There is no doubt 2020 has been tough for every industry, but with the economic fallout of the coronavirus pandemic still very much ongoing, how will that impact the future of fintech as we head into 2021?

Fintech has long been lauded for being at the heart of change within finance, driving future thinking through agile launches and thrive-or-fail advancements. It ended 2019 with high hopes, but progress and opportunities in many areas, such as travel, have been stifled, with funding down or flat.

That is not to say some parts of the sector haven’t succeeded. For instance, those in the buy now, pay later credit space saw huge funding rounds; Klarna raised $650 million and Affirm received $500 million, fuelled by demand from stuck-at-home consumers, looking to finance DIY projects, plus new furnishings and household products.

But will this general belt-tightening continue in 2021 and who will suffer the most? Well, according to a report by FleishmanHillard Fishburn, which has been developed in conjunction with Money20/20, seven in ten of the C-suite fintech leaders spoken to think early-stage fintech startups will find it more difficult to secure funding going forward. Two-thirds also believe there will be a spike in mergers and acquisitions, due to many fintechs being cash crunched.

Opening the report, Claudia Bate, fintech lead at FHF, says: “Funding has dried up as investors grow cautious, expansion plans have been shelved, and hyper-growth and unprofitable businesses are feeling the strain.”

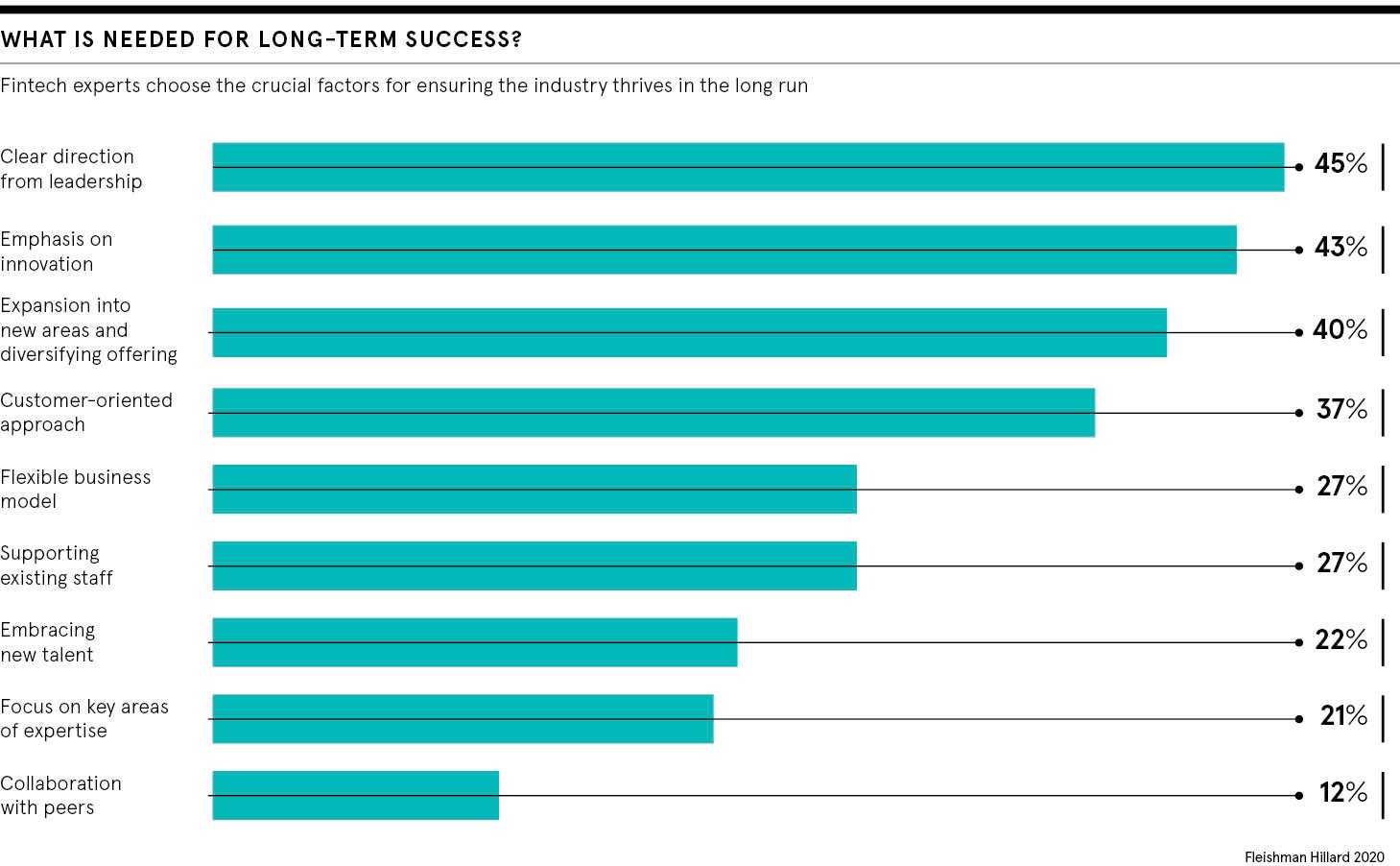

Concerns around profitability also cause Alex Reddish, chief commercial officer at Tribe Payments, to believe investment will be constrained as goals change. He predicts: “The bull run had to end sometime. As COVID-19 rolls on and the recession deepens, investors will no longer be satisfied with ‘growth’ and instead will be looking at hard numbers: profitability, average revenue per user, discounted cash flow, price-to-earnings ratio.

