Conventional wisdom in the financial world is that large incumbent banks need to partner with smaller startup and scale-up companies for a mutually beneficial relationship that aims to foster innovation and ultimately improve services.

Recent regulatory mandates, based on the European Union’s second iteration of the Payments Services Directive as well as from the Competitions and Markets Authority (CMA) in the UK, have pushed traditional banks to open up their data and platforms, in the form of application programing interface (API) toolkits.

These APIs, mostly focused on retail current accounts, create an avenue for financial services startups to integrate their products with existing bank infrastructure more easily. The aim is to create a more competitive environment and hopefully offer increased options for consumers. All of this is known by the umbrella term “open banking”.

Click to view

The CMA directive is aimed at the top nine banks in Britain and Northern Ireland, banks such as Barclays, RBS and Lloyds Banking Group. Despite not being governed by the CMA mandate, Starling Bank, a year-old mobile-only bank in the UK is taking an aggressive approach to open banking.

According to Megan Caywood, Starling’s chief platform officer: “Starling is taking that a step further with its API and marketplace. The API goes beyond the CMA requirements and looks to surface every Starling feature via the API, such as an API for savings goals even though that isn’t mandated, and enabling accessibility tools like webhooks to make integration easier.

“The Starling marketplace goes beyond simply enabling third parties to access bank data; it enables those parties to be visible and available to customers within the Starling Bank app – it integrates the partners’ APIs as well. That’s appealing to third parties as it gives them a new customer-acquisition channel and a way to make it easier for Starling customers to access their products.”

