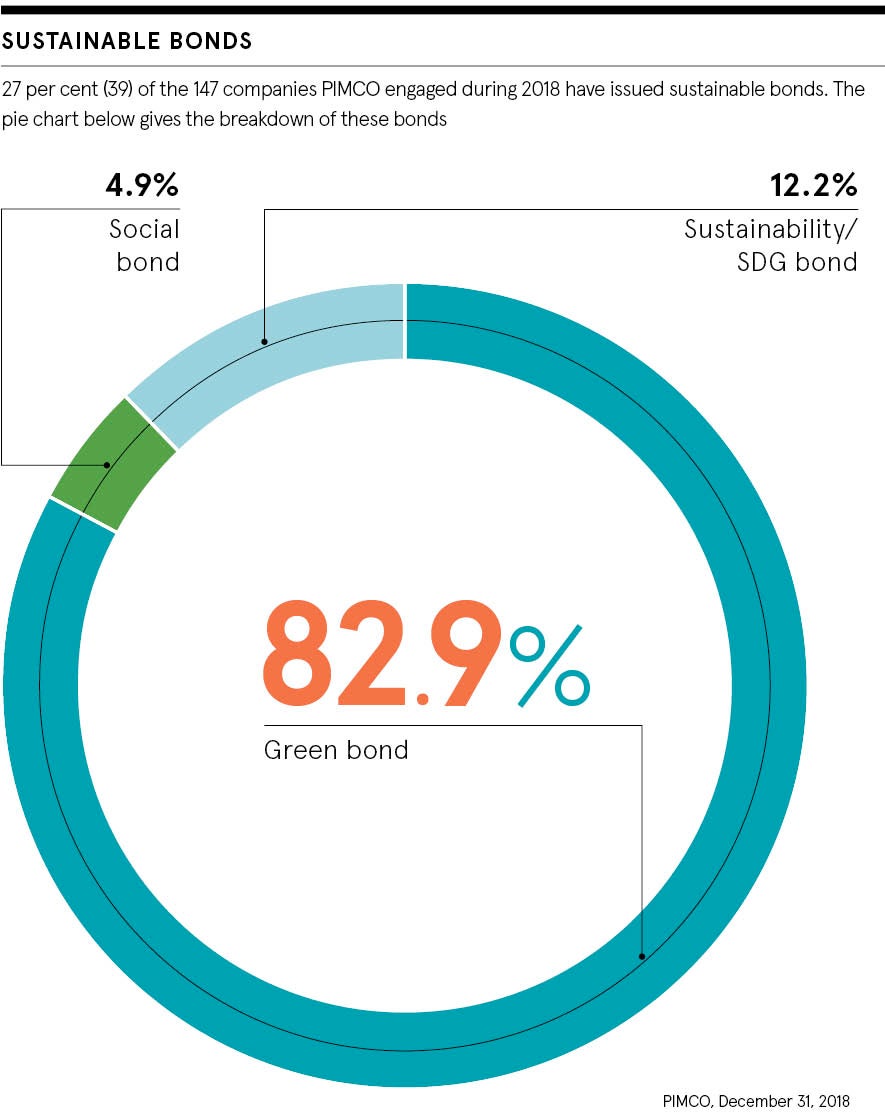

It was only two years ago that the world’s first Sustainable Development Goal (SDG) bond was issued. Twelve months later, leading fixed-income investment manager PIMCO reports that 27 per cent of issuers they engaged with unveiled sustainable or green bonds during 2018.

Fast-forward to summer 2019 and the UK government has announced plans for mandatory reporting on climate risk by pension schemes.

Changing times for investment

The sheer volume of environmental, social and governance (ESG) questions coming through now from asset owners and consultants is indicative of changing times, says Olivia Albrecht, head of ESG business strategy, at PIMCO.

“There is a groundswell of understanding today around ESG, and 2019 feels fundamentally different from 2017 and 2018,” she says. “Clients who historically focused only on the equity portion of portfolios are now increasingly interested in fixed income, with an upsurge in product development happening too.”

As asset owners target ESG and sustainable investment, issuers are also prioritising integration of practices and are on the lookout for projects to finance. So, while ESG may still largely be an emerging trend, its evolution is swift, notes Lupin Rahman, PIMCO head of emerging market sovereign credit.

“In 2017-18 you had a sharp acceleration in green bond issuance in the corporate space,” says Ms Rahman. “Now this theme is really moving into sovereign territory with green bond issuance by countries such as France, the Netherlands and Chile.”

In 2019 PIMCO received an A+ rating (highest score) from our UN PRI Assessment Report

The reach and remit of ESG is also expanding beyond the environmental domain of so-called green finance, aligning with wider SDGs.

