Corporate bonds have, until now, largely flown under the radar of retail investors. With limited online trading and purchase sizes typically exceeding £100,000 a unit, they have historically been the preserve of large institutions and fund managers.

However, in an environment of low interest rates and unappealingly low returns on cash, there is a growing appetite among retail investors for an alternative to traditional savings products and often-volatile equity markets.

Yet, for many, the question remains: what exactly is a corporate bond? Simply put, corporate bonds are debt issued by companies looking to raise money to fund or expand the business. The company sells the bond to investors in exchange for a fixed rate of interest, known as the coupon rate, and the promise to repay the original investment at a fixed date in the future, known as maturity.

Bonds provide investors with greater certainty over when they will receive their money than equities

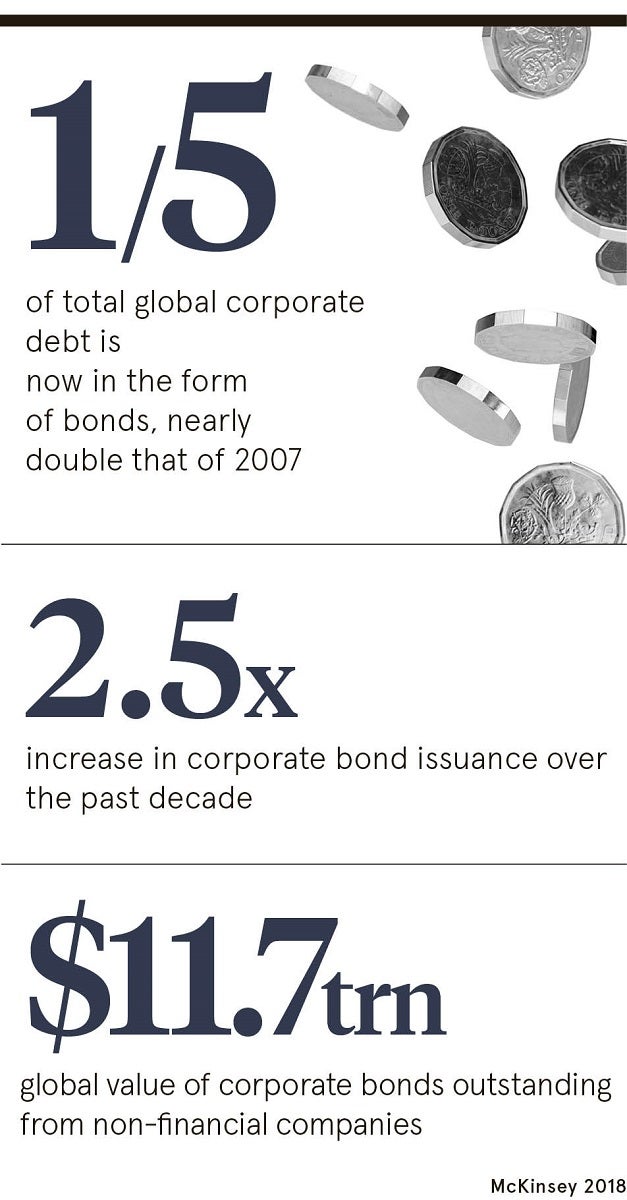

Raising capital through private investors has proved popular among companies that can otherwise face steep interest rates and various lending conditions attached to bank loans. According to the McKinsey Global Institute, almost 20 per cent of total global corporate debt is now in the form of bonds, nearly double that of 2007.

But, despite global growth and efforts in the UK to set up a dedicated retail bond market, most notably the London ORB (Order book for Retail Bonds), corporate bonds have retained an air of mystery among private investors, in part due to the traditionally institutional nature of the market.

Jeremy Spain, fixed income analyst at Charles Stanley, explains: “Either rightly or wrongly, some bonds tend to be looked at as being complex instruments and as such open to the possibility of a greater chance of mis-selling. This illusion has been given greater credence by the publicity surrounding the selling of certain types of fixed income instruments to private investors.”

