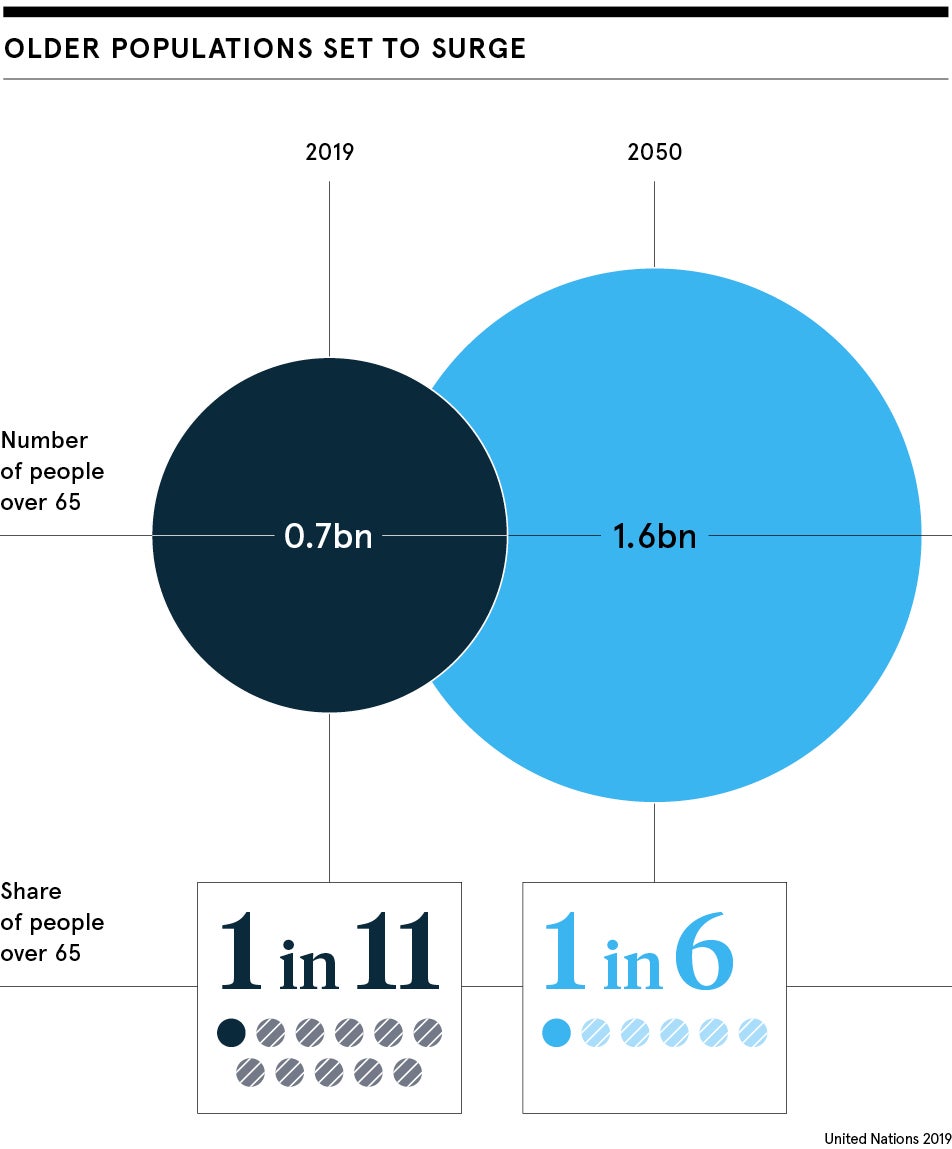

As you read this there are some 7.7 billion people in the world. Not only is that figure increasing by the second, but so is the average age of our fellow planet-dwellers. Come 2050, the United Nations estimates this upward trajectory will have added another two billion people to the Earth’s population.

Significantly, some 1.6 billion of these 9.7 billion souls will be over 65, which means that in 30 years one in six people will be of retirement age. That compares to just one in eleven today.

Of course, the planetary greying will not be evenly distributed: one in four people in Europe and North America is expected to be over 65, while the population of over-65s will double elsewhere. Meanwhile the number of people over 80 is expected to rise from 143 million today to an astonishing 426 million in 2050. That’s not far off the present population of the entire European Union.

Against this backdrop, 55 countries or regions will see their populations decline, many markedly, all helping to reduce the proportion of workers to dependents.

Already in Japan that ratio is 1.8, so each pensioner is supported by fewer than two workers. In 30 years, 48 countries will have ratios under two. “These low values underscore the potential impact of population ageing on the labour market and economic performance, as well as the fiscal pressures that many countries will face in the coming decades as they seek to build and maintain public systems of healthcare, pensions and social protection for older persons,” the UN warns.

