If you were to create a word cloud to describe capital markets in 2020, most prominent, in large, emphatic capital letters, would be VOLATILE.

At the start of the year, the most concerning aspect for those involved in capital markets was the UK’s exit from the European Union. There remains an uncomfortable amount of doubt about how Brexit will play out, with traders and business leaders alike looking longingly towards Brussels in the hope of a favourable outcome of negotiations before the transition period ends on January 1.

November’s American presidential election had long been circled as a time when the capital markets might play bull or bear. But then, in March, came the worldwide spread of coronavirus. The pandemic has touched every aspect of our lives and infected all sectors and their markets.

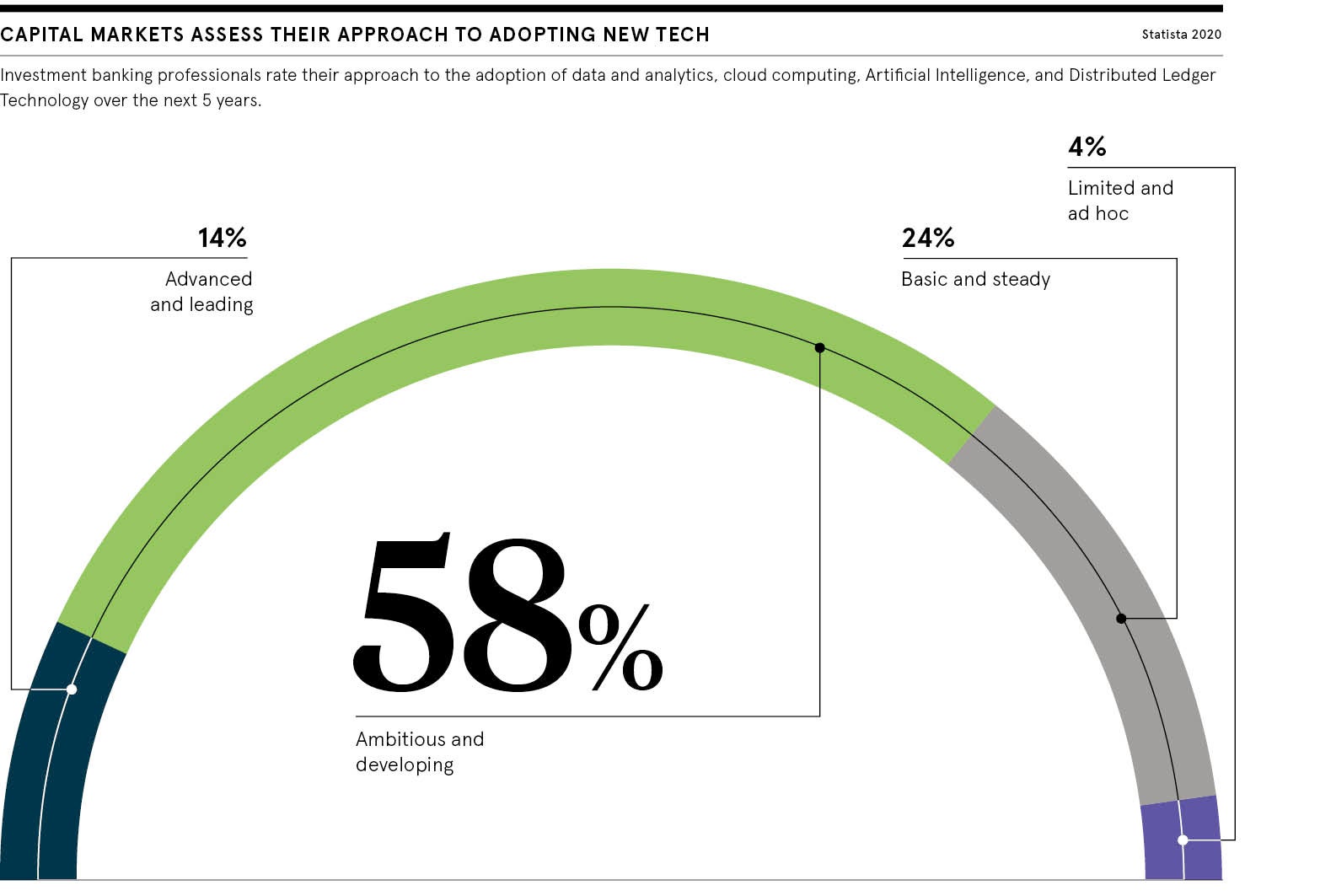

This extreme volatility has accelerated innovation to reduce risk, maximise returns and improve resilience for governments, large financial institutions and traders. And driving the necessary evolution of the architecture of capital markets is technology.

