Data, data, everywhere – industries across the globe are now swimming in the stuff. The risk management and insurance industry is no different. Many of us are aware that data should be put to good use, processed and interpreted intelligently, but the burning question for most corporations and insurers is how?

The customer service industry is awash with examples of how consumer data is used effectively to personalise experiences, brands and product offerings. However, practical examples for the risk management and insurance industry are harder to find.

“Big data should be a key tool for our industry, but it’s become a nightmare,” says Willem van der Hooft, business development director at Van Ameyde, a Europe-wide company that has been working on claims management solutions since 1945.

“It’s one thing to collect and interpret as much data as you can get your hands on, but to do it in a way that makes a difference to your business goals is the challenge. End-to-end digitisation helps. The more the claims process is digitised, the more data you have available, the more insight you will have for risk management and market segmentation.”

Van Ameyde is at the forefront of the revolution in IT-driven claims and risk-related services, successfully modelling analytics programs for risk managers and insurance providers. The company has found that data analytics serves many purposes with respect to claims. For instance, loss statistics allow companies to identify repetitive causes. Once these are solved you can reduce their frequency and save money in the process.

“This requires complete insight into all losses wherever they occur,” says Mr van der Hooft, whose company has 46 offices in 28 countries. “The same goes for more sophisticated predictive risk models. You need a complete and consolidated data set you can mine for information.”