Funding has dried up as investors grow cautious, expansion plans have been shelved, and hyper-growth and unprofitable businesses are feeling the strain

“We will see a shift away from paid customer acquisition, ‘moon shot’ ideas and unfocused diversification, where fintechs rebundle a multitude of services, towards specialised and sustainable offerings that can prove profitability.”

Open Banking will drive traditional banks forward

One beneficiary of this proposed laser focus could be in now proven and accepted solutions, such as digital payments, through open banking. These have seen a huge boost in 2020 because of COVID, both in their use but also, crucially, in the confidence people now place in them.

And with the cost to the merchant of taking payment, for example through their own app, being lower than through the traditional contactless chip-and-pin card routes, Nick Corrigan, UK and Ireland managing director and president of Global Payments, says the pace is quickening for smaller, everyday payments using such means.

He explains: “While these entrenched payment rails have a very important place, offering protection for bigger purchases like a TV or a holiday, they aren’t needed for many consumer purchases. It’s unlikely you’re going to seek a refund and have to have a chargeback raised for a cup of coffee or an insurance renewal, which is what these big networks are so vital for facilitating.

“When you take these types of credit and debit-card purchases, about 30 per cent of them could sit outside of the typical network ecosystem. This is why we’re seeing banks quickly launch their open banking services, specifically for these types of scenarios. In 2021, open banking is really going to start doing what it was intended to do: increase competition.”

Another, perhaps unexpected, use for open banking in the future of fintech could be for social good, especially given the number of financially vulnerable people looks set to rise due to unemployment and recession. Not-for-profit lender Fair for You’s Sarah Gardiner says: “We use open banking to enable low-income families who meet our affordability checks, but who can’t access mainstream credit, to buy essential household items with ethical credit. As you’d expect, we’ve seen a substantial increase in applications for affordable loans during the pandemic.

“We will keep serving more customers with dignity in 2021, with our only limiting factor being levels of additional investment. We’re thankful to the UK’s leading social investors for investing millions into us this year and are now seeking an additional £10 million in debt funding to continue to help vulnerable families navigate the challenges of Brexit and the pandemic.”

Global business and fintech can thrive together

In the year ahead we will also see technology brands ramp up their own future of fintech plays, for example Amazon Pay will be joined by Google offering its bank account as well as the rise of the Apple Card. All could offer opportunities for smaller fintech players to capture the attention of these big, money-laden beasts with their own innovations.

Having such huge consumer names raising fintech’s profile will also help to grow use of the ewallet, something many experts predict will be the big future of fintech talking point for 2021 among retailers and customers.

Jane Loginova, co-founder of Radar Payments, believes this will be emboldened by retailers embracing new payment methods and it could also be boosted by one of 2021’s surprise successes, the QR (quick response) code, which gained prominence due to the influence of COVID tracking-and-tracing apps.

She says: “Unlike card transactions which require merchants to invest in costly and complex point-of-sale terminals, QR codes are cheap to deploy and easy to use. Currently, the QR code payment solutions available require an app, for example developed by a retailer, that can only be used in its stores. In developed markets, leveraging popular digital wallets already on consumer smartphones, such as Apple Pay, Samsung Pay and Google Pay, will make QR codes more accessible. They will continue to emerge as an important payment method in 2021.”

Brad Hyett, chief executive of phos, agrees on the importance of ewallets to the future of fintech, saying they prove contactless is here to stay. “The launch and proliferation of ewallets has been building in 2020, but this trend will really take precedence in the world of payments in 2021,” he says. “The global mobile wallets industry is predicted to jump by almost 50 per cent, to reach a value of $1.47 trillion amid the COVID-19 pandemic, with more than 1.7 billion people using mobile wallets by 2024.

“While most of us will be familiar with Apple Pay and Google Pay, these won’t be the only touchpoints that people have with ewallets either. Increasing numbers of companies are developing their own solutions to directly serve the needs of their customers.

“The majority of smartphones in use today can natively offer this kind of technology, so customers can pay on a website, a mobile app or physically in-store. But the crucial point is all these scenarios are contactless and cashless, and so respond to the changing demands we have seen for these kinds of payment options.”

There is no doubt 2020 has been tough for every industry, but with the economic fallout of the coronavirus pandemic still very much ongoing, how will that impact the future of fintech as we head into 2021?

Fintech has long been lauded for being at the heart of change within finance, driving future thinking through agile launches and thrive-or-fail advancements. It ended 2019 with high hopes, but progress and opportunities in many areas, such as travel, have been stifled, with funding down or flat.

That is not to say some parts of the sector haven't succeeded. For instance, those in the buy now, pay later credit space saw huge funding rounds; Klarna raised $650 million and Affirm received $500 million, fuelled by demand from stuck-at-home consumers, looking to finance DIY projects, plus new furnishings and household products.