The content industry is witnessing disruption on a grand scale. Competition between brands for users cuts across platforms, across borders, and affects all demographics.

TV networks are competing with on-demand streaming. Newspapers are fighting for readers with social networks and viral websites. And new platforms are emerging.

How can content brands survive and thrive in this chaotic landscape? EY is working with the most innovative global content producers and distributors to identify the traits of success across all verticals.

“We believe the lessons are universal,” says Rahul Gautam, technology, media and telecommunications leader at EY, UK and Ireland. “The market will support different business models, but the winners will exhibit common characteristics. Whether you are in video streaming, news, music, telecoms or the movies, the principles are a blueprint for growth.”

The first trait is scale. Simply being larger than rivals confers advantages in a number of ways. Content creators want to broadcast their artistry to the largest number of fans, so they want to work with the largest distributors. They want the benefit of aggregated audiences and the ability to access these audiences efficiently.

Consumers have a similar outlook. They want to access the widest variety of content, so they perceive the top-ranking brands as the default choice. Niche players can prosper, but usually by picking up artists and consumers who need something out of the ordinary.

Size translates to the ability to invest in the product. For example, movie-streaming brands are able to allocate huge budgets to bespoke projects. Their size means they even out-compete national broadcasters in terms of new content spend. Scale becomes a virtuous circle, in which the rich get richer. Smaller content owners are squeezed out.

The second quality is a laser focus on the customer. “Standards are now sky high,” says Mr Gautam. “Consumers expect a seamless, frictionless and personalised experience across all devices. If it takes 30 seconds to log on, forget it. If payment is troublesome, you can expect users to abandon you. Content brands ought to know this, but very few excel.”

Constant focus is needed because expectations are always rising. If a customer has been watching a TV show on a tablet, they expect to be able to switch to a laptop, smartphone or other device and continue where they left off. It is simply expected. Yet not all content providers offer this.

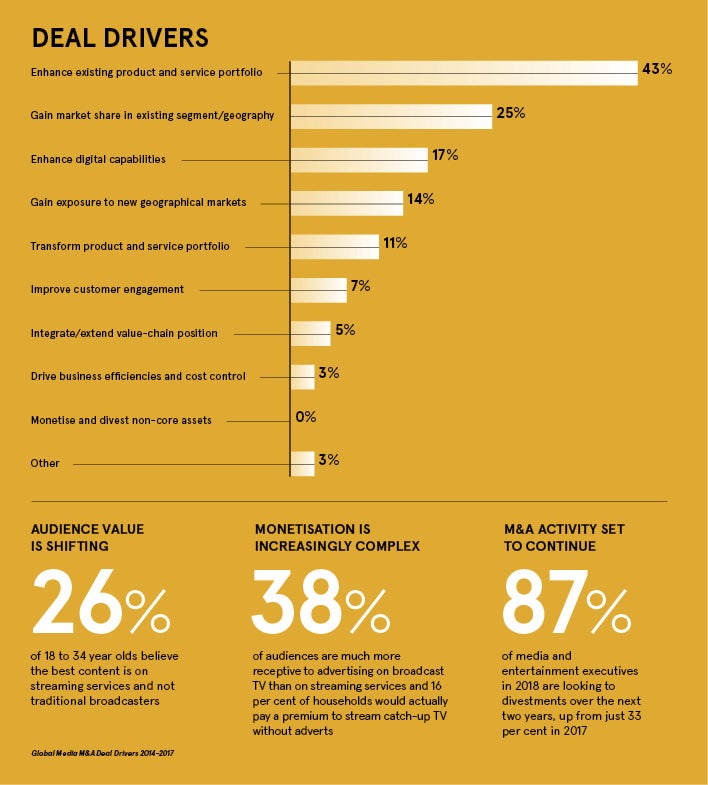

The user experience (UX) must be optimised for the customer. Multi-variate testing can refine the UX over time, but sometimes bold decisions need to be made to impress users. A survey by EY revealed 38 per cent of audiences are much more receptive to advertising on broadcast TV than on streaming services and 16 per cent of households would actually pay a premium to stream catch-up TV without adverts. Only brands with a profound understanding of the preferences of their customers can get the big calls right.

Third is a talent for innovating in delivery, not merely with the content itself. For example, the boom in smart speakers in the home offer brands a new route to audiences. Agile content owners have developed apps to integrate with these smart speakers. Now they are able to reach tens of millions of new consumers through an innovative and brand-enhancing medium. Early movers stand to be disproportionately rewarded.

Creative thinking around delivery means experimenting with new technologies. Virtual reality (VR) is an emerging field in this regard. Sports-betting companies have toyed with VR viewing experiences. Now you can see what the jockeys see as they leap over the penultimate fence at Aintree. Is it a game-changer? It’s too early to tell, but the best content brands have a track record of exploring new delivery channels.

Also there is the opportunity to transform traditionally relatively niche sports, such as cycling or horse racing. Mobile camera and internet of things technology can now capture moments, feeling and facts from sports which were once viewed statically. This not only enhances the customer experience, but also the opportunity to add commercial value by providing more real-estate space for advertisement or brand enhancement.

Scale, focus on the customer and innovation in delivery: these three qualities are found in all leading content brands. Naturally, the mission for challenger brands is to improve their performance in each category.

Scale, for example, is easy to target, but hard to achieve. “We see M&A as a great way to build scale fast,” says Will Fisher, EY’s Transactions Advisory Services global media and entertainment leader. “Over the past four years, the largest driver of M&A has been to enhance the product or service portfolio. And more than two thirds of deals have been to gain market share or build in new geographies.”

Raising finance is a part of this drive. Capital can be used for M&A, to fund new content, to invest in R&D or marketing. Divestments are a popular method of raising cash. In 2018, 87 per cent of media and entertainment executives are looking to divestments over the next two years. That is a significant increase on just 33 per cent in in 2017.

The three qualities will apply to each company in a different way. Even the idea of “winning” will vary. “You can only define winning when you know your core proposition,” says Mr Fisher. “Do you want to maximise viewer numbers to convert that to ad revenue? Is content a way to sell something else, such as subscription to an affiliated service? It’s a fundamental debate you need to have.”

In the heat of battle, brands often lose sight of their core objective. For example, social media is a hot topic and brands are investing in building followings on the main platforms. But do social media numbers contribute to the bottom line? Consumers are often being pushed to a third-party site, making monetisation hard or impossible.

“The market will support different business models,” Mr Gautam concludes. “But it is clear that the winners possess common qualities. Scale, a focus on the customer, and product and service innovation are the three key capabilities. It may shock content creators and distributors, but without them, you can have the best content and still lose.”

For advice on building a content strategy please contact Rahul Gautam, EY’s UK and Ireland technology, media and telecommunications leader [email protected] or Will Fisher, global media and entertainment leader, EY Transaction Advisory Services [email protected]