Value needs to shift faster and real-time payments offer tangible benefits, ensuring the instant availability of emergency funds after a natural disaster, for example, or immediately confirming payments to release urgent medical supplies.

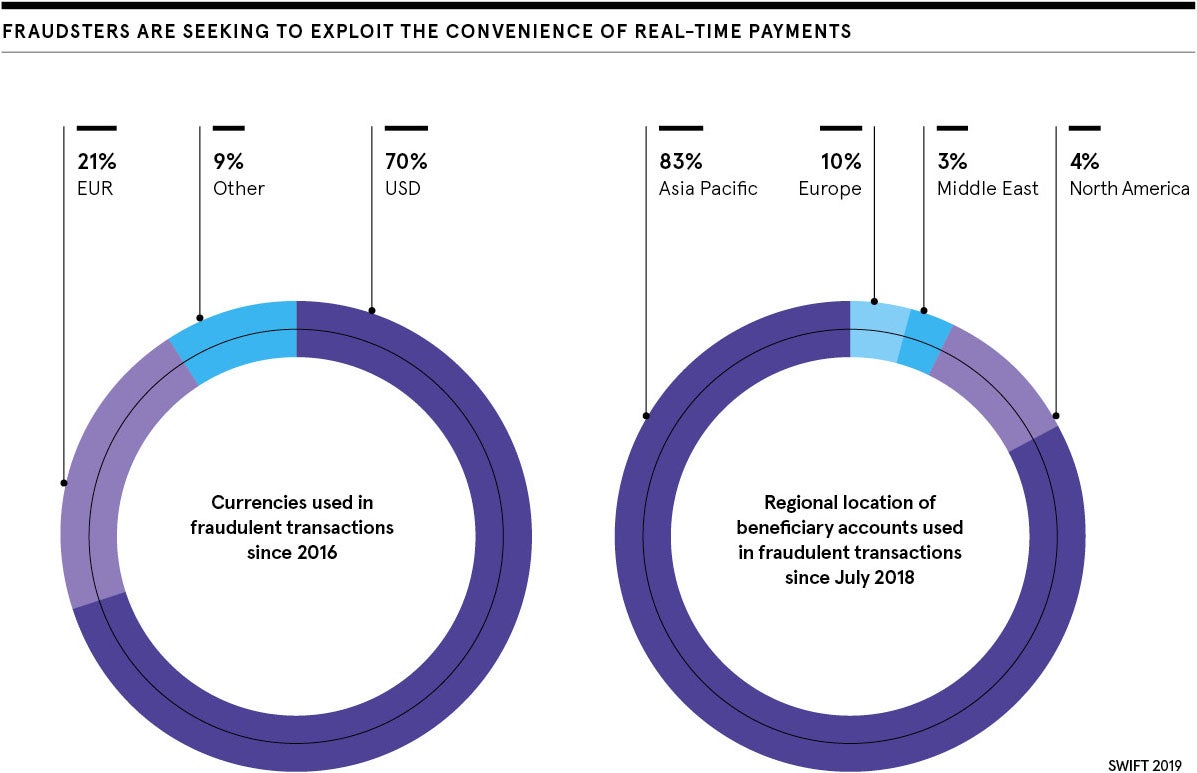

As payments move faster security is paramount. Criminals may seek to exploit the convenience of faster payments for fraud or money laundering purposes. And when a

payment settles instantly, the opportunity to recover funds is greatly reduced.

Speed and safety, therefore, must evolve in parallel to maintain integrity and security of the payments system.

While media attention has focused on consumer fraud in the context of real-time payments, banks are also collaborating to reduce the fraud risk across the global banking network.

Fighting back

“With real-time, cross-border payments, we need a new approach to fraud prevention that avoids and stops high-risk payments, rather than reporting after the fact,” says Tony Wicks, head of financial crime compliance at payments co-operative SWIFT.

“The game has changed. Compliance teams need to make quick decisions, more so than ever before. It’s increasingly important to try and take human error out of the equation. Transaction behaviour involves multiple institutions and is becoming more complex. So I think there will be increasing demand for tools and services at network level.”

SWIFT is driving community-wide solutions to enable fast and secure payments. Its Customer Security Programme (CSP) is at the heart, prescribing a set of regularly updated mandatory controls to create consistent security practices across its entire community.

“All financial institutions must meet this set of standards using clearly defined controls,” says Brett Lancaster, managing director and global head of customer security at SWIFT, who oversees the CSP. “All customers must attest their level of compliance every year. Failure to meet these controls means we report them to their local regulator.”

Importantly, financial institutions can also access attestation data to assess counter party risk. The financial ecosystem is interlinked, so everybody cares about the weakest link in the chain.

“Our customers are taking this seriously,” says Mr Lancaster. “About 95 per cent have attested to their compliance to the CSP controls covering about 99.5 per cent of all traffic across SWIFT.”

People, process and technology

The co-operative has developed technology-based solutions, such as the real-time application programming interface, built into the global payments innovation (SWIFT gpi). Banks sending and receiving data over the SWIFT network can pre-check the beneficiary account information with the ultimate receiving bank. This minimises the risk of misdirection to other accounts. More broadly, the use of artificial intelligence (AI) facilitates rapid scanning of very large datasets, helping to identify potential problems before they are processed.

SWIFT recently launched Payment Controls, a new tool to prevent and detect fraud, which helps banks monitor and protect their core payments, by flagging and responding to fast-moving, suspect transactions efficiently.

With real-time, cross-border payments, we need a new approach to fraud prevention that avoids and stops high-risk payments, rather than reporting after the fact

“The fact that you may have a payment refused because of fraud risk creates potential inconvenience for customers,” says Mr Wicks. “So we need to make the systems and processes accurate and precise when detecting fraud. This means we can help minimise fraud risk, as well as the impact on legitimate transactions. We are using AI and other methods to improve outcomes for customers.

“In the world of compliance, people typically want to slow things down and take longer to make decisions. That’s incompatible with the current thinking. So we need to change how we address these problems from a compliance perspective. If we can get this right, and I think we are going in the right direction, then it’s the supporting fabric that will make a difference to instant payments, especially within the cross-border world.”

For more information please visit www.swift.com

Fighting back