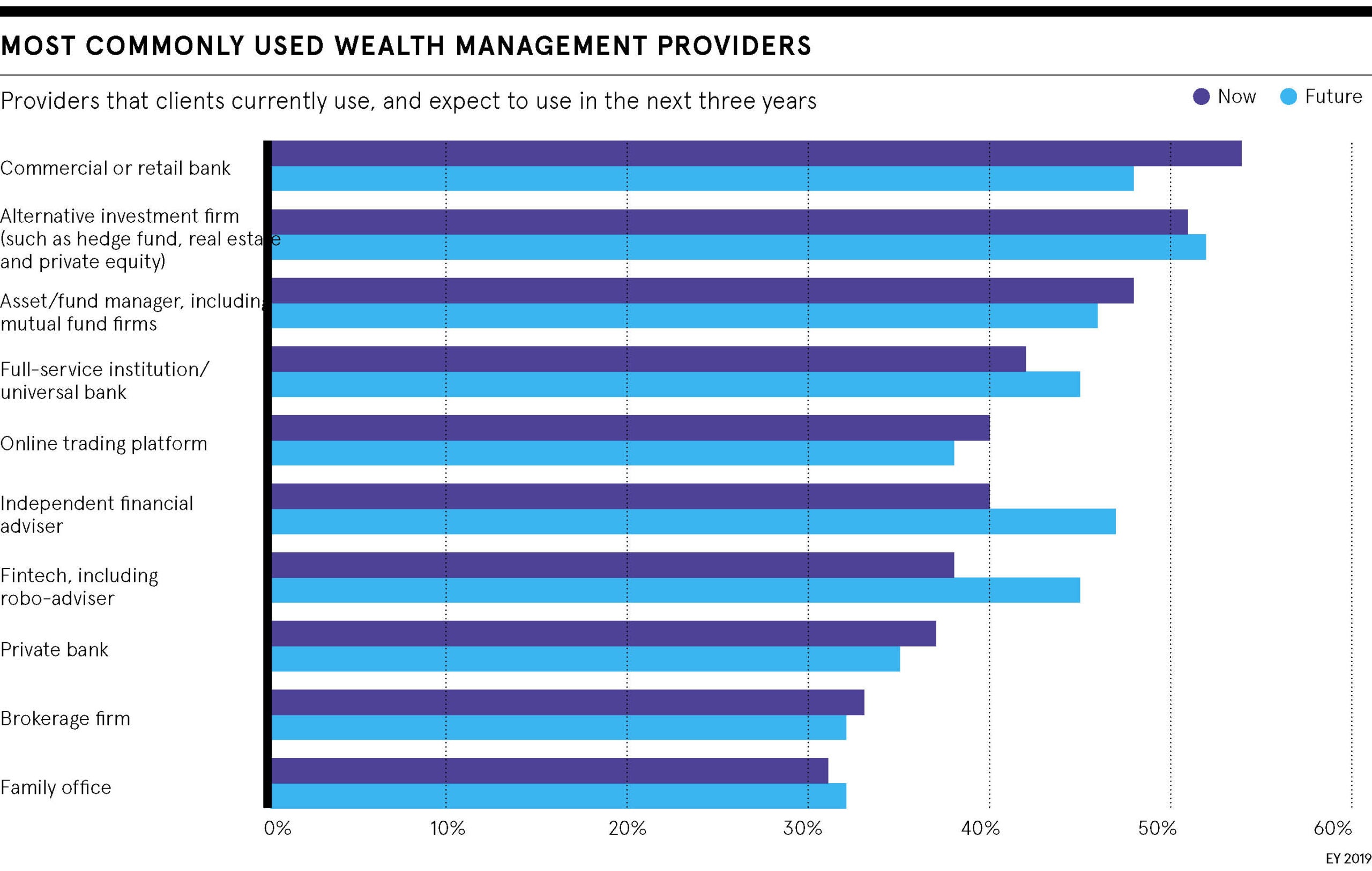

How to choose a wealth manager is not just an ultra-rich billionaire’s dilemma. More and more people in the UK need advice about their pension savings, investments, belongings and property, and a good financial planner can be indispensable.

Against a backdrop of the damaging closure of high-profile Woodford Investment Management and continuing uncertainty in global markets, it is harder than ever to preserve capital and have a decent income when bank deposits pay derisory interest.

