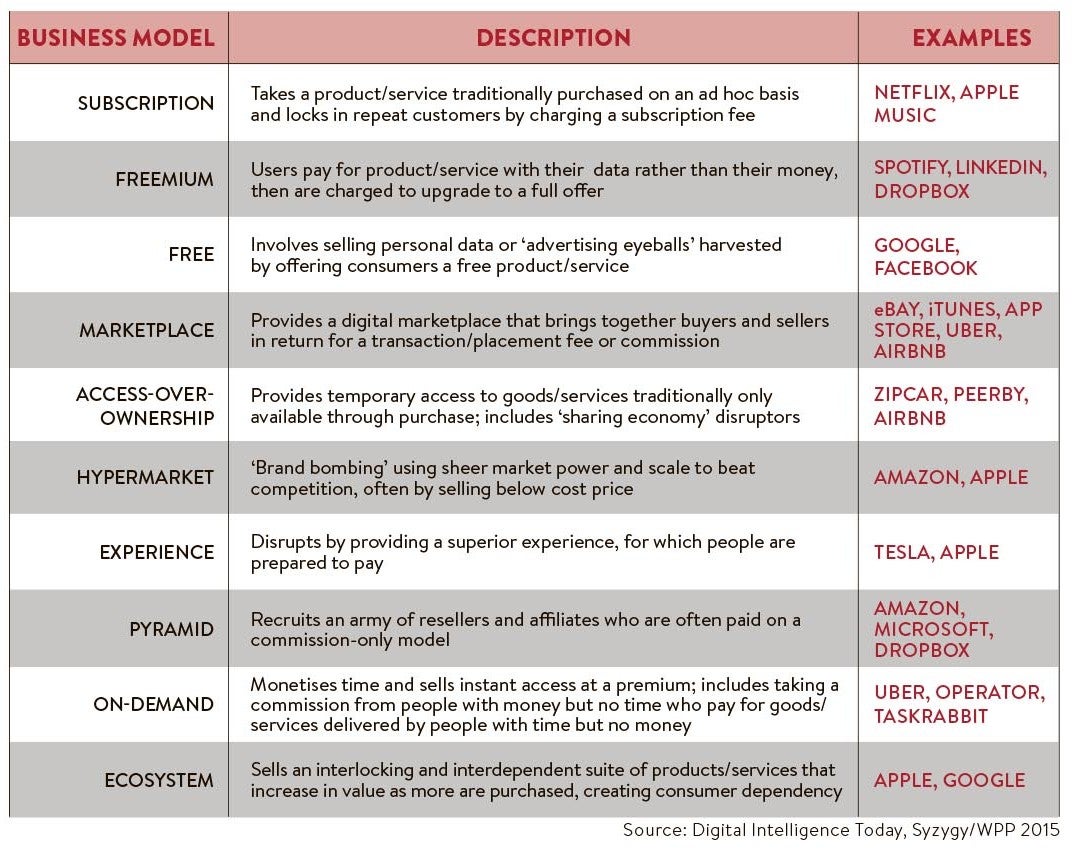

Online marketplaces are revolutionising the economy. Using mobile apps, some clever algorithms and a customer review system, businesses such as Uber, Airbnb, Alibaba and eBay have transformed what it means to be a middleman.

These modern day intermediaries connect buyers and sellers, and offer reassurance that goods and services will arrive, meet expectations and be paid for without problems. They are “weightless” businesses with few assets; Uber owns no cars, Airbnb owns no property and Alibaba holds no stock. They outsource risk, they piggyback on other people’s technology and connectivity, and some play hard and fast with regulation. They often manage to conjure up new markets from underused assets.

Responding to change

Uber’s rapid global growth has led to widespread criticism from licensed taxi drivers who claim unfair competition due to a lack of regulation of private hire vehicles

But the rise of the online marketplaces poses a massive challenge to the wider economy. Established operators are struggling to match the new business models and many are seeing their livelihoods under threat.

Taxi drivers around the world have challenged the legality of Uber, while Airbnb has also faced legal constraints on its model of rental accommodation. But these startups grow so fast they are already huge before established interests can organise a fightback. Companies are facing up to the reality that their profit model could be disrupted within a few short years by unexpected startups that come from nowhere to wipe out their business.

As Tom Goodwin, senior vice president for strategy and innovation at Havas Media US, says: “Technology is making incredible things now possible. Every company, regardless of what business they are in, seems to be looking at new technologies and the new behaviours that come from those technologies and looking to leverage them.”

The network effect

Mr Goodwin refers to the online marketplaces as “skins”, small businesses connecting huge numbers of buyers and sellers. “It is about owning no assets, where possible skirting regulations, employing a small number of staff, and doing the minimum job so you are outsourcing the risk and the responsibility to the buyer or the seller. In becoming a connector, that allows you to grow incredibly quickly, to grow around the world in a way that doesn’t require local staff,” he says.

Crucial to the growth of many online marketplaces is the way they have used technology to change people’s behaviour and attitudes. He adds: “A while ago, companies would have assumed that people didn’t want to spend the night in a stranger’s house, that they wouldn’t really trust a stranger to drive them around. But with the customer review system, there is an implied trust in the brand itself. You presume Uber is doing its due diligence on its drivers, you presume that Airbnb is making sure that you are not going to feel unsafe in the property.”

