A succession of reforms has redrawn the pensions landscape, for the first time urging those saving for retirement to really focus on their finances and make some crucial decisions about the future. But they also need the tools and the educational support to help them do that, which is where companies such as Aon have moved swiftly to provide them.

Aon’s flagship products, Bigblue Touch and the Aon Master Trust, are set to play a key role in the workplace financial education space.

Wrapped around the schemes is a technology platform through which members can access a suite of financial aggregation tools that allows them to track their personal finances in parallel with their retirement savings. This puts them in a better position to understand if they are on track for the retirement outcome they need and, if not, what options they have to improve it.

This nudging technology effectively shows you how to create more disposable income – you cannot engage with a pension scheme unless you can see your complete financial situation

It is what Tobin Murphy-Coles, Aon commercial director, describes as “nudging technology”.

He says: “Traditionally, if you wanted to save into a pension scheme, you would go to a provider, join a scheme, get access to the provider’s website and see how your pension is performing.

“With Bigblue Touch and the Aon Master Trust you can get a detailed overview of your financial affairs, including your mortgage, savings, plus any additional pensions or investments, enabling you to reach a decision on whether you can afford to pay more into a pension scheme.

“This nudging technology effectively shows you how to create more disposable income – you cannot engage with a pension scheme unless you can see your complete financial situation.”

[embed_related]

Launched in April 2014, the platform already has 70,000 users of its aggregation technology, a figure that is set to double by the end of this year.

A key attribute of the system is its relevance to pension savers at all stages of the retirement planning journey.

The platform has a number of clever features, including a lifetime allowance tool that can forecast someone’s current level of contribution and values held in other schemes, and identify an equivalent cash value that would apply to lifetime allowance.

Any member whose fund looks likely to exceed 80 per cent of its limit will be prompted by the system to explore alternative retirement savings vehicles. Individuals can model additional contributions to understand if and when they might exceed the lifetime limit.

The Aon pension products can identify a range of triggers for different demographics to anticipate customer needs and feed them information in advance. It can also create bespoke ones and will indicate when someone might need help from an independent financial adviser to deal with specific issues.

The needs of pension savers nearing retirement are also well accommodated.

Aon defined contribution proposition leader Debbie Falvey says: “One of the key demographics are those pension savers who are ten years away from retirement. Given the recent changes to the pensions system, they really need to be thinking now about their investment strategy so their investments match their future retirement plans, but they also need to be supported in this.”

Aon defined contribution proposition leader Debbie Falvey says: “One of the key demographics are those pension savers who are ten years away from retirement. Given the recent changes to the pensions system, they really need to be thinking now about their investment strategy so their investments match their future retirement plans, but they also need to be supported in this.”

Provision of workplace financial education is patchy and is mainly offered by larger organisations, focused on mid-life and pre-retirement employees. In reality, demand goes beyond these two age groups.

Ms Falvey says: “One of the biggest financial education challenges of this new pensions environment has been created by pension auto-enrolment. We have a situation where people are being enrolled by their employer into the default fund and are lulled into a false sense of security. They need access to the right information and the tools to make the best decisions if they want the best outcome years down the line.

“With the pension freedoms people are having to make some really important decisions about their pension savings. Do they take the cash, draw down, annuitise or take a mix-and-match approach and do a combination? The platform’s modelling tools can help them create the flexibility they need.”

The platform also links to Aon’s annuity service, and can produce a quote based on aggregated pensions and an analysis of annuity versus drawdown.

“In a way, having more flexibility might encourage people to save more and allow them to plan a flexible retirement, perhaps taking a bit of their fund and winding down from their work gradually,” says Ms Falvey.

The pension reforms have highlighted the need for employers to support their employees with their retirement saving in a way that is both engaging and cost effective, and empowers pension savers to make the right decisions about their future finances.

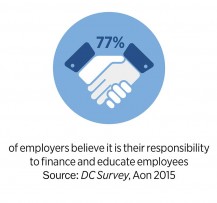

Sophia Singleton from Aon’s defined contribution team says: “Our research shows employers feel this is important and that they have a key role to play. Using technology will be vital to delivering the right outcomes.”

For further information on Aon’s financial education products:

www.aon.co.uk/financialeducation

0344 573 0033