This growth in demand looks set not only to continue, but increasingly see ESG factors formally incorporated into all investment decisions, not just dedicated ESG-labelled portfolios.

Furthermore, as understanding of economic effects improves, the market is rapidly realising ESG considerations are material in driving fixed-income and risk-adjusted returns, adds Ms Rahman.

“The old way of thinking was that ESG is just about doing good, but what markets are recognising more and more, be it related to environmental issues, social factors or governance, is that all these considerations have an impact on financial returns,” she says.

Key to ESG mainstreaming over time, however, will be the performance component, says Ms Albrecht. “One question that keeps coming up on the part of investors is whether an ESG-style approach means an automatic give-up of performance expectations. The answer is simple: no. There need not be a performance sacrifice with ESG if the opportunity set is sufficiently broad. In fact, what we need is something of a mindset shift to bust this persistent myth.”

Materiality, risk and 3Es

At PIMCO, ESG investing is underpinned by a fundamental focus on materiality of risks. Its integration is broad-based across the firm, involving every risk-taker and informing all aspects of fixed-income investment, rather than remaining a siloed sideshow.

This approach is systemic and strategic, explains Ms Rahman. “ESG is not a matter of reinventing the investment wheel. At PIMCO we have been thinking about factors that we deem drive returns over longer-term horizons for some time, incorporating cost-benefit analysis into bigger-picture sustainability planning,” she says.

Adopting a top-down perspective, as well as bottom up, for instance, means exploring how climate risk is going to impact macro-forecasting, which in turn affects central bank policies, then the stability of financial markets.

In part, this risk intelligence and forecasting capability at PIMCO is borne out of the natural behaviour cycle of the fixed-income market itself. Issuers have to come to market repeatedly to finance their debt position, which facilitates dialogue.

More specifically, the PIMCO approach to ESG follows a three-stage process, known as the 3Es: exclusion, evaluation and engagement. While exclusion and evaluation are familiar to investors, it is perhaps engagement that is the real differentiator around ESG, says Ms Rahman. “Our engagement activities help us to identify improving ESG issuers that may offer greater value add in terms of returns,” she says. “We want to influencethat process.”

With a significant credit analyst and IT team devoted to ESG, PIMCO is able to seize engagement opportunities effectively. As a consequence, its annual ESG Investing Report for 2018 reveals issuer engagement grew year on year, rising to 81 per cent from 69 per cent in 2017.

In total, last year PIMCO conducted over 5,000 meetings and calls with issuers at or near the C-suite level. This extensive, elite access enabled the firm to enjoy a highly representative cross section of open discussions with many chief executives and chief financial officers, often going beyond the usual financial and balance-sheet metrics to tackle targeted sustainable development issues.

Once again, the two top ranking SDG themes – climate action, and decent work and economic growth – remained the most important themes in 2018, with more than half of companies PIMCO engaged with highlighting these goals as priorities. Social issues such as gender inequality, standards of education and good health all ranked higher with issuers than in 2017.

Influence is investment driven

As an industry leader in fixed-income investment, PIMCO is better able to structure financial market securities to fit with sustainable investing considerations and mitigate specific ESG risks. PIMCO was also an early mover around what would now be regarded as ESG issues, having launched one of the first socially responsible bond funds in 1991, in the United States.

This position as thought leader effectively brings with it a responsibility for PIMCO, acknowledges Ms Rahman. “We are working with a large number of industry groups on ESG, whether UN principles for responsible investment (UN PRI) or central banks and government regulatory bodies. So, that role as a global citizen is very important in helping shape ESG policies and disclosures,” she says.

Just as $1.8 trillion in assets at PIMCO alone is significant, this collaborative potential is much bigger still, says Ms Albrecht. “Our influence is most powerful when we come together as an industry and collectively drive change, whether through the Sustainability Accounting Standards Board or via the Climate Action 100.”

Fundamentally, though, it remains vital not to lose sight of primary

business and financial drivers. She concludes: “At PIMCO, our ESG capabilities sit within the investment team. So they lean upon our in-house expertise across the full fixed-income universe. Ultimately, crucially, this is investment driven.”

Please speak to a financial adviser to explore new possibilities with PIMCO

Socially responsible investing is qualitative and subjective by nature, and there is no guarantee that the criteria utilized, or judgment exercised, by PIMCO will reflect the beliefs or values of any one particular investor. Investors should consult their investment professional prior to making an investment decision. PIMCO Europe Ltd (Company No. 2604517) is authorised and regulated by the Financial Conduct Authority (12 Endeavour Square, London, E20 1JN) in the UK. PIMCO Europe Ltd services are available only to professional clients as defined in the Financial Conduct Authority’s Handbook and are not available to individual investors, who should not rely on this communication. ©2019, PIMCO.

Changing times for investment

Materiality, risk and 3Es