We’ve heard it all before: incumbent banks need to transform their legacy systems, whether to meet the shifting regulatory landscape or purely just to remain competitive.

But while many fintech firms have developed the software and solutions to help, they have felt pushed aside until relatively recently, begging the question whether they are trusted by the legacy players.

Fahd Rachidy, founder and chief executive of digital retirement solutions fintech ABAKA, says both fintechs and traditional banking groups need to work harder on collaboration if the pace of innovation is to continue to increase.

Traditional firms are very risk averse and for heavily regulated, companies are reluctant to take a chance on new technologies

Mr Rachidy says fintechs are guilty of developing impressive innovations, but without giving due consideration to the systems with which they need to dovetail.

“Their products have not been capable of integrating seamlessly with complex legacy technologies or adapting to the varied business requirements of companies in this sector,” he says.

“Core applications have also not been strategically aligned with banks’ future marketing and business initiatives. Fintechs might have bright ideas, but ultimately they lack focus on delivering practical products and processes that can be manufactured affordably and integrated with ease.”

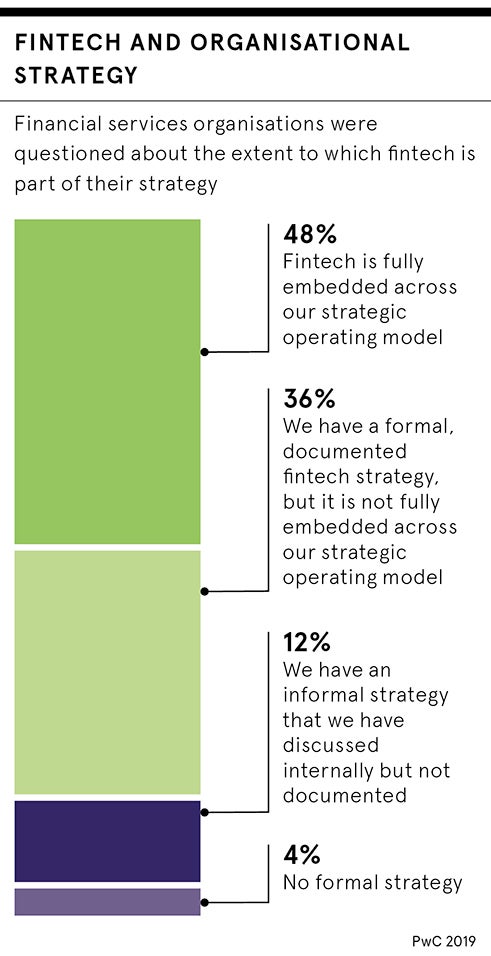

Many ways to transform core banking system

Kanika Hope, global strategic business development director at Temenos, acknowledges it has been hard for a bank to come across a fintech that fits exactly with its business model or exacting compliance standards. But she says this is simply a stumbling block and the focus is now on acquiring or incorporating the capability fintechs bring.

“One model by which banks are embracing fintechs is to buy the technology from the fintechs via digital marketplaces or pay-as-you-go open application programming interface-based technology platform models which are on the rise, especially in Europe,” says Ms Hope.

“Another model is the building of fintech capability from scratch in-house, ring-fenced from the mothership, but wholly owned by the bank.”

Ms Hope cites Bank Leumi of Israel as an interesting example of an incumbent bank with legacy technology that has chosen to build a brand-new digital-only bank to try and get around some of the issues.

“This build-and-renovate approach is a more transformative approach than the comparatively light-touch partnerships between fintechs as it opens up the option of migrating the parent bank’s existing business in the future,” she says.

Is big really best when it comes to tech?

In spite of the products and services on offer from fintech firms, banks have so far favoured the business models of major companies. For Mitesh Soni, chief evangelist at global fintech firm Finastra, this boils down to risk appetite and culture.

“Traditional firms are very risk averse and for heavily regulated industries like banking, companies are reluctant to take a chance on new technologies. As the adage goes, nobody ever got fired for choosing IBM,” says Mr Soni.

Companies such as IBM employ a large team of highly skilled people, giving off the impression to its customer base that should something go wrong or need attention, they have the manpower and expertise to solve it swiftly.

Gareth Malna, associate solicitor in the fintech team at Burges Salmon, explains: “The bank either wants full control or to know that it is dealing with a reputable provider. Even fintechs that have great products can be bad businesses and unknown fintechs provide both reputation and business-continuity risks.

“This partly explains why banks choose to take over fintech businesses; it gives the bank that level of control over the whole of the business which wouldn’t otherwise exist.”

But Remonda Kirketerp-Møller, founder and chief executive of regulatory technology firm muinmos, argues it is a misconception that the larger technology providers offer more protection to financial institutions.

“That’s simply not the case,” she says. “These large technology providers have very strict limitation of liability clauses to secure themselves against IT failures and similar, and in return, limiting any compensation they will pay out to those financial institutions relying on them.

Ms Kirketerp-Møller says fellow regtech innovators have identified huge opportunities to work with financial services firms, clients and regulators, and have found ways to navigate the corporate risk of mis-selling through strict governance and great service.

Time for change and collaboration

While it is clear the large, well-established businesses have a strong foothold among financial institutions when it comes to the transformation of their core banking solutions, fintechs that can prove their worth and longevity can break the mould.

“This is simply a product of time and credentials,” says Mr Malna. “The time it takes to build those credentials is often in stark contrast to the speed at which the fintech is working internally and that mismatch can create frustration.”

The relationship also works both ways and as financial institutions begin to open their doors, albeit slowly, to the idea of innovative technology offered by fintechs, so too must the fintech firms embrace the core of the banking sector, most notably compliance.

“Fintechs need to embrace compliance with relish,” argues Flux co-founder and chief operating officer Veronique Merriam Barbosa. “It shows that you’re capable of doing what you say and can be trusted. It’s independent, immoveable and can be the keys that allow fintechs into the core banking system to improve it for the better.

“Compliance shows clearly your ability to not only make something interesting, but something which genuinely works with an existing industry, demonstrating validity to a specific audience, and that it could be used at scale to improve financial services for everyone.”

Many ways to transform core banking system