Yet, despite hourly reports of scamsters preying on vulnerable individuals, people often spend more time planning their holidays than selecting an adviser.

A total of 3.6 million households in Britain hold wealth of more than £1 million, according to the Office for National Statistics. That equates to one in five over the age of 65, and many people within ten years of retirement have amassed large sums in pensions, redundancy or inheritances.

First step: find a firm

So what’s the first step in choosing the right wealth manager for you? Firstly, any prospective wealth manager should be authorised by the Financial Conduct Authority, which can be checked via the FCA’s online Financial Services Register.

Often professional advisers, such as accountants and lawyers, will have a network of contacts and are well placed to steer you in the direction of a wealth manager. Friends and family, particularly, if they have been with a firm for a long time and have had good service, are another possibility.

Make sure you visit the prospective financial planner’s office. First impressions and gut instinct are important; even the quality of the furnishings and layout of the desks, as well as the website and mobile phone apps and paperwork, deserve scrutiny.

If you’re really stuck at where to start, it is often advised to look for a wealth management firm that has been in business for a decade or more, or quoted by financial journalists as a trusted authority. Billions of assets under management from many clients are also reassuring. Ask for testimonials from clients. Look for reviews on websites.

Patrick Connolly, chartered financial planner of Chase de Vere, says: “When looking at which financial advice firm is right for you, you need to decide whether you want to meet face to face with your adviser, whether you’re happy to work with them remotely by telephone or email, or whether you just need some information and then you’re happy to make your own decisions.

“If you make your own decisions, even if you’ve received guidance or information, then you are entirely responsible for your decisions. You will have no comeback if it all goes horribly wrong.”

George Houston, technical director at Mattioli Woods, advises to take some time to get to know your adviser and for them to get to know you. “It is worth the initial investment,” he says. “We are all human beings and some people just don’t get on; that is not to say you have to get on, it just helps if you do. Ensuring you and your family feel comfortable with a wealth manager is important as you will be sharing a lot of personal and financial information with them and hopefully the relationship will stretch into the foreseeable future.”

