The emerging regulatory technology or regtech market, driven by artificial intelligence, is helping to reduce fraud in the financial services sector, but how is the so-called future of compliance computing progressing?

The emerging regulatory technology or regtech market, driven by artificial intelligence, is helping to reduce fraud in the financial services sector, but how is the so-called future of compliance computing progressing?

Stefan Sulistyo, co-founder of Munich-based risk-management-as-a-service company Alyne, overheard a director of a German bank talking about it having more than 1,200 employees tasked with compliance functions alone. Indeed, Deutsche Bank lists more than 1,000 positions in audit, risk and compliance.

There can, it seems, be little doubt that big financial institutions are throwing what Mr Sulistyo calls “an insane amount of people” at the regulatory compliance problem. “An informed estimate for financial institutions is now around 10 to 15 per cent of total workforce dedicated to governance, risk management and compliance,” he says. Unsurprisingly, he adds that the best risk professionals are in such high demand they are “as rare as unicorns and more expensive than their weight in gold”.

Mr Sulistyo says if you talk to London bankers, they are already hailing AI-driven regtech as a kind of magic silver bullet and saviour of the financial industry.

But can it really fulfil these expectations?

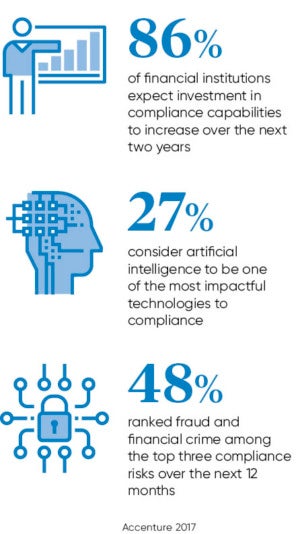

Nobody in the financial services sector would argue that the impact of increasing regulation and increasingly large fines for regulatory failures has built steadily over the last decade. Nor, for that matter, that risk and compliance is now one of the largest areas of spending within the industry. It hasn’t been exactly uncommon for banks to have increased their budgets over this period by 15 to 25 per cent a year in this area alone.

“It is now reaching saturation point,” argues Jeremy Doyle, associate partner with Watson Financial Services at IBM UK. “Continued spend is becoming untenable and there is increased urgency to find ways of reducing cost, while remaining compliant, protected and in a position to drive growth.”

Luckily, during this same period, the maturity of technology in cloud computing, machine-learning and artificial intelligence (AI) has accelerated dramatically while the entry cost declines. So are AI and machine-learning now driving the next generation of regtech solutions to reduce fraud in the financial services sector?

AI in finance

If machine-learning, a subset of AI that has been around for many years now, can help to identify complex and nonlinear patterns in the increasingly huge data sets within the financial services sector and by so doing create more realistic risk models, then surely it’s uptake is a given? After all, the single most effective method of preventing fraud is refusing the fraudster entry in the first place.

“In the financial services area, we see specific applications in insurance telematics – edge devices that send information against which insurers can evaluate and mitigate risk using machine-learning classifiers,” says Steve Wilcockson, financial services industry lead at MathWorks. This could be validating whether an alleged crash is a fraudulent claim or even convolutional neural networks – popular in machine-vision technology solutions – identifying counterfeit bank notes.

MathWorks surveyed financial risk professionals last year and Mr Wilcockson says they found that machine-learning use has quadrupled compared to a similar group surveyed in 2014. Which sounds good, until you learn that 60 per cent of respondents were still not actually using machine-learning; half of those have plans to do so in the next year.

Application of machine-learning is progressing at different rates across risk-taking buy-side firms and the more risk-averse sell-side. “On the buy-side, machine-learning techniques are often an extension of risk-factor analysis suites to differentiate from peers and rivals, while the sell-side has a more nuanced risk management first view, oriented around task, skills and, importantly, regulation,” Mr Wilcockson says.

Trends and predictions

Paul Garel-Jones, regtech lead partner at Deloitte UK, says one of the hottest areas at the moment is applying AI to convert unstructured data sets, such as video, image or voice, to consumable and actionable information.

“Financial service institutions are already using image and voice analysis to identify and authenticate their customers remotely,” he says. “They’re also increasingly using voice and image recognition-based AI techniques to profile behaviours and identify risks better.”

Some within the industry, such as Husayn Kassai, co-founder and chief executive of next-generation background check service Onfido, sees machine-learning as being hugely beneficial for financial services when it comes to banking the unbanked. Identity verification can prove tricky as these rely on people being registered with a credit reference agency.

London bankers are already hailing AI-driven regtech as a kind of magic silver bullet and saviour of the financial industry

Onfido already combines document checks with what it calls a “street-level check” where a postcard is sent to an applicant’s house to verify identity. But traditionally, only complex and expensive software has been able to scan and compute identity documents. “What’s cool about machine-learning,” Mr Kassai explains, “is that it will help us to be highly accurate in identifying documents which have been uploaded using commodity technology such as low-resolution smartphones.” If all you need to upload a document is a basic smartphone and an internet café connection, even people in developing countries can then be background checked.

Of course, it’s not all rose-smelling in the artificial intelligence garden; there are downsides to AI and machine-learning in regtech solutions. Torsten Mayer, vice president for regulatory solutions at data analytics company FICO, warns that the biggest danger in applying AI to regtech is that compliance, risk and fraud officers will get caught up in the hype around AI.

“There are a lot of vendors out there who are promising to solve everything with unproven AI solutions,” he says. “AI is not the sole answer to compliance and a great algorithm doesn’t by itself make a great solution.”

Indeed, AI can currently get you 80 per cent of the way there, but 80 per cent is not good enough in risk. A point picked up by MathWork’s Mr Wilcockson when he says that methods developed from Silicon Valley on largely static and fixed problems don’t automatically translate to the extreme dimensionality and unpredictability of Wall Street, City of London or Raffles Place.

But can it really fulfil these expectations?

AI in finance