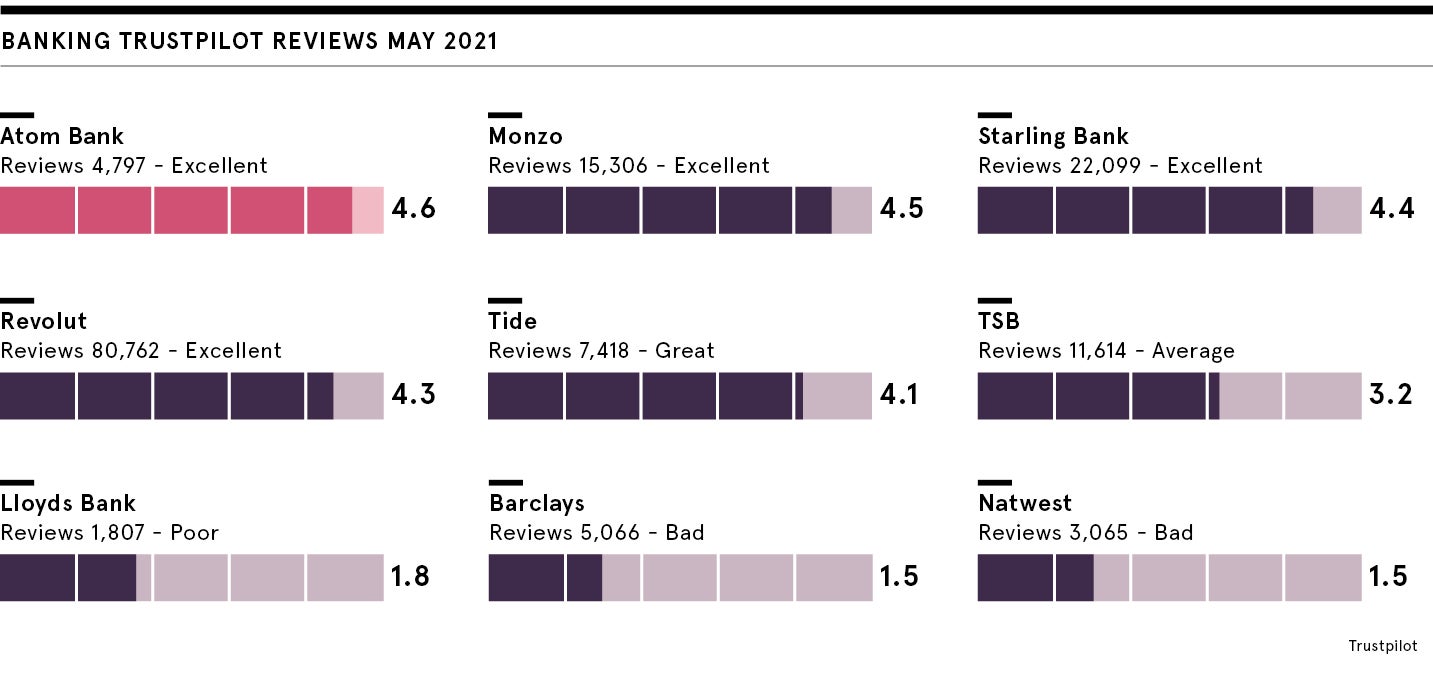

It’s long been clear that the traditional model of retail banking is broken but, as the rapid rise of neobanks shows, millions of consumers now want change.

These digital-first businesses have lower overheads than traditional banks as they do not have to splash out as much on property or people.

But there’s a further step that some of them are making, to jettison unprofitable services and focus on delivering a smaller range of services more effectively and profitably for customers and themselves without cutting corners.

Alone among the recent wave of new entrant banks, Atom is focused on making the chunkiest household and SME lending decisions as easy as possible. It has an enviable reputation as a digital mortgage lender, having helped UK homeowners with over £3bn of mortgage sales since 2017. And now it is on track to have £1bn of business lending on its balance sheet by the end of the year.

But the secret to its success is as much in what it isn’t doing as what it has done. Atom is not a current account bank, and according to Edward Twiddy – its chief customer officer and co-founder – that is what makes it able to beat off the competition from both high street lenders and rival neobanks.

