FUTURE INVESTOR

UK millennials have it rough. They battle a higher cost of living than previous generations and a well-documented struggle to scrape together deposits to buy a house. But this generation is also set for a windfall.

A report in June, entitled The Generation Game by financial group Sanlam UK, concludes that millennials are set to inherit some £1.2 trillion in the next 30 years, with around 5.1 million people anticipating windfalls of at least £50,000 in fixed assets.

With such a volume of cash changing hands, the profile of the typical investor will certainly change, so approaches to investing will need to adapt.

Large-scale intergenerational wealth transfer on the horizon

Jonathan Polin, chief executive of Sanlam UK, says the report demonstrates the scale of the intergenerational wealth transfer that the UK is set to see over the next few decades.

“This level of inheritance is unprecedented, and its transfer presents both opportunities and challenges for the financial services industry and society more generally,” he says. “That it comes at a time of societal, political and economic upheaval simply adds another element of complexity and uncertainty to an already extraordinary picture.”

The Sanlam report is the latest in a host of surveys documenting an imminent intergenerational wealth transfer, but senior investment executives are cautioning against treating millennials as one big homogenous group with identical investment behaviours.

“The future investor will, as now, have many faces,” says Simon Gibson, chief investment officer at advisory group Mattioli Woods. “Some will want to do it themselves, while others will value their time more and prefer someone else working for them.”

The many faces of future investors

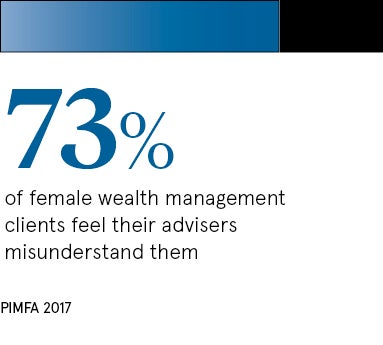

This new group of investors is also likely to have a much greater number of women, according to a report by consultancy group EY. This will require a marked change in how firms communicate with clients, according to Anne McClean, a financial planner at Charles Stanley.

“There is plenty of research to show that women aren’t engaging with investment. I have a lot of female clients of all ages and I can tell you that the issue isn’t one of interest but of language. As an industry, our language isn’t their language,” says Ms McClean.

This new group of investors is likely to have a much greater number of women

Financial commentators recognise the new generation will have very different attitudes to technology than the generations before them and that this will impact on their approach to portfolio construction.

Holly Mackay, the founder of consumer advice website Boring Money, says machines and artificial intelligence are likely to play a much greater role in investment planning in the coming years, and the new breed of investors are more likely to trust them.

“There is a US-based firm that launched last December which offers advice to clients for $10 a month. It’s game-changing,” she says. “For those with simple affairs, there is no reason why a machine cannot be programmed with tax and investment rules to help people with less complex needs, and learn to become more effective over time.”

Ms Mackay says advisers will still play a role in the investment planning process, but this is likely to be refined into developing and teaching these machines so they evolve and become more than just a static computer program.

She adds: “Those with complex needs, particularly around pensions, which remain hellishly complicated, will probably still need the individual touch, even in ten years’ time. The game of charging people 1 per cent to put together a portfolio of funds is over.”

FUTURE ADVISER

UK wealth management and investment advice groups need to work much harder to engage with the millennial generation.

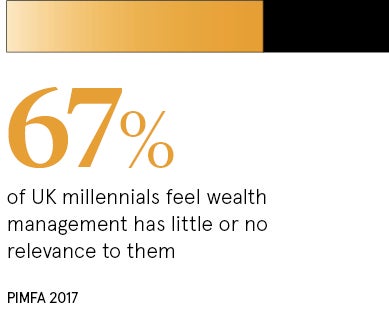

That was a conclusion from the Millennial Forum Surveys, published at the end of 2017 by the UK’s Personal Investment Management and Financial Advice Association (PIMFA).

The research, conducted with 802 millennials across the UK, found that 67 per cent of respondents felt wealth management had little or no relevance and nearly half of those in this category said they held negative perceptions of the industry.

Certified financial planner Colum Wilde, founder and chief executive of Clever Adviser Technology, says the younger generation’s view that wealth management had no relevance to them correlates with a general reluctance to save among younger age groups.

He explains that this was previously noted in a psychology paper, written by US behavioural economist Shlomo Benartzi, which found that young people view their older selves heading into retirement as strangers. Neurological research supports this.

An overwhelming message from the PIMFA survey is advisers of the future will need to do more to engage with the client in future decades, in terms of technology, customer relationship and portfolio composition.

Technology taking investment into the future

Jake Wombwell-Povey, chief executive at investment group Goji, says the next decade will see increasing numbers of advisers using technology to support the service that they offer.

“Technology will start to become bionic,” he says. “Advisers will supplement and support their client service offering with more technological applications.

Advisers will supplement and support their client service offering with more technological applications

“We will always value the human touch, so advisers need to use technology to drive efficiencies in commoditised services, like onboarding, reporting and compliance, while also supporting an increasing concierge-style offering in areas where customers really value advice.”

While Goji is a relative newcomer to the investment industry, Mr Wombwell-Povey’s sentiments are echoed by senior figures at far more established brands. Tracey Reddings, head of front office, UK and Ireland, at Julius Baer International, says: “The wealth management industry should be focusing on innovation not just disruption, harnessing technology to heighten the human touch, not remove it.

“Technology allows us to be more efficient and communicate globally with ease and speed, so rather than focusing on people versus technology, we should be concentrating on the benefits of enhanced interaction, heightened machine intelligence, processing speed and security to create a better customer experience.”

Is the future wealth manager a robot?

While much of the focus of industry commentators is focused on enhancing their existing role, there is evidence to show that many of the next generation of investors will want to avoid the human element altogether, opting for fully automated robo-advice.

A 2017 report by Loughborough University on the future of advice concludes that the preferred combination of technology–human capabilities is likely to evolve because tech will become more sophisticated. But it adds: “Some commentators believe that focusing on softer cognitive tasks will only protect human workers for a relatively short time.”

So are we heading to a completely automated advice sector? Not completely, according to the Loughborough report. The researchers say that while technology may be the first port of call for some fundamental functions, it is unlikely to take over completely because of its creative and social limits.

As Kuber’s chief executive Dermot Campbell concludes: “People still want face-to-face contact, but I see digital tools emerging to facilitate human advice, rather than just robo-advice.”

FUTURE INVESTOR

Large-scale intergenerational wealth transfer on the horizon