SPONSORED BY dacadoo

The insurance industry is experiencing a sea change more fundamental than any seen in decades, with a PwC study showing three in four insurance companies are convinced that at least some parts of their business are at risk of disruption. Consumers’ shifting demands are combining with digital innovation to transform analogue business models, with record funding being allocated towards insurtech developments, even against a backdrop of the coronavirus pandemic.

Just as Amazon has revolutionised retail, the ways in which insurance services function are being completely reimagined, leading to the birth of integrated insurance operators offering consumer-centric, digital health ecosystems that meet new demands and build loyalty. The digitalisation and integration of these services is far from complete at many organisations and, as an Accenture report observes, in the insurance sector “enterprises have not yet re-oriented to just how personal and meaningful technology has become in most people’s lives”.

“Many insurers have failed to fully grasp the magnitude of the changes that are happening,” explains Peter Ohnemus, chief executive at the insurtech firm dacadoo, which provides digital health engagement and health risk assessment systems to insurers. “Few of the current operators were founded recently or are operating based on today’s consumer behaviour; they don’t reflect the expectations of the mobile-first, digital and flexible generation.”

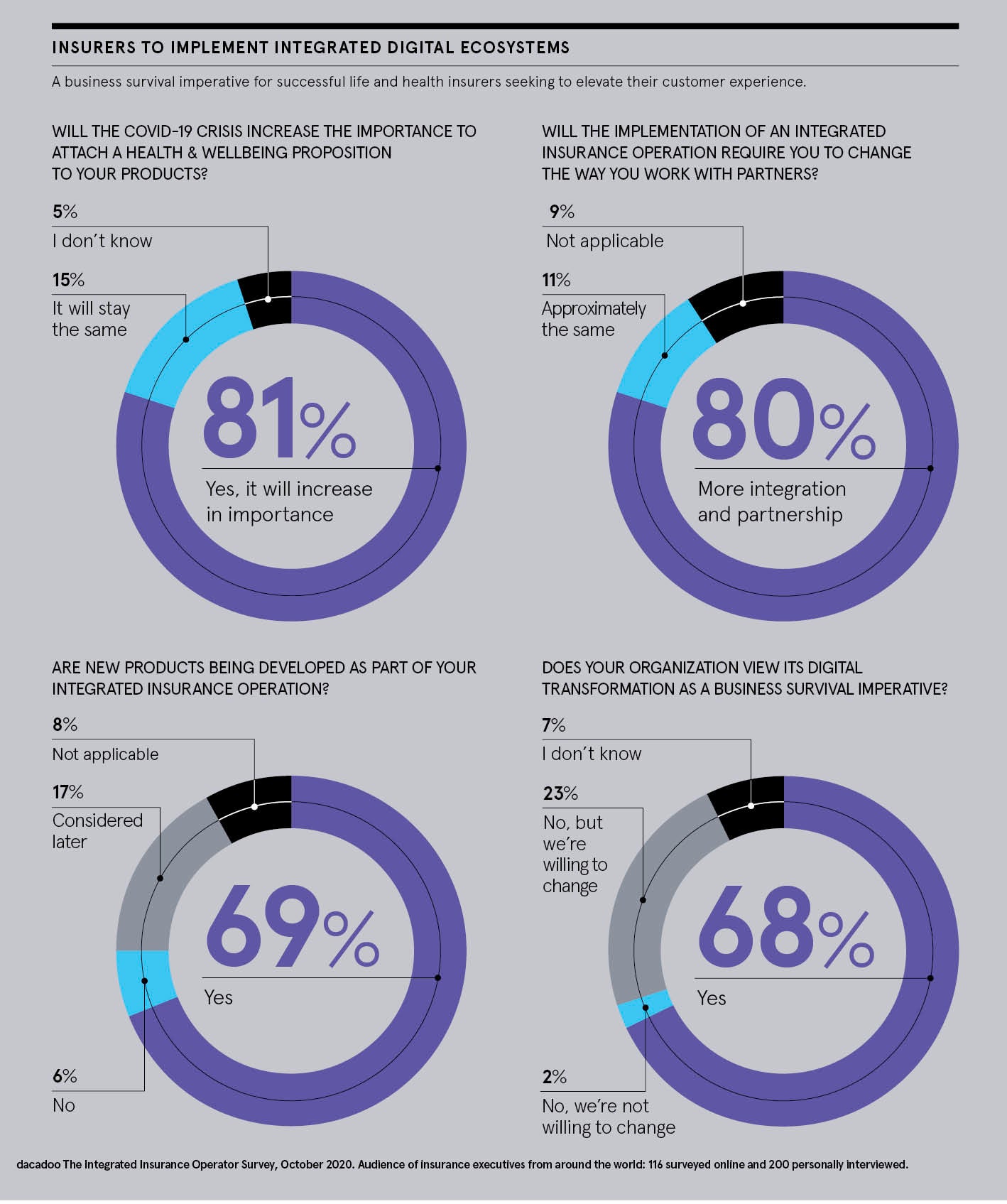

A global survey of more than 300 insurance executives, conducted by dacadoo, shows that while eight in ten recognise COVID-19 as driving a need to add meaningful health and wellbeing propositions, most feel their organisation does not see an innovative digital health strategy as an imperative business commitment.

There are potentially significant risks for insurers in overlooking new expectations among their customers. While insurers have been seeking to cut underwriting and processing costs, given customers’ longer life expectancies, newer considerations represent threats to their business models too. A recent cross-industry report by Deloitte points out that smart organisations are moving away from efficiency-first mindsets towards elevating consumer experiences. As customers look for deeper connections with brands, innovation must be built around their experiences.

Contemporary consumers want to buy directly on their smartphones from trusted operators, and they want personalised, easy-to-find and engaging offerings relevant to their lives and their health. They expect fitness and wellbeing to be part of a larger insurance landscape that draws from connected objects, health devices and biological data, and provides offerings based on smart data integration and automation.

Indeed, the dacadoo research reveals that 86 per cent of insurers place a medium or high priority on becoming an integrated insurance operator. The pressures brought by COVID-19 have added further impetus to trends towards integration. Yet only a third of insurance companies currently work with digital health engagement platforms to harness the data they need to deliver more personalised services and gain the trust of their customers.

