The UK’s mid-market companies are the unsung heroes of business. Despite representing just 1 per cent of companies, research by law firm Gowling WLG forecasts their contribution to the economy will reach £335 billion by 2020, an 18 per cent rise on 2015. Much of that contribution will come from international expansion.

The UK’s mid-market companies are the unsung heroes of business. Despite representing just 1 per cent of companies, research by law firm Gowling WLG forecasts their contribution to the economy will reach £335 billion by 2020, an 18 per cent rise on 2015. Much of that contribution will come from international expansion.

Around 35,000 companies make up the UK’s mid-market and 62 per cent of them plan to increase investment in exports beyond the European Union because of Brexit, according to a survey of 500 medium-sized businesses by Mills & Reeve. But Brexit isn’t the only driver of expansion.

Cloud computing and mobile technologies have removed barriers that previously made entering new territories too expensive and complicated to consider for many mid-market companies. The ability to transact on a world stage is much easier and as such, opportunities for growth and diversification overseas are bigger than ever before.

A greater multinational footprint, specifically outside Europe, brings new and arguably heightened risks.

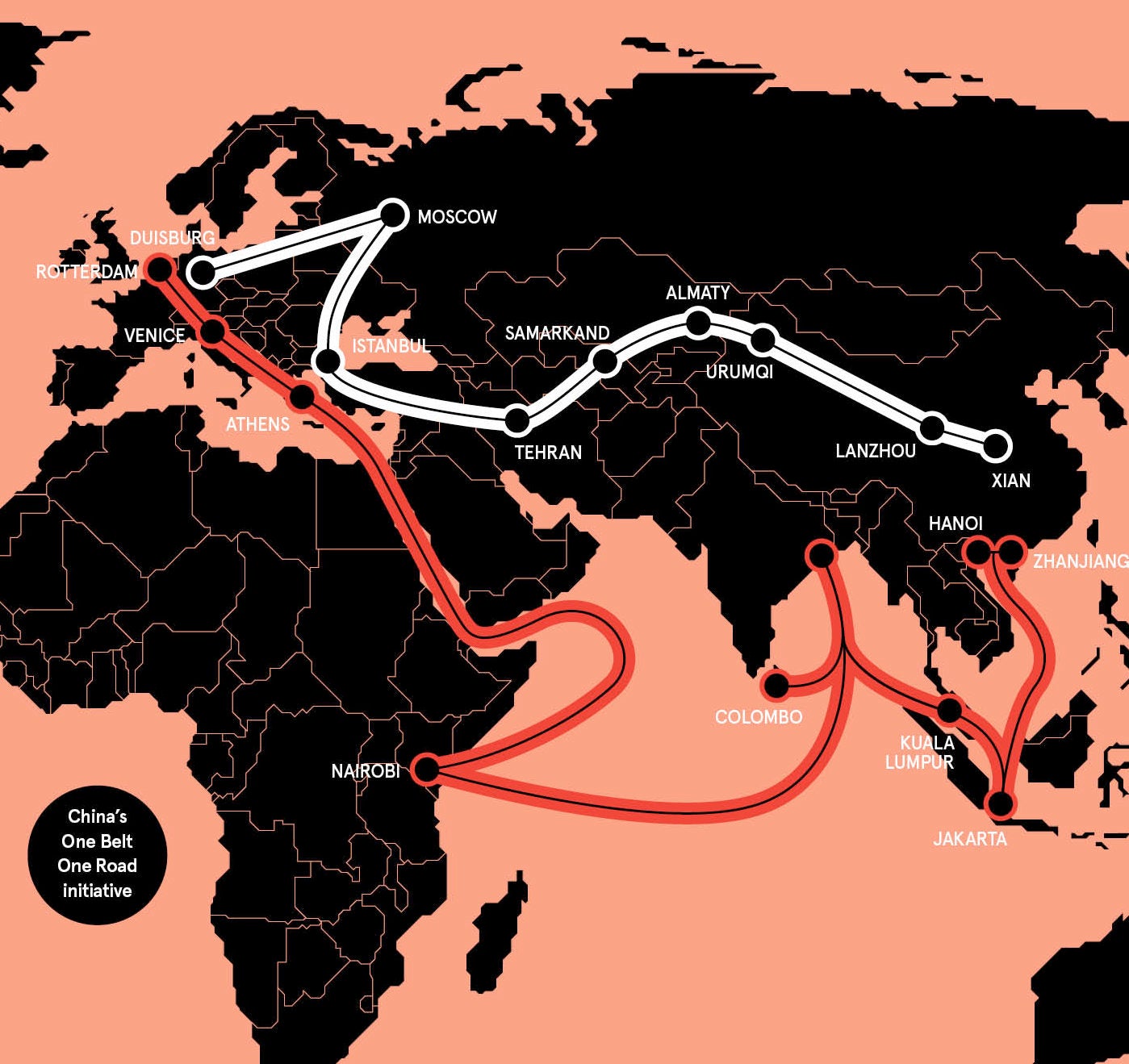

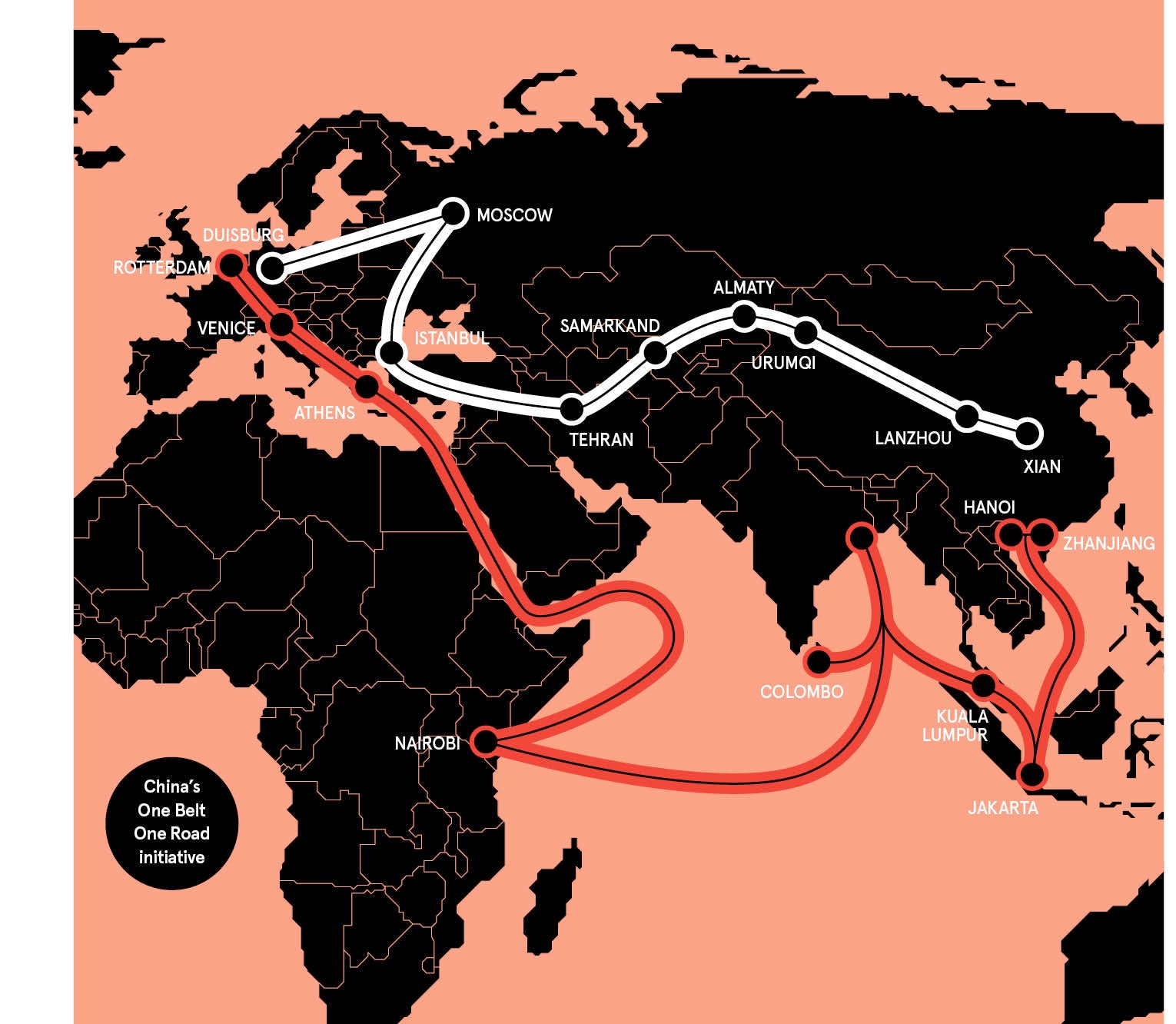

Many mid-market companies are increasingly looking to the Far East for expansion and to China in particular, with the One Belt, One Road initiative opening up a wide range of opportunities and markets. While UK mid-market companies might be largely undeterred by the prospect of a US-China trade war, they need to bear in mind that the laws and exposures they face outside Europe are often very different to what they’re used to at home.