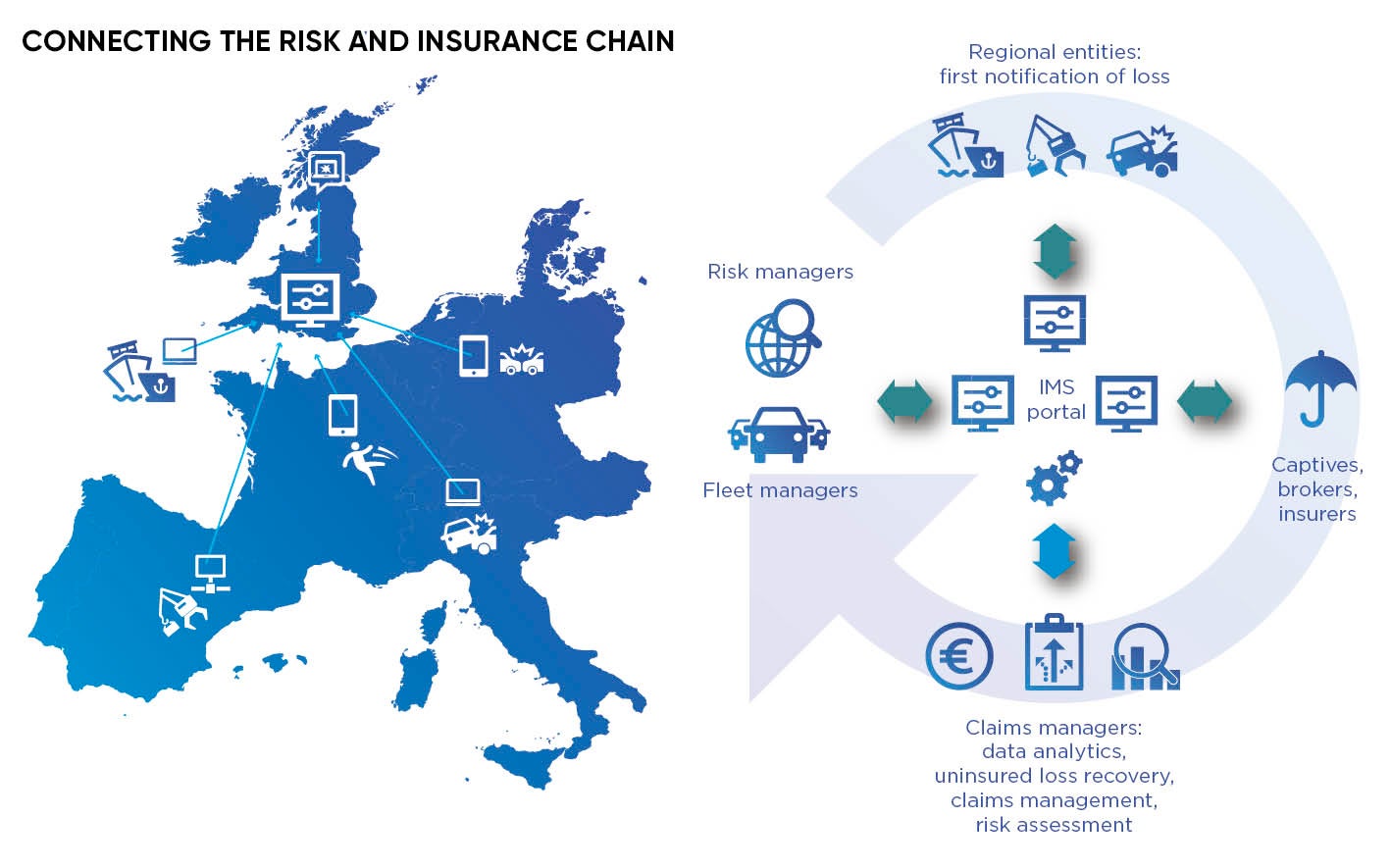

That’s why Van Ameyde set up its pan-European Incident Management System (IMS). This is a platform that all Van Ameyde’s customers and their suppliers are connected to. The aim is to process data from all incidents across Europe, at scale, in a uniform way. Information ranging from losses to policies and customers’ personal details is logged.

“IMS is empowering industry players’ insight to make informed decisions. This system is also the foundation for our analytics capabilities,” says Ruben Snepvangers, data analyst at Van Ameyde.

Van Ameyde has created a predictive risk model for a multi-national car hire company. The results are to be used in the company’s pricing strategy, including insurance premiums offered to clients.

“We’ve created a model that encompasses losses relating to age, car model, insurance cover, days hired and location. Despite limited sample sizes and data points, predictions using this model are correct in 70 per cent of cases. When segmenting low and high-risk customers, the model had an even higher success rate,” says Mr Snepvangers.

Van Ameyde found that the key to designing a successful predictive model involved setting clear goals. “We asked our client the question what exactly do you want to achieve? A clearly defined end-game makes all the difference when determining what information to use in the analyses,” Mr Snepvangers explains.

Risk profiles are also used in the insurance industry. This enables insurers to segment consumers based on their desirability and design customised solutions. It involves using enriched customer profiles, which are based on policy details, insurance application information and any claims someone may have had. All this data is used to build up a detailed picture of each customer.

The insurer could take on a new role as the policyholder’s risk manager offering advice to reduce claims

The type of insurance policies each of us takes out tells us a lot about our respective lifestyles. If you combine claims and policy information you can see that there’s a connection between risk appetite, defined by the level of insurance taken out, and the actual risk posed, defined by the number and extent of losses. Profiles can now be enriched further by additional information that’s available from voluntary sharing schemes such as car telematics.

“We tend not to speak of big data because we don’t actually use all the data available. While customers may be willing to share data if they see substantial benefits, such as lower insurance premiums, sensitivity over privacy is crucial,” says Mr van der Hooft.

“In some European countries, it’s perfectly acceptable to use social media to detect fraud, but in others it’s against the law. Mining data from social media for marketing segmentation purposes, even if it’s legal, may still raise eyebrows among some potential customer groups. A voluntary survey may work just as well.”

Detecting fraudulent inquiries is also a big industry issue. Van Ameyde now uses machine-learning algorithms. These improve the company’s ability to detect fraud, but they also predict possible deceitful behaviour. All this information is then fed back into the analytical model.

Creating risk profiles for certain customer groups also allows accurate market segmentation and the design of more personalised services and pricing schemes. Take safe-driving and usage-based schemes for motor insurance, these have paved the way for more accurate tariffs for motorists.

Van Ameyde believes there is more the industry can do with risk profiles. The insurer could take on a new role as the policyholder’s risk manager offering advice to reduce claims.

“Take those people who live in flood-risk areas, they could be advised to adopt measures at their property that will increase flood resilience and at the same time reduce their premiums, such as raising thresholds, putting in airbrick covers or storing expensive household items on the first floor rather than in the basement,” says Mr van der Hooft.

“In the risk management industry, the accuracy of pricing hugely impacts the risk transfer strategy. Get it right and both risk managers and their insurance providers benefit. The key to all this is information. If data is structured, centralised and reliable, you can make comprehensive risk assessments. You will also have a complete picture of the losses incurred throughout the company. This is the basis for a robust pricing, risk mitigation and risk management strategy.”

To find out more call in at booth 29 at the Airmic 2017 conference or visit www.vanameyde.com