Alix Stewart, fund manager at Schroders, echoes the sentiment that the dynamics of the bond market remain misunderstood. “There seems to be a misconception that without a default on an individual bond you can’t lose your principal; however, you can see the value of your fund fall if yields rise and the bond market sells off,” she says.

“This has meant that at times when there were big swings in bonds prices and defaults, or fear of defaults on many bonds, it was a shock to see the value of investments move so much.”

Liberalising the market

While private investors have been afforded exposure to company debt through the peer-to-peer market, this form of investing has often been plagued by negative headlines, limited liquidity and concerns over its durability.

In contrast, corporate bond issuances are assigned a rating based on their creditworthiness and offer an attractive investment opportunity that sits between cash and equities on the risk-return spectrum.

Rezaah Ahmad, founder and chief executive of digital bond platform WiseAlpha, says: “Corporate bonds are the best mainstream, risk-adjusted asset class; it is simply that they have been monopolised by institutional investors, leaving them closed off to the everyday investor.”

In a bid to liberalise the market, WiseAlpha has fractionalised the bonds of large companies into small units, allowing retail investors to invest in bond issuances from as little as £100.

Mr Ahmad explains: “Many of the companies issuing bonds are the same FTSE 350-listed household names that investors turn to for stock investments. Investors can benefit from transparent corporate reporting and the ability to easily track a company’s progress, while experiencing less volatility than equities.

“Bonds also have to be repaid by maturity, providing investors with greater certainty over when they will receive their money in comparison to equities, whose valuations are open-ended. From this perspective, bonds offer less risk and more reward.”

Mr Spain agrees that regular interest payments are an alluring prospect if the company is deemed creditworthy.

“The attraction of a fixed rate bond is that it offers a steady stream of income in the form of coupons,” he says. “Many investors are happy to take the income produced by a bond and ignore the day-to-day volatility in price, as long as the issuer demonstrates decent debt sustainability.”

Risks and opportunities

Broadly speaking, corporate bonds are divided into two risk categories: investment grade, considered low default risk and paying a lower yield; and high yield, otherwise known as junk bonds, deemed altogether riskier, but offering higher returns as way of compensation.

But there are a number of key considerations investors must make when assessing bonds, specifically the financial strength of the issuer, duration of the bond, interest rates and wider economic backdrop.

As Mr Spain explains: “There are plenty of considerations for any potential investor in the fixed-income markets; the most obvious are the prospects for global growth and the length of the current business cycle. These concerns are closely tied into the inflation outlook and any geopolitical risks.”

Corporate bonds often offer higher yields than other fixed-income instruments, including government bonds, to offset the higher risk involved. If a corporate issuer runs into financial difficulties, they may default on their interest payments.

In the worst-case scenario, the bondholder could lose all their original investment and, crucially, corporate bonds are not covered by the Financial Services Compensation Scheme. However, if a company defaults, bondholders are higher up the pecking order than shareholders when the proceeds of asset sales are shared.

There is also the cardinal rule of bonds: if interest rates go up, bond prices are likely to go down. But as the saying goes, “He who dares wins”. According to WiseAlpha, both investment-grade bonds and high-yield bonds have outperformed UK equities over the last 20 years both in terms of returns and price volatility.

Ms Stewart at Schroders says: “Investors in corporate bonds should look at them as a diversifier from the other parts of their portfolio; they would do well as an alternative to growth or value equities.

“Longer duration funds can provide a good offset to portfolios that would be exposed to a recession as central banks have proven they would cut interest rates further and buy corporate bonds again if the need arose. This would keep corporate bond valuations well supported.”

Against a backdrop of economic and political uncertainty, and a concerted push to provide investors with greater access and opportunities, corporate bonds could well become the investment of choice going forward.

Liberalising the market

Risks and opportunities