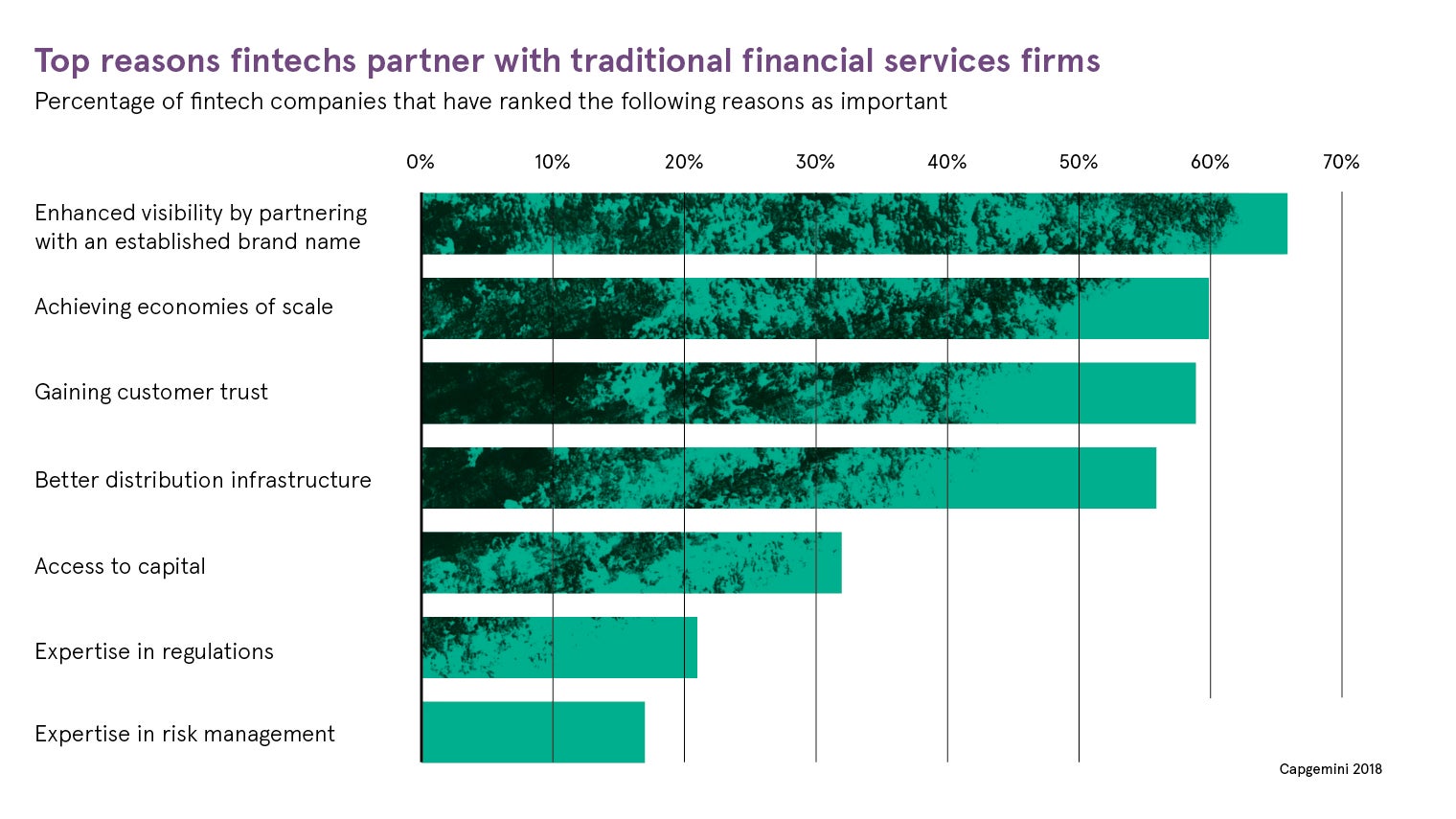

Last month, global professional services firm Capgemini launched its World FinTech Report, along with LinkedIn and in collaboration with Efma. The overarching theme was that global fintech – financial technology startups – and traditional financial institutions and banks need to partner and collaborate. While that goal sounds good on conference panels and in blog posts, the reality is much harder to actualise.

Nektarios Liolios, founder and chief executive of Startupbootcamp FinTech, an accelerator programme for global fintech startups funded by partner banks and financial services firms, sheds some light on the lofty goal of startup-bank partnerships.

Speaking as part of a transatlantic debate, hosted by Capgemini, in association with 11.FS Media, Mr Liolios says the problem lies in the chasm between an appetite for innovation and a capacity to achieve it on the part of traditional financial services firms. Conversations on how to bridge that chasm are not happening, he says.

“How do you measure success, how do you measure what works and what doesn’t work? How do you get the business excited enough to put money towards it when the innovation budget is actually shrinking?” Mr Liolios asks.

Startups are not standing out from the crowd

According to Carrie Osman, founder and chief executive at CRUXY & CO, a strategic UK consultancy, many banks are now overwhelmed by the possibilities opened up by the regulations fuelling open banking. “You would think, with these regulations coming out, it would make it easier for banks. What is happening is it has made the space more crowded,” she says. “Startups are not standing out from the crowd.”

However, startups need to focus on exactly what value they will bring to a large firm and how their offering will interact with vast, enterprise-wide technology “from day one”, Ms Osman adds.

Despite the hype and noise around bank-fintech collaboration, and past struggles to make these partnerships happen, there are bright spots appearing within the financial services sector. Late last year, HSBC and their subsidiary First Direct announced a partnership with London-based fintech startup Bud. Most recently, Barclays signed a banking deal with cryptocurrency exchange Coinbase and, as part of the deal, Coinbase now has an e-money licence and access to the Faster Payments Scheme.

Case Study 01

Starling and PensionBee

Starling Bank recently added PensionBee, a UK-based startup, on to its marketplace. Starling uses the PensionBee application programming interface, or API, to pull a pension balance into their app, when customers give permission to share that data. Existing PensionBee customers can see their real-time pension balance alongside their real-time current account balance. According to Clare Reilly, head of corporate development at PensionBee: “A pension is not an abstract pot of money, shrouded in complexity, which bears no relation to the rest of your financial universe. Your pension balance should be visible alongside all your other balances, current account, ISA, mortgage, credit card and savings.”

Case Study 02

Munich Re and Buzzvault

Munich Re’s Digital Partners business recently partnered with Buzzvault, a UK startup offering a home contents insurance product. The solution is a digital asset vault built on blockchain technology. “In theory, Munich Re could have built their own blockchain-based home contents insurance product,” says Andy Rear, managing director of Munich Re’s Digital Partners, “but the result would not be as good.” Working with Buzzvault “enables us to bring our insurance and data expertise to the market in a different way”. According to Becky Downing, chief executive of Buzzvault: “Collaboration has always been at the heart of successful innovation – think of Apple working with the likes of Verizon and Intel.”

Case Study 01