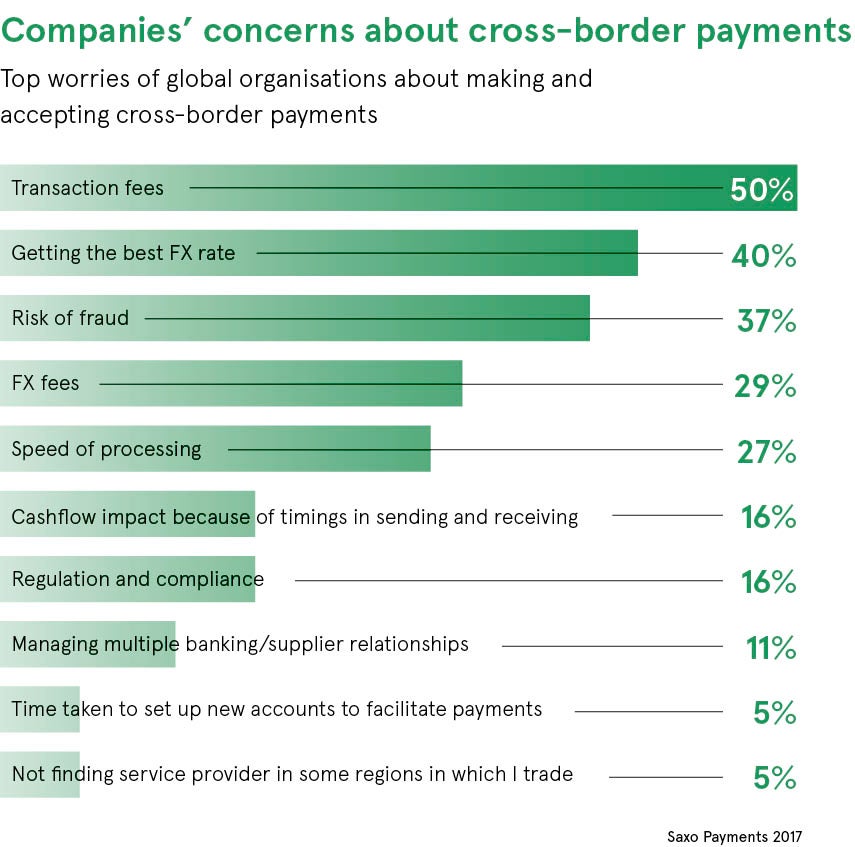

Anyone who has transferred money between countries recently realises the process has evolved little in decades. Too slow, too opaque and too expensive are the gripes. This is sparking debate among banks worldwide whether cross-border payments could be faster and cheaper, more reliable and transparent, if a 21st-century digital solution was deployed.

The prize is hardly small change, global payments looks set to be a $2-trillion industry by 2020, according to McKinsey, accounting for a third of banking revenues. And as more of us become plugged into the globalised economy, the money changing hands is set to head skywards.

Blockchain, the distributed ledger technology (DLT) that underpins cryptocurrencies, is touted as one solution. Roughly 90 per cent of top European, North American and Australian banks are experimenting with it, and recently it has reached peak hype.

The unique selling point of blockchain – that mutually distrusting parties, geographically agnostic, can reach a trusted agreement electronically without a referee – is music to bankers’ ears. Some say it’s still an immature technology looking for a problem; others say it will transform how we make payments worldwide. At the same time the incumbent in the global money-moving industry, Swift, is fighting back. So the jury is still out.

FOR

DLT is more efficient, accurate and trustworthy, but it needs the right systems in place

Even though blockchain is potentially entering Gartner’s “trough of disappointment” in its so-called “hype cycle”, it still offers answers to the current painpoints in international payments. It’s all about getting rid of the middleman. When two business parties involved have a single-shared view of the transaction, there’s a paradigm shift.

“After a century in which the costs of financial intermediation have remained largely unchanged, DLT could now be a game-changer for the industry,” explains Kuangyi Wei, head of research and market engagement at management consultancy Parker Fitzgerald. “When it comes, the estimated savings could be up to a third of current operating costs.”

The requirement of banks to hold and process funds temporarily for transactions that they might otherwise have no vested interest in could diminish with blockchain.

Currently, payment providers need to pre-fund accounts on either side of a transaction in local currencies. This can be expensive and lead to a poor deal for customers. DLT negates this need. That’s because trust is hardwired into the design of blockchain. Everyone has a record. The ledger doesn’t lie. Shared record-keeping also boosts efficiency and reduces data discrepancies.

