This Christmas you could acquire a car laden with artificial intelligence (AI). It may only be a few inches long – AI startup Anki does not make them full size – but it’s the direction of travel for the consumer market.

“We shouldn’t underestimate how common AI systems already are in our lives,” says Sarbjit Nahal, head of thematic investing at Bank of America Merrill Lynch Global Research.

Boris Sofman, one of the co-founders and chief executive of Anki, adds: “I believe we are now at the inflection point of realising AI’s true potential, which will greatly impact many of the biggest and most entrenched industries, just as we’re seeing with entertainment and transportation industries today.”

As the use of this technology grows, so potentially does the commercial success of its developers. However, investors need to understand exactly what they are getting when they buy into stocks of firms that offer AI technology. The starting point is to understand what we mean by artificial intelligence.

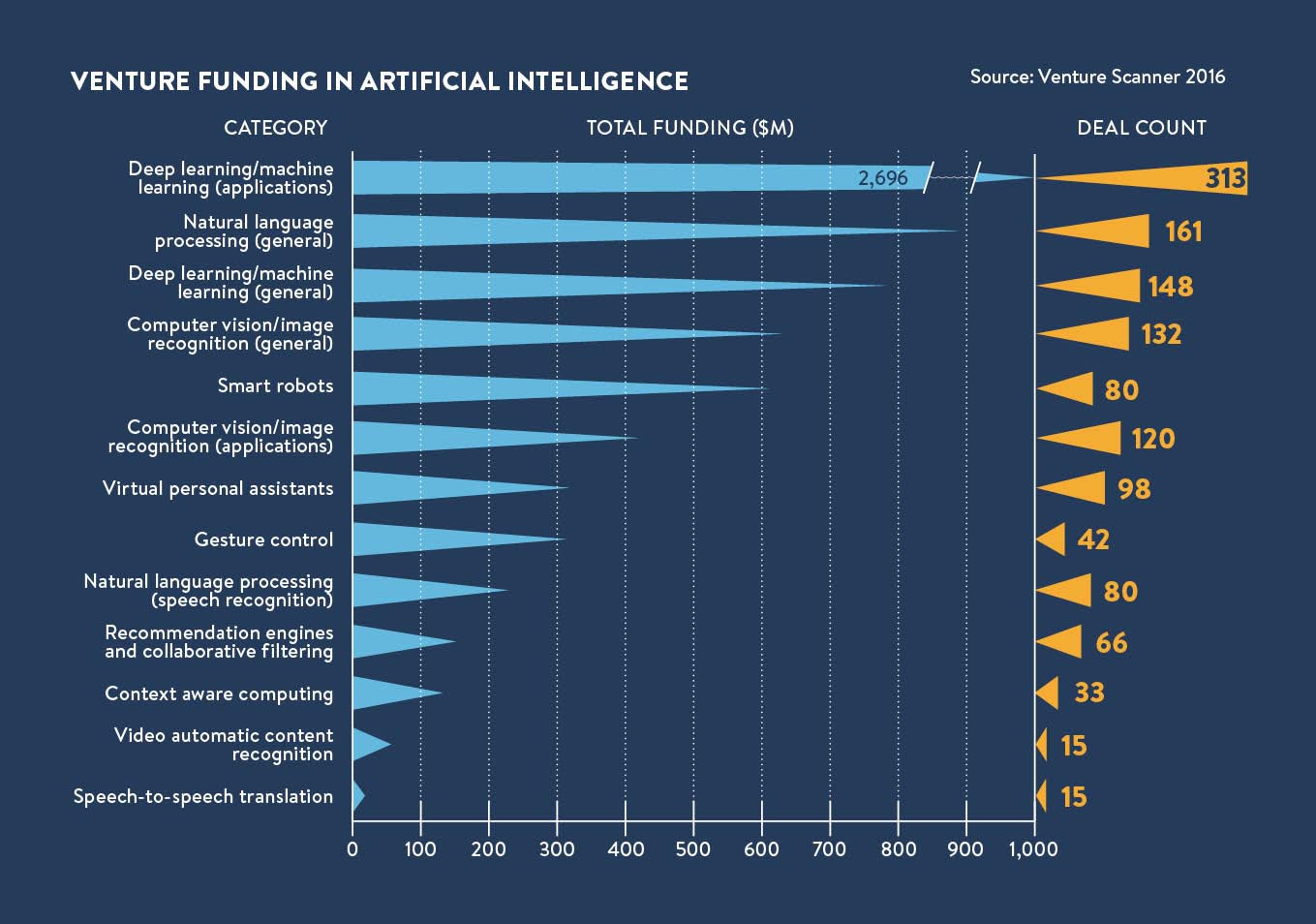

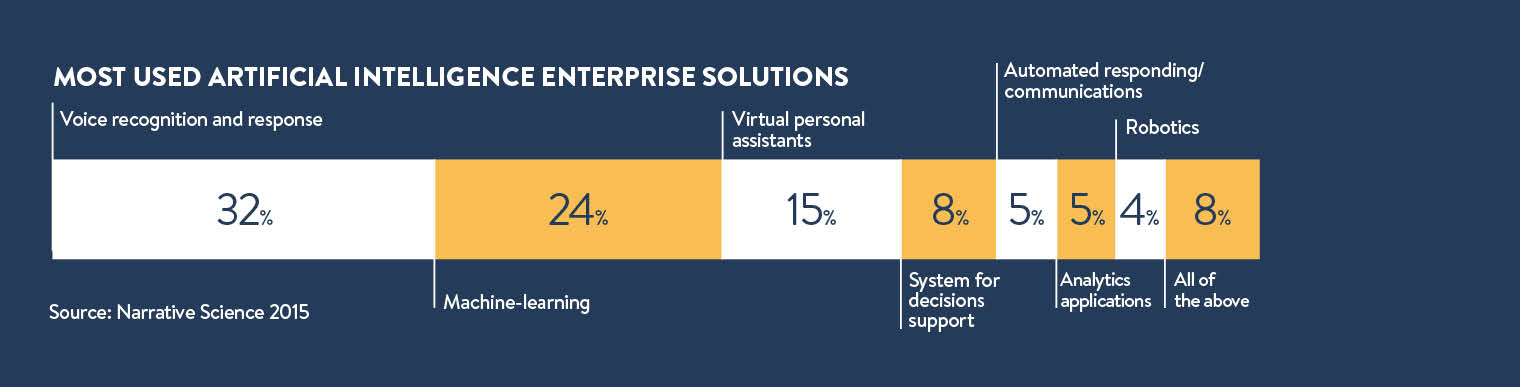

Click here for the full infographic

Artificial intelligence explained

Back in 1980, John Searle, Slusser professor of philosophy at the University of California, Berkeley, split AI into two categories: strong AI, meaning a truly conscious mind; and weak AI, which replicates the action of the mind without understanding.

Professor Searle argued that digital technology could only develop weak AI. He said the former was impossible for digital computers to develop and that the commercial AI technology on offer today falls into the weak-AI category. Despite the moniker, this is powerful technology.

“The difference is akin to the way a child learns multiplication by rote, allowing them to give the right answer to a multiplication question without, at first, understanding why,” says Professor Mark Bishop, director of the Tungsten Centre for Intelligent Data Analytics at Goldsmiths College, University of London. “Most people perceive that over time the majority of tasks humans do are vulnerable to being mechanised [using weak AI].

Firms are now able to put AI in a working environment with confidence so investors can get a clearer view of a business’s offering and assess its potential

Voice recognition, visual recognition and the reading of emotion all require weak AI to function. From a practical point of view these tools are specialist rather than being a general intelligence which can be adapted to different tasks. For the investor, this impacts where a firm has commercial opportunity. A self-driving car will not suddenly become sentient and begin to solve complex medical questions; the developers must have a particular market in which the technology can be applied.

The use cases of systems themselves fall into specific niches, which are incredibly varied. Hardware manufacturers that provide graphical processor units and other pieces that are necessary to deliver AI systems are one possible investment case.

A research report published by Bank of America Merrill Lynch Global Research last November noted eight key businesses that could serve as entry points for investors wanting exposure to AI stocks. These included the technology providers themselves, aerospace and defence, notably drones, automotive and transport stocks, financials, healthcare, industrials, domestic services, agriculture and mining.

The breadth of investment cases is, therefore, considerable. A dynamic that investors need to consider is the maturity of these systems. Firms are now able to put AI in a working environment with confidence so investors can get a clearer view of a business’s offering and assess its potential as a stock to invest in.