These businesses thrive on the network effect – the more buyers and sellers they unite, the more valuable they become to new participants. This has helped them rapidly achieve huge scale. Ride-hailing app Uber launched in 2009 and is now present in 300 cities around the world. Five years after launch, apartment rental service Airbnb offers 500,000 homes in 34,000 cities. Chinese e-commerce business Alibaba connects buyers and sellers across China and across continents as well.

Business models of the future

Hussein Kanji, a partner at venture capital specialists Hoxton Ventures, which backed restaurant delivery service Deliveroo, says it is hard to tell if a new business model is going to succeed. “They don’t look all that interesting in the early days because you can’t tell if they are going to get scale or not,” he says. “You can’t often tell if they can succeed as an intermediary. Once they start maturing and they are one or two years in, you can see why they are becoming very valuable businesses.”

Mr Kanji adds that in the early days of the internet, many believed the technology would lead to the end of middlemen and people would be able to interact directly. In reality, it turns out intermediaries are vital.

He believes it is hard for established businesses to combat these new business models. “Becoming a competitor is darn near impossible for bigger companies. It is not like Marriott, Starwood or Hilton hotels can go and build a competitor to Airbnb,” he says. “Once they win, it’s a winner-takes-all market and they become dominant.”

Established players must watch out for new, disruptive digital business models. They can become early investors or partners, or get involved in some way. For instance, a hotel group with an eye for transformative startups could have listed its properties on Airbnb in the early days to gain an early-mover advantage.

Another strategy is for an established business to work out how to piggyback the new services. For instance, car manufacturers could create a healthy business insuring and renting out their cars to the growing numbers of Uber drivers.

[embed_related]

Uberisation

Many businesspeople are wary of what has come to be known as “uberisation”, where established business models are disrupted by a low-cost digital platform, just as Netflix is threatening the network TV model and new mobile-based banks could take market share from established banks.

But according to Mike Sutcliff, chief executive of consultancy Accenture Digital, fears of uberisation have been exaggerated. “The leading companies in each industry are as actively invested in experimenting and creating the future as any of the startups are,” he says.

All major car companies have a presence in Silicon Valley, he says, and have venture capital units following the progress of interesting new startups. The automobile businesses all have labs working on driverless cars and battery technologies.

“What we talk to clients about is not only the industry they are in and their existing competitive set, but we ask them to think about the adjacent industries and whether there is an opportunity to bring a different economic model that would disrupt the profit pool they are playing in today,” says Mr Sutcliffe.

The leading companies in each industry are as actively invested in experimenting and creating the future as any of the startups are

He points to US business Zenefits, which offers free software to run the employee payroll and other labour services for small and medium-sized businesses in return for those companies using it as a health insurance agent. It has been highly successful and provides stiff competition to the established players in employee benefits.

“They have taken an adjacent market play and said the market I’m in is being an insurance agent, the adjacent market that I am disrupting is the market of providing employee benefits, so all the players in the employee benefits market would describe themselves as being uberised,” says Mr Sutcliff. So it is an adjacent market entry that many businesses need to look out for.

Established businesses need to hold their nerve in the face of the profit-destroying new digital business models. As Mr Goodwin of Havas Media US concludes: “You should be both wary and excited at the same time. The worst thing you can do is ignore this; the best thing you can do is bring in people who understand the changes that are now possible in order to figure out the opportunities this will offer.”

CASE STUDIES: DELIVEROO, TRANSFERWISE AND JUSTPARK

Some of the UK’s brightest new companies are using digital business models to open up new markets and challenge established interests.

Some of the UK’s brightest new companies are using digital business models to open up new markets and challenge established interests.

Deliveroo, co-founded in London by Americans William Shu and Greg Orlowski, delivers meals to customers from quality local restaurants using an army of cycle and scooter drivers. Its smartphone app allows customers to choose from a number of restaurants in their area with delivery promised in about half an hour.

Mr Shu believes this is not eating into any other business, but is building a completely new market, as most of the restaurants involved did little takeaway business before Deliveroo came on the scene. “We are not substituting anything; we are creating something completely new. It was something you couldn’t actually have gotten before and I think that’s an important distinction,” he says.

Since it launched in London in February 2013, the service has expanded to 34 cities in the UK and overall 55 cities worldwide in 12 countries. It is now launching in Asia. The company, which employs some 300 people, has raised $200 million in funding from backers and has been valued at between $350 million and $660 million.

A truly disruptive business in the financial sector is TransferWise, which has transformed international money transfers and created stiff competition for banks. It has massively reduced the fees for making cross-border money transfers by using an algorithm to match requests in different currencies.

No money actually crosses any borders, but if someone in Europe wants to send €100 to the UK, this is matched with the equivalent in pounds from someone in the UK wanting to send money to Europe. This system enables the company, which is based in London, to charge minimal fees. So far some £3 billion has been transferred via TransferWise.

Another venture that has unlocked value from previously underused assets is JustPark, which connects drivers looking for a parking space with people who have a drive or piece of land they want to offer for parking. It has been described as an Airbnb for parking.

The service charges a 20 per cent commission on parking. With 750,000 registered users and some 150,000 parking spaces, the business turned over £3.7 million in 2014, with net revenue of £1 million. It has received venture capital funding, an investment from BMWi and last year raised £3.5 million on crowdsourcing site Crowdcube, a record for a UK startup.

Responding to change