Giving more, taking less

The reason is that all of us – well, nearly all of us – pay nothing when we go to the cashpoint, buy our shopping on a debit card, or set up direct debits or standing orders. This is not the case for people who are not paying off their credit cards every month, or in and out of unauthorised overdrafts.

But in the UK the vast majority of people get current accounts for free, despite them being expensive to set up and run and much less valuable to the banks in terms of the free float of deposits that sit in them overnight and at the end of the month.

“There’s a political debate to be had about whether competition is well served by having a zero-priced product at the heart of banking, but it will be a brave move to require the industry to start charging everyone for their debit card,” says Twiddy.

“In the meantime, Atom’s insight is that by taking the cost of current accounts away, it is freed up to offer better rates on savings accounts, mortgages or business loans, while investing more in digital innovation.”

With lower costs and a simpler model, Atom becomes a strange kind of business – giving more to its customers and taking less. It is currently offering competitive rates in mortgages lending.

Shaking up business lending

Combine great mortgage rates with very competitive savings rates – Atom offers 0.85% on a 2 Year Fixed Saver – and the advantages for personal customers are clear. But while consumers are increasingly aware of the benefits offered by neobanks and are moving away from the idea of being banked with a single business in order to find the best deal, Twiddy says that too many UK small businesses still miss out on the best opportunities.

“Mr Mainwaring is no longer the gatekeeper to any of us getting a mortgage, and everyone can get independent advice from a mortgage broker these days. This democratisation of decision-making and re-balancing of power between banks and consumers has some way to go yet, but it is at least further ahead in personal banking than in business banking.”

Atom’s own commercial lending is, like its mortgages, only sold through networks of independent brokers across the country. That might seem like an odd choice for a direct digital lender, but Twiddy explains: “While we might, at some point in the future, sell our mortgages and commercial loans direct to customers, we are very happy to go toe-to-toe with the biggest lenders in the country and to sell our loans through brokers who are not committed to sell an Atom loan and instead are there to inform and protect the customer.”

Atom lends SMEs up to £5m a time with a typical loan size of around £800,000. It also guarantees transparent pricing, no loading of fees and no haggling – all areas in which traditional lenders score poorly.

It is perhaps not surprising that the neobank recently achieved a net promoter score of +88 in a recent survey of its business banking customers, highlighting customers’ willingness to recommend it to others. UK high street banks typically score in the teens in such polls.

Positive and proactive

Atom also has a strong reputation for helping and supporting its customers with any questions or through bad times. During the pandemic, its positive and proactive approach came into its own for those customers who needed help with repayments, whether they were businesses or mortgage holders. Atom was also approved to offer government-backed loans via the Coronavirus Business Interruption Loan Scheme and is now part of its successor, the Recovery Loan Scheme.

In addition, Atom recently announced a partnership with specialist business lender Funding Circle which will see another £350m of loans offered to UK SMEs this year. The aim is to make it simpler for SMEs to access finance, with applications taking an average of six minutes and lending decisions just nine seconds thanks to the use of advanced machine learning capabilities.

Atom has cut its teeth during one of the most turbulent periods ever in the UK. Coming out of that on the cusp of breaking even and with a resilient and contemporary technology stack now firmly in place, Twiddy believes the business is very well placed to play its role.

“At the heart of banking there’s a solid truth that savers and borrowers both need a good deal and anything that gets in the way is a drag on them and on the economy. As other fintechs and payments specialists come to market and create more ways to manage the day-to-day buying of goods and services, we’ll be here to make sure that the people who want to own their own homes and grow their businesses can find a bank for them.”

For more information please visit atombank.co.uk

Sponsored by

It’s long been clear that the traditional model of retail banking is broken but, as the rapid rise of neobanks shows, millions of consumers now want change.

These digital-first businesses have lower overheads than traditional banks as they do not have to splash out as much on property or people.

But there’s a further step that some of them are making, to jettison unprofitable services and focus on delivering a smaller range of services more effectively and profitably for customers and themselves without cutting corners.