The insurance industry is being transformed through new technologies that are enabling more customer engagement by powering a new generation of products built on usage and behaviour-based insurance (UBI) data.

The digitisation of insurance, particularly in motoring, radically changes the relationship between insurance companies and their customers. Such products include pay-as-you-drive (PAYD) and pay-how-you-drive (PHYD).

This new wave of products not only allows insurance companies to measure and gain detailed insights into customer behaviour, but also to influence driving behaviour by using advanced engagement mechanisms from companies such as Amodo, whose mobility platform solutions are leading the UBI charge.

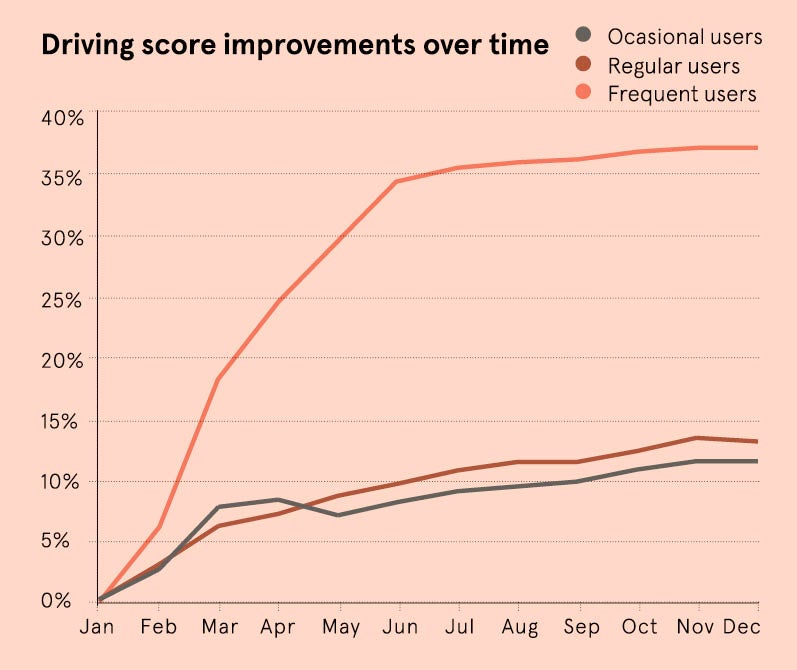

To test the link between customer engagement and driving behaviour, Amodo analysed the behaviour of a range of drivers over a 12-month period. Participants installed a UBI smartphone app that generated a driving safety score based on factors such as speeding time and harshness of braking, acceleration and cornering. An optional recording function was stimulated by gamification mechanisms such as individual and group challenges, competitions and reward contests.

The most frequent users of the app, who on average recorded 34 per cent of their journeys, increased their driving safety score by almost 40 per cent over the 12 months. Drivers classified as “regular” users of the app, using it on 16 per cent of their trips, increased their score by 15 per cent, while those who only used it occasionally, on 8.5 per cent of their trips, improved their score by 14 per cent.

“This confirms the positive link between customer engagement and driving behaviour,” says Marijan Mumdziev, Amodo’s chief executive. “The UBI product offered to the drivers used balanced distribution of mechanics for short-term, mid-term and long-term engagement, all of which are essential in engaging drivers over a longer period of time and effectively changing their driving style.”

Through the results of the research, it’s clear that driving behaviour data can become a powerful tool for achieving the business goals of insurance companies, which are uniquely aligned with customer goals in terms of focusing on safety.

Amodo’s research also reinforces the assumptions about engagement indicated by other studies, such as a 2013 survey by Tower Watsons in which 60 per cent of customers interested in UBI programmes said they would be willing to change their driving behaviour.

When asked how they might change if a UBI device was installed in their car, respondents listed sticking to the speed limit (71 per cent), keeping a safer distance from other vehicles (52 per cent) and driving more considerately (49 per cent) as the

leading adjustments.

Technology is enabling insurance companies to improve many aspects of their business

Technology is enabling insurance companies to improve many aspects of their business. Amodo’s research demonstrates how telematics technology can prevent risk by encouraging safer driving, benefiting both insurers and their customers.

“The key to successful risk prevention programmes in motor and other insurance products is customer engagement,” Mr Mumdziev says. “This doesn’t happen just by installing a smartphone app; it needs to be carefully designed, planned and then automated with the appropriate engagement platforms such as Amodo.

“It is nothing short of a science to build a successful customer engagement programme. Our customer engagement design is built on top of lots of behaviour data insights and patterns that we use in combination with communication strategies, gamification mechanisms, social tools, incentivisation plans and others to measure and change customer behaviour over a longer period.”

Insurers can also find significant value in leveraging driving behaviour data not only for risk prevention, but also for product development and marketing, thereby gaining a better understanding on customer needs and respective segmentation.

Consumer interest in UBI and related value-added services presents a great opportunity for insurance companies. By relying on superior solutions and support to implement such products, insurers can gain necessary market advantage, and ensure a profitable and sustainable future.

For more information please visit amodo.eu