“The insurers that will grow and define the next ten to twenty years of insurance will be integrated operators. They know how to work with the whole consumer life cycle, integrating distinct but relevant offerings such as health and wealth, and they will drive the disruption from within,” Ohnemus explains.

Those failing to innovate could soon see tech giants eroding their share of the market, with the likes of Apple, Facebook and Google going after the $8 trillion spent globally each year on healthcare. Worryingly, only a quarter of insurers surveyed say they are first to market with innovations. The few that are ahead, by contrast, are already collecting data from a range of sources such as wearables, third-party systems, mobile apps and health records to generate actionable analysis.

The COVID-19 crisis has also prompted some reconsideration of the role of businesses and how they might serve a broader range of stakeholders. This could include putting greater emphasis on meeting the needs of not just customers but employees, suppliers, local communities and society at large, according to the World Economic Forum.

“Insurers need to participate much more meaningfully in the stakeholder economy,” argues Ohnemus. “There must be a recognition of what people really need or want when it comes to their health, insurance and digital interactions. Insurers should become the platform operator around healthy living, sports challenges, health concerns, financial coaching, mental wellbeing, telemedicine and beyond.”

Rather than building their own technology, insurers should focus on honing expertise while choosing the right data-expert partners and suppliers to work with. Those surveyed by dacadoo recognise the danger, with 70 per cent worried about their internal capabilities in these regards.

The integrated insurance operator that orchestrates the ecosystem will derive rapid growth and larger profit margins

Insurers can become the orchestrators of new ecosystems and data lakes, providing platforms integrated with third parties, including healthcare providers, fitness clubs, travel agencies and retailers. This will enable them to profit from scale and automation. Eight in ten expect closer partnerships will be necessary for success and 60 per cent will add more partners. In a world of nano-sensors and shared analytics that assess individuals’ health and risks, trust is essential.

“For the insurer, building and leading such an ecosystem means they will have a unique understanding of a consumer’s life, while the consumer gains relevant health scores and personalised lifestyle navigations,” says Ohnemus. “Such micro-services and lifestyle-based insurance products will become extremely popular, as long as customer trust and privacy are retained and a good mobile experience is delivered.”

The overall goal is to create larger markets and growth opportunities, as happened with smartphones, where the exchange of information and services represents a significantly more profitable opportunity than simply selling handsets.

“There will soon be a multi-trillion-dollar platform economy for insurers,” Ohnemus concludes. “The integrated insurance operator that orchestrates the ecosystem will derive rapid growth and larger profit margins.”

Download the full Integrated Insurance Operator report here.

To find out how to lead the new ecosystem as an integrated insurance operator please visit dacadoo.com