“All parties within the payment system have to reconcile the data at every stage. DLT could provide a highly available, cryptographically secure and trusted platform where all parties have access to the same data,” says Otto Benz, payments technical services director at Lloyds Banking Group.

Small to medium-sized enterprises, in particular, suffer from payments difficulties. “They are currently left in the dark about the status of their transaction and out of pocket from high fees,” says Marcus Treacher, global head of strategic accounts at Ripple. “It can also take weeks for a cross-border payment to settle, which can put the brakes on a small business’s liquidity, and create friction between customers and suppliers.”

After a century in which the costs of financial intermediation have remained largely unchanged, DLT could now be a game-changer for the industry

Those that do millions of international micro-payments, from hotel booking engines to auction sites, also have an issue.

Ripple, a California-based company, among others, is leading the charge for blockchain in this industry. It’s already working with more than 100 financial institutions worldwide, including the Bank of England, to leverage the technology.

But Ripple, backed by Santander, says its distributed ledger is not currently scalable or private enough for banks. “Putting all the world’s transactions on one blockchain is impossible. Institutions also have diverse needs when it comes to payments and one single blockchain is not capable of serving all of these, let alone in the public domain,” says Mr Treacher.

It’s the reason why Ripple and others are developing inter-ledger protocols that can be adapted by all. Banks in different countries often run computer systems that cannot talk to one another. When the international financial plumbing is standardised then this technology could come into its own and in the process strengthen the global financial system.

“This should increasingly provide one route for improving consumer confidence in banking, in that the requirement of banks to process funds for transactions that they might otherwise have no vested interest in will diminish, and so banks can be judged solely on the services they provide and the performance of the products they sell,” says Kit Ruparel, chief technology officer at Recordsure.

AGAINST

AGAINST

DLT is over-hyped and will be difficult to scale

Clunky and cumbersome are two words that have been used to describe distributed ledgers. When immutable databases are maintained by a network of computers, rather than a centralised authority, and secured by advanced cryptography, you can just imagine the computing power you need to reconcile everything. The problem gets worse when the number of cross-border payments, banks and jurisdictions increases.

Centralised databases are still more efficient than blockchains. Over-sold and over-hyped are other words used in this context, managing expectations on what blockchain can achieve will be critical.

“The crucial problem of maintaining the order of all transactions across all copies of the data is a fundamental computer science problem. For DLT to make it into production, the majority of institutions have to agree to use the same procedures,” says Lloyds’ Mr Benz.

There are several forums now established to develop and promote standards for industrywide DLT adoption. One example is Utility Settlement Coin, an asset-backed digital cash instrument using the technology within global institutional financial markets. But these are still early days.

Financial services firms are concerned about the idea of sharing a network that allows their competitors to see even anonymised records of their transactions

It is the reason why Swift, the 45-year-old, Brussels-based incumbent and global heavyweight in worldwide payments, is still going strong. The co-operative is owned by thousands of banks. The organisation still deals with half the world’s high-value transactions that move across borders.

Swift hasn’t sat still either; with all the blockchain hype, it’s been busy trying to address the painpoints in payments with speedy transfers, transparency, predictability of fees, end-to-end tracking and transfer of rich data. That’s why Swift has developed their Global Payments Innovation (GPI), a new set of business rules that 165 banks worldwide have signed up to. Half of all payments now reach their destination within 30 minutes.

“Rather than combating DLT, a lot of incumbent systems are embracing the opportunities that it presents. The GPI solution is a much-needed upgrade to a broken system. While this is not transformational, it signifies a step in the right direction,” says Mr Treacher.

Swift has tested blockchain and is sceptical about whether it could achieve the scale needed for a global payment ecosystem. The examples banks currently use of blockchain are those involving simple in-house transactions or those between just two institutions.

“Operational resilience has also become a major issue for central banks and regulators. Concerns raised about DLT include privacy, security, scalability and competition,” explains Ms Wei at Parker Fitzgerald.

“Take privacy; even if the keys or certificates to each transaction are anonymised, in a small network of users it can be easy to identify participants by analysing transaction flow. Financial services firms are concerned about the idea of sharing a network that allows their competitors to see even anonymised records of their transactions.” So, do watch this space.

FOR

DLT is more efficient, accurate and trustworthy, but it needs the right systems in place