“Capital markets have had a tough year in 2020, mainly as a result of the coronavirus pandemic, with COVID-19 rates rising and the prospect of a third shutdown across the world now apparent,” says Sankar Krishnan, executive vice president of capital markets and banking at Capgemini. “Looming fiscal cliffs caused by shutdown, continued virus uncertainty and the US election impacting global politics are all added to the mix.”

Against this backdrop, though, several key trends have emerged and they might remain for some time. For one, there are new products and terminology. “We never before heard of terms such as ‘COVID stocks’, ‘work-from-home stocks’, ‘return-to-work stocks’ and few people had come across special purpose acquisition companies or SPACs,” says Krishnan.

Time to upgrade obsolete legacy systems

There has been substantial growth in SPACs, whose main objective is to raise capital through an initial public offering to acquire companies. In September, SPACInsider reported there had been $36.2 billion in SPAC proceeds so far in 2020, almost three times greater than the whole of last year at $13.6 billion.

However, private equity firms closed around 30 per cent of deals in the first half of 2020 compared to the same period last year, says Krishnan. “This is expected to continue for the rest of the year,” he says. “That said, mergers and acquisitions activity continued to be strong as valuations dropped.

“On the sell side, broker-dealers and investment banks have seen significant volume decline, mainly due to obsolete legacy systems that were driving down margins. Almost all large investment banks are investing in digital, mainly for improving customer and employee productivity, cybersecurity and rethinking talent.”

Predicting more development in this area, he adds: “It is widely anticipated traditional investment banking will get broken down to specialist investment banks that focus on deal origination and utilities that will perform middle and back-office functions.”

Another trend identified by Krishnan is the evolution of data providers, who play a “critical part of our capital market activity as we know it”. He says: “Traditional buyers rely on the likes of Slack and Bloomberg for trader communications and buyers are directly sourcing data from the market or boutique providers. A variety of capital markets-focused fintechs are also coming of age and establishing niche models in the field of Libor [London inter-bank offered rate] pricing, artificial intelligence-driven bond pricing, fixed income analytics and so on.”

Technology driving innovation and reducing risk

Michael Voisin, global head of capital markets practice at law firm Linklaters, says: “Capital markets are in a good state, both globally and regionally. They are doing what they are designed to do: providing cost-effective financing to businesses in need of it.

“The enduring benefit of the capital markets is their ability to provide deep liquidity for large fundraisings at the most competitive rates.” As an example, he points to the European Commission’s recent bond issues, which raised €17 billion and carried negative interest rates, so investors were willing to lose a small return on their investment in return for capital protection. “There was investor demand for €233 billion, so they could have sold almost 14 times more bonds at that price than they were seeking to raise,” says Voisin.

What is clear is we can’t stay as we are

This year he has spotted a jump in financing for environmental, social and governance (ESG) purposes, and is pleased governments are helping in this area. “Fundraising for the pandemic has included government-supported schemes, such as the Bank of England’s COVID Corporate Financing Facility, as well as longer-term financings,” he says. “And we have seen a raft of ESG issuance across the world, such as blue bonds in Asia to support ocean-related environmental programmes.”

Angie Walker, global head of capital markets and banking at software firm R3, believes blockchain technology and digital assets “will play a fundamental part in collateral optimisation, risk mitigation and driving much greater efficiency through vast simplification of otherwise over-engineered and unnecessarily complex processes”.

Suggesting that capital markets are “in a transformational state”, she sounds a note of caution. “It is evident that much has to change and the growing tide of regulatory obligations around risk, capital adequacy and reporting is going to continue to fuel that,” she says.

Blockchain and digital opportunities

When assessing the characteristics of global capital markets that demand unique technical architecture, Walker says: “Remote working combined with a significant shift towards capital formation within the private sector have driven a need for new architectures that allow for the facilitation and global accessibility of asset types not accessible through traditional central market infrastructures.”

And it is here where blockchain, the immutable ledger underpinning bitcoin and hundreds of other cryptoassets, can play a pivotal role. “The digitalisation of such assets and representation of those assets on distributed ledger-based technology is vital to allowing this to grow exponentially, in a way that centralised infrastructures, such as regional stock exchanges, would not have addressed,” she says.

Offing a final piece of advice to those operating in capital markets, Walker adds: “What is clear is we can’t stay as we are. Yet for the braver, nimbler and more pioneering industry providers, the opportunity to leverage digital innovation to drive true greenfield growth is immeasurably large.”

In such uncertain and volatile times, these words envisioning a brighter, tech-powered future serve as a welcome balm.

If you were to create a word cloud to describe capital markets in 2020, most prominent, in large, emphatic capital letters, would be VOLATILE.

At the start of the year, the most concerning aspect for those involved in capital markets was the UK’s exit from the European Union. There remains an uncomfortable amount of doubt about how Brexit will play out, with traders and business leaders alike looking longingly towards Brussels in the hope of a favourable outcome of negotiations before the transition period ends on January 1.