A confluence of factors have led to a sudden rise in the growth of AI technologies, which allow for greater innovation and experimentation, says Professor Andrew Moore, dean of the School of Computer Science at Carnegie Mellon University in Pittsburgh, Pennsylvania.

“To help restaurants understand whether their customers are enjoying themselves, you can put in a system that measures smiles and face creases,” he says. “Four years ago that was science fiction, now you can put that together pretty much using open source software.”

An example visible to the public has been the rise of AI personal assistants. Apple’s Siri, Amazon’s Echo and Microsoft’s Cortana are all downloadable or built in to devices and make smart interpretations of what the user is saying.

“We are entering a world where some companies have a pretty good road map for the next five to ten years so there is an investment opportunity, but there will also be a profound period of disruption; some companies are just waking up to the fact that customer interaction will be very different by 2019,” says Professor Moore.

Digital firms leading the way

The large digital firms and established technology providers are leading the charge in developing technology. In a February 2015 report, entitled The real consequences of artificial intelligence, Goldman Sachs found that the greatest number of AI-related patents filed with the United States Patent and Trademark Office were by IBM, followed by Microsoft, then private individuals and Google.

“When you look at everything behind the investments made and the patents filed, those numbers have increased and there is a relatively small number of companies coming to dominate the space, including traditional American technology firms as well as several Japanese IT companies,” says Mr Nahal.

Firms that operate in the online environment are able to expose their tools to a greater number of users and thereby help their systems to learn allowing some firms to extend their position as leaders.

“The more users that are involved, the smarter a machine can get,” Mr Nahal says. “The smarter it gets the more users you will have. So there is a compounding or network effect which does very well for the tech companies that are involved in this space.”

He gives the example of service robots where growth has been far quicker than the market had anticipated. “It has already gone beyond the levels expected of 2020,” he says.

The issue of control over AI will mean device manufacturers that can aggregate control over multiple AIs with a single interface will get an advantage and potentially disintermediate other firms offering AI.

“The way that shakes out will determine who the winners and losers are during this period in the market,” says Professor Moore.

There are also unusual dynamics in the technology business, such as open source technology, which can change the capacity of new firms to rise up and develop new systems, in some cases undermining existing value and in other cases creating it.

Anki’s development of AI-enabled toy racing cars and robot companion Cozmo will not come purely from internal developments, says Mr Sofman, and will also contribute to wider sector growth.

“We certainly don’t think this is something that we can or should do alone, which is one of the reasons we are planning to release the Cozmo [platform development information] in the near future, to empower academics, researchers, developers and aspiring roboticists to use this incredibly capable platform for both research and entertainment applications,” he says.

The adoption of open source and information-sharing in the AI sphere may well mean the growth of the sector can be far greater than is predicted even now.

Artificial intelligence explained