In other words, it’s not looking good. And it gets worse when you consider studies have shown that an ageing population will also reduce levels of economic growth. For evidence of this, look no further than the insipid economic performance of Japan over the last two decades.

Is the pensioner boom akin to climate change?

Mark Williams, chair of the pensions board at the Institute and Faculty of Actuaries, puts the scale of the pension problem this way: “It’s a little akin to climate change in a sense that it’s something that people know about and most people recognise it’s a problem, but in terms of solving it, it’s baby steps,” he says. “At the moment, the pace of change is too slow for us to have a situation where things are going to improve in a way that isn’t going to lead to a pretty big car crash at some point.”

So just how bad is the pensions shortfall? “There is no doubt that there is a generation of people who are not going to be able to afford to retire at any sort of sensible age based on current projections,” says Williams. “The implications of that are enormous.”

Just one is that even though the population of over-65s will soar, the numbers who actually retire will start to lag. “I would certainly expect that people will need to work into their seventies,” says Williams.

It’s something that people know about and most people recognise it’s a problem, but in terms of solving it, it’s baby steps

Across countries in the Organisation for Economic Co-operation and Development (OECD), the official long-term retirement age average for those entering the workforce now is 66, while in the UK it’s 68. But if Williams is right, this could just be the tip of the iceberg. If people can’t afford to retire, they won’t.

Another factor in play is the economic health of those retiring in 2050; currently new retirees might reasonably expect to have paid off mortgages. But you might not be so lucky in the 2040s and this is not just a British problem either. “The trends for an ageing population and for there being an adequacy problem around pension saving in a money purchase form are certainly issues that are prevalent around the globe,” warns Williams.

So what needs to be done? Most importantly, more money needs to be saved for old age – actuaries say it’s £800 a month in the UK – which will probably need to come from increased employers’ contributions as well as employees’ themselves, and the state. “If everyone does something there is a set of circumstances that means you are not in a doom-and-gloom scenario,” Williams adds. “But there is no doubt this means quite a big change, just as it does for climate change.

“This is a massive issue facing our industry. The first step is to recognise it, then take the steps. But it will take a bit of pain and a lot of work.”

There is no silver bullet for pensions challenges

Monika Queisser, the economist who is head of social policy at the OECD, doesn’t deny the challenges, but takes solace in the fact that effective retirement ages are increasing and labour-force participation among the elderly and women is rising.

“There’s no silver bullet,” says Queisser. “Working longer remains the most effective way to deal with the challenge. By working longer you’re reducing the time you have to be paid a pension and you’re increasing the resources that go into the pension system through contributions.”

But she does not think people will continue to work into their seventies in great numbers, mainly because for many, such as manual workers, it won’t be an option. Similarly, while many countries have scaled back their pensions promises to balance the books, she says: “There’s limits to how far you can go because obviously people need some sort of meaningful replacement of their earnings in retirement.”

This leads to her main concern: the prospects for old-age inequality. “This is something that countries should be worrying about a lot more. It’s also one of the reasons why increasing retirement ages is so unpopular because there’s so much inequality in life expectancy, where you have people from high socio-economic groups who live much longer than people from lower socio-economic groups. This compounds over the life cycle,” says Queisser.

When you consider that income inequalities in developing and emerging economies are typically higher than in OECD countries, as indeed are the health inequalities, then you begin to see the scale of the problem. And that’s before you account for the much higher proportions of the workforce in informal parts of the economy, many of whom are unlikely to fall within a pensions system, in developing countries. That’s a figure which is as high as 80 to 90 per cent in India, for instance.

“If those countries don’t succeed in lowering health and income inequalities and education inequalities over the life cycle, they’re setting themselves up for even more dramatic inequalities in old age,” Queisser warns.

In short, it could be a bumpy ride. So start saving and buckle up.

As you read this there are some 7.7 billion people in the world. Not only is that figure increasing by the second, but so is the average age of our fellow planet-dwellers. Come 2050, the United Nations estimates this upward trajectory will have added another two billion people to the Earth’s population.

Significantly, some 1.6 billion of these 9.7 billion souls will be over 65, which means that in 30 years one in six people will be of retirement age. That compares to just one in eleven today.

Of course, the planetary greying will not be evenly distributed: one in four people in Europe and North America is expected to be over 65, while the population of over-65s will double elsewhere. Meanwhile the number of people over 80 is expected to rise from 143 million today to an astonishing 426 million in 2050. That’s not far off the present population of the entire European Union.