The ubiquity of smart devices combined with fintech innovation has driven a dramatic behavioural shift in how consumers wish to make payments. With an ever-increasing number of payment options available, and the smooth digital experiences that consumers have become accustomed to, there is now a much higher expectation for speed and ease of use for payments.

In a world where people crave instant gratification, it’s clear consumers don’t want to wait for a credit card payment to clear or for a bank transfer to complete. Transferring money through traditional methods simply takes too long for today’s always-connected culture, signalling significant growth in solutions that enable instant payments.

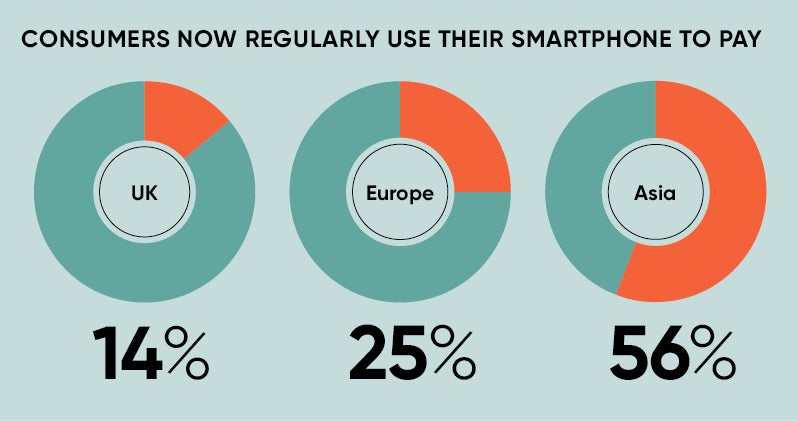

Two thirds of UK consumers have made a contactless payment since the technology was introduced ten years ago, according to Visa, while benchmark data from ACI Worldwide and Aite shows that 14 per cent of UK consumers now regularly use their smartphone to pay. This grows to 25 per cent in other parts of Europe and 56 per cent in Asia. But this is just the tip of the instant payment iceberg.

“Most instant payments are 100 per cent secure, providing reassurance for those who are reluctant to put card details in the public domain,” says Koen Vanpraet, chief executive at PaySec, whose parent company Sappaya owns an ecosystem of service providers that specialise in instant payments. Sappaya’s payment gateways, including PaySec and Pago, aggregate the best payment solutions for a given territory, while its cashless payments solution, tappit, is changing the way events and entertainment venues accept cash.

“Instant payments are also far less costly than card transactions, avoid the risk of chargebacks for the merchants and are also facilitating new trends such as cashless NFC [near-field communication],” Mr Vanpraet adds. “Improved technology gives consumers what they have long been demanding – a simple and quick way to complete transactions.”

This rise in instant payments and the evolving consumer attitudes have triggered substantial investments in functionality, coverage, security and customer experience by the fintech industry. Alternative payments are disrupting the market and ensuring credit cards are not the only option for consumers and merchants, while pressuring legacy financial institutions and banks into embracing the new world of commerce.

Meanwhile, regulatory bodies and existing card schemes are stepping up their efforts to deploy new laws and industry standards that better protect clients, and foster more partnership and industry-wide collaboration. PSD2, the European Union’s Revised Payment Services Directive, provides larger and safer access to a broader set of payment options and functionality. It will enhance the creation of open standards and a set of technology products that will be more user friendly, integrated and comprehensive.

The new directive will further increase competition in the payments industry as it breaks open banking and allows other players into what was previously something of a closed shop for high street banks. This will lead to more choice for the consumer and further localised regulation. Consumers will be able to handle more financial transactions and payments through the same interface or app.

While 89 per cent of consumers are unaware of how PSD2 will affect them, one in five surveyed by Intelligent Environments said they think it will be more convenient than ever to manage their money and that they’re looking forward to being able to manage multiple bank accounts from a single app.

“By forcing existing banks to open their platforms to third-party payment providers, PSD2 will allow more fintech companies to connect to bank data and applications,” says Mr Vanpraet. “The result will be a more comprehensive, efficient and consumer-friendly environment, which will foster the usage of instant payments even more.”

Fast and secure instant payment like direct bank transfers and direct debit, as well as cashless on-the-go devices, such as wearables and mobile wallets, are set to take off massively in the next three years. Usage of these payment methods won’t necessarily slow the use of traditional credit cards, but they will certainly grow much faster.

The payments industry has changed more in the last decade than it did in the whole previous century and it’s on an exponential curve. The industry is very fractured and that trend will continue, especially in light of PSD2 and the rise of cryptocurrencies. This revolution is happening in every country around the world, not just Europe, so it will take a long time for real patterns to emerge, and providers and technologies to win out.

As the relative share of instant payments rises in the coming years at the expense of traditional payment methods, card schemes and banks will continue to invest in providing faster solutions and new payment options to keep up with the market.

Consumers in underdeveloped countries that lack traditional infrastructures will jump straight to the latest innovations, but more mature countries will have to go through a technology development cycle to migrate to the new landscape.

Payments need to be fast, secure, cheap, easy and instantaneous, and the future will be defined by a huge increase in customer choice

“While the West dawdles its way to a payments evolution, countries such as China and Indonesia are having a revolution with a raft of new solutions that work without banks,” says Mr Vanpraet. “Whether it’s WeChat’s payment solution that includes peer-to- peer payments, LINE in other parts of Asia or Indonesia’s Go-Jek wallet, which can be used to pay for rides, shopping, food delivery and even a massage, underdeveloped countries are the ones pushing the envelope because the need is so much bigger.”

Payments need to be fast, secure, cheap, easy and instantaneous, and the future will be defined by a huge increase in customer choice. Consumers will spend how they want, when they want and won’t have to pay for the privilege. They will start turning away if the payment process is not what they want, so ecosystems like Sappaya will be critical in providing the products and much-needed support for merchants in meeting these expectations.

For more information please visit