Questions to ask your financial planner

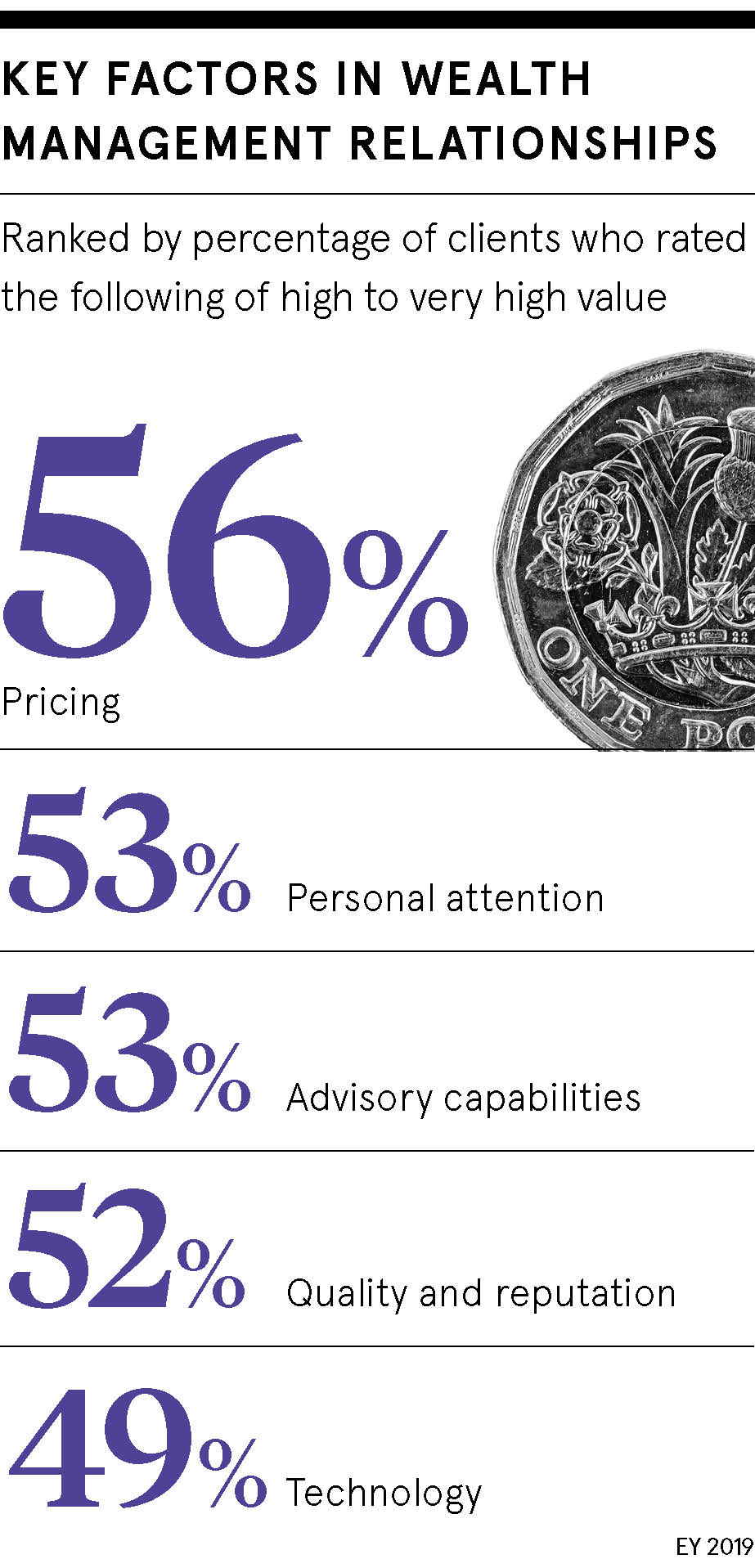

Find out what areas of specialism the financial planner has and what back-up plans are in place for when he or she is away from the office. Make sure everything is transparent, particularly charges as there can often be hidden extras. And also be clear on exactly what level of service you are getting in return.

First impressions and gut instinct are important; even the quality of the furnishings and layout of the desks

Will you get quarterly updates or more frequent communications? Is an investment manager available at the end of a telephone? How proactive are they? How quickly will they move when shares underperform or a company gets a series of profit warnings; will your holding languish in your portfolio for months?

Robin Eggar, co-head of UK investment management at Brooks Macdonald, says having a proper comparison is useful, so it’s necessary to meet and interview more than one adviser. “It is also important to note who is at that first meeting. Is it the person who is running your relationship going forward or a new business winner who needs to meet a sales target?”

As well as choosing someone you can trust, you should look for properly qualified individuals. There are a myriad of financial qualifications that can give comfort, such as the CISI Diploma in Wealth Management, the CFA Investment Management Certificate (IMC) Chartered Financial Planner, STEP (Society of Trust and Estate Practitioners) qualifications and accreditation from SOLLA (Society of Later Life Advisers).

Fees vary enormously. Wealth managers such as Quilter Cheviot might charge 1 per cent plus 0.2 per cent VAT a year of the portfolio value for discretionary management. Some financial planners operate on an hourly fee basis.

Good wealth managers will match your goals

Financial planners will take care to match your goals, such as concerns over the environment. Most wealth managers have been, and still are, ahead of the game when it comes to environmental, social and corporate governance (ESG) or sustainable investing.

Malcolm McLean, senior consultant at Barnnett Waddingham, says: “They have moved on from what has been rather facetiously described as the ‘green versus greed dilemma’ with ESG investing now being a key point of conversation with their clients.”

What are the warning signs?

Be on the lookout for warning signs. Rob Burgeman, investment manager at Brewin Dolphin, says: “If there has been a raft of negative publicity about a wealth manager, this should warrant investigation. When looking for a wealth manager, make sure you do your own due diligence. Use the internet to see what the media and wider industry are saying about an organisation you are interested in talking to. Make sure you don’t just rely on the media profile on their own website, research news articles and reports.”

As well as ensuring they are suitably qualified and regulated, other warning signs could be a lack of experience and/or a lack of clarity over charges. If the investment manager can’t show you long-term performance records against an appropriate index, avoid them.

Other danger signals include the prospect of exceptionally high returns, exotic offshore investments, recommendations for products you don’t understand, you don’t feel comfortable with your adviser or don’t fully trust them. Avoid advisers who can only sell a restricted range of products and anyone who pressurises you to make a decision. Don’t speak to cold callers or respond to unsolicited emails.

Many individuals are at risk of falling for scammers’ so-called investment opportunities, taking only a day to make a decision with a lifetime to regret it. So take your time and don’t rush. It pays to do your homework.

First step: find a firm