Businesses need to work with experienced partners who can help them deal with the complexities of this risk landscape

The ability to navigate and manage these multinational risks is increasingly important, particularly when companies are expanding in lesser-known or emerging markets. So businesses need to work with experienced partners who can help them deal with the complexities of this risk landscape.

“The mid-market space is so diverse and organisations are even braver today,” says Sara Mitchell, head of corporate division, UK and Ireland, at insurance firm Chubb. “The world feels a lot smaller for business because of the infrastructure that’s in place, whether it be through insurance or other financial institutions. Companies are utilising the experience they’ve got in different sectors and finding it less frightening to grow in another country.”

Mid-market companies operating on a multinational footing for the first time need to tackle the local regulatory requirements for insurance policies and cover, and what needs to be evidenced in each territory. Most mid-market companies don’t have an insurance department to look after this so require somebody to do the heavy lifting for them.

The prospect of a large uninsured loss is not the only thing that keeps executives awake when entering new territories; the risk of reputational damage can be just as terrifying. Such damage can be easily suffered if the company doesn’t have a policy which is legal or valid when trying to operate in other regions. Businesses also need guidance on taxation and local premium payments issues.

“Particularly outside of the EU, you can’t wave a piece of European paper and expect that to be accepted in the US, for example,” says Mark Roberts, property and casualty (P&C) chief underwriting officer, UK and Ireland, at Chubb. “Mid-market companies want an insurance policy that is aligned with local regulations and local expertise.” With operations in 54 countries and territories, Chubb is able to tap into local offices to provide local risk engineering support and claims handling.

Companies also need to consider the new risks they are likely to face in unfamiliar environments. These could include natural catastrophe, new and previously unknown liability exposures, terrorism and the growing threat of cyber. Natural catastrophes and cyber rank among the biggest and potentially most damaging risks for businesses operating in the Far East.

Wherever organisations have operations, they have computer systems that can be exposed so it is of paramount importance to ensure those systems, as well as any data belonging to both the company and its customers, are secure. Damage following a data breach can be severe both financially and reputationally. Strict new laws on cybersecurity and data privacy have been introduced recently in several countries in the Asia-Pacific region.

“Data regulations can and will vary in different territories and we can advise our clients on the exposures in this regard, while also ensuring that their insurance covers are reflective of this,” says Karen Strong, UK and Ireland head of industry practices at Chubb. “Cyber is such a short word and it’s bandied around easily and increasingly, but there are so many different elements to cyber-exposures, both for the client themselves and for the impact on their customers. This introduces first and third-party risks for our clients.

“An example of growing exposures in this regard is the fact that many mid-market companies utilise hosted services for the efficiencies they provide while enabling growth into new territories and this introduces new concerns to a company’s risk register.”

If the worst does happen, it is important to be able to rely on an insurance partner that has the ability to pay claims promptly and locally.

Companies also need to consider issues in specific territories. As well as dealing with language and cultural changes, becoming more global can open up heightened litigation risk for product liabilities. Companies exporting products abroad for the first time or opening up overseas offices need to be aware of additional and potentially more onerous obligations.

The need to label goods correctly for the local market, warn about possible hazards, and comply with the relevant local safety and regulatory standards must be considered.

To deal with this, Chubb’s multinational experts from underwriting and risk control are able to provide advice on a country-specific basis.

A policy sold in the UK would not necessarily be fit for purpose somewhere else, so Chubb has local offices and operations in many of the countries that mid-market companies are expanding to, providing people on the ground who can help them navigate the legal and regulatory environment.

“For a lot of our clients who buy directors and officers (D&O) policies, they actually buy what we call local policies,” says Hilda Toh, UK and Ireland financial lines manager at Chubb. “So if they’re a UK mid-market company and they’re setting up operations in China, India, Japan, Mexico or wherever it may be, we can help them with issuing a D&O policy for that local jurisdiction as well. That local policy would be written in a local language, and with local laws and regulatory environment taken into consideration.”

Suresh Krishnan, head of global accounts division, Europe, at Chubb, concludes: “An off-the-shelf single-policy response is simply not prudent, particularly in a multinational context. Clients need partners with the capability to craft solutions with local policy, local risk engineering, local claims and local compliance capabilities that fit an individual company’s profile, tailored precisely to its specific needs.”

For more information please visit chubb.com