As the state pension age rises, workplace pensions are undergoing a transformation that has seen the decline of final salary schemes, a shift to defined contribution (DC) schemes and the introduction of auto-enrolment.

DC means each of us is in charge of our own personal pension pot, while the pension freedoms that came into place recently have given us more choice over what to do with that pot when we reach retirement age.

This increased individual responsibility and our increasing longevity means we should all be paying a lot more attention to our pension provisions than our parents had to.

Firstly we need to ask ourselves how much we’ll need for the retirement lifestyle we want, whether that is maintaining our current standard of living, planning to travel or live abroad, downsizing, or sharing our accumulated wealth with family.

The second step is to calculate how big our pot will need to be to fund the retirement lifestyle we are expecting. Often this then leads to the inconvenient realisation that we’ll need to set aside more now to ensure we are still able to exercise financial choice in the future.

One of the issues highlighted in recent research by BlackRock is that people tend to underestimate how much they need to set aside for retirement. The average person in the UK thinks a pension pot of £230,000 will be enough for a retirement income of around £26,000, when they really need at least double that, even with the state pension.

So how do we take more control of our future? How can we better ensure that we have the financial resources to decide when and how we retire? Claire Finn, BlackRock’s head of UK strategic partnerships and DC investments, advises using a simple equation for retirement income (see graphic).

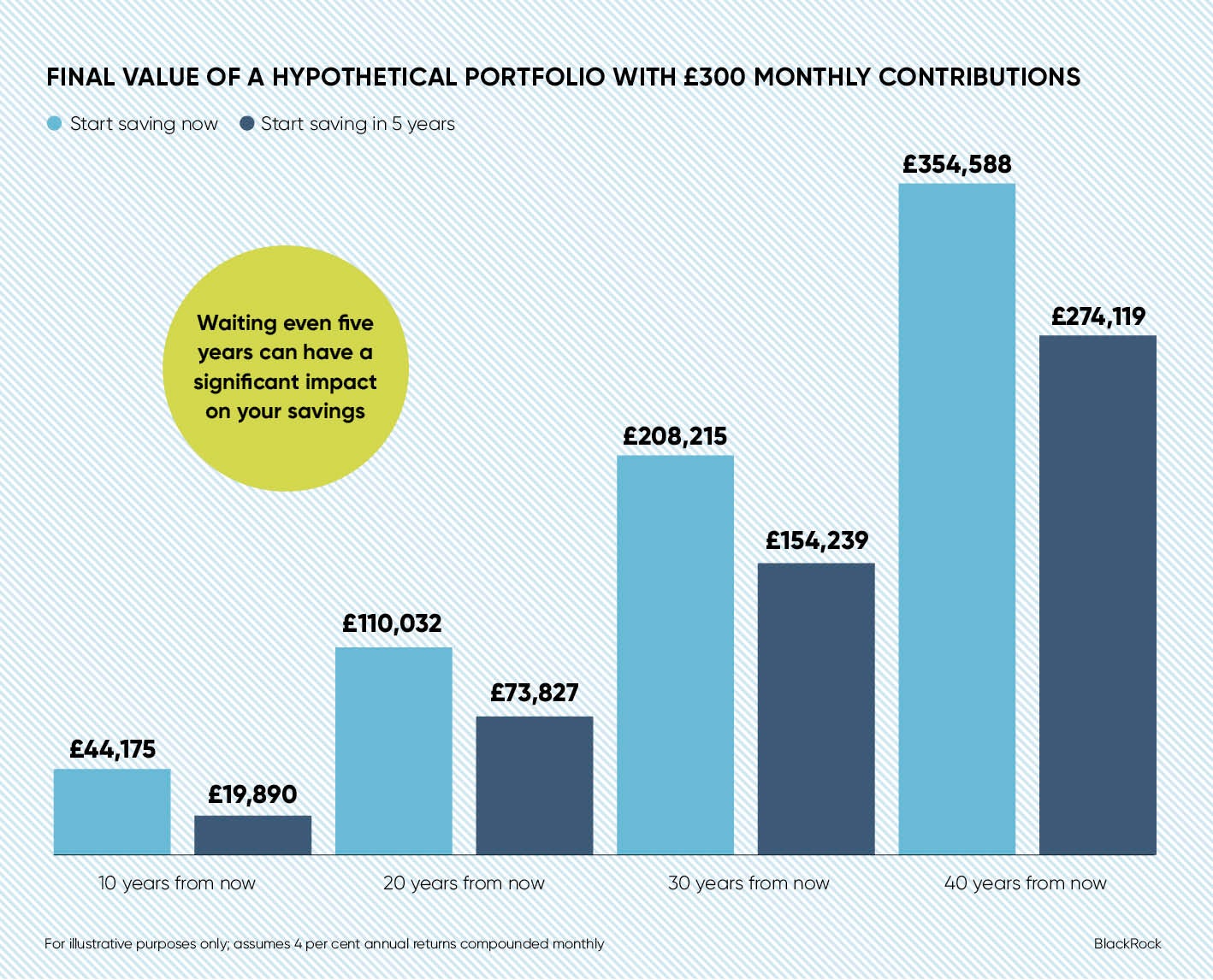

The biggest influence on how big our pot will be is how much we are putting into it. For those young enough to start saving towards retirement early, the power of compounding should not be underestimated. The longer something has to grow, the more this growth snowballs.

For the rest of us, the biggest lever we can pull is to put more money into our pensions.

Ms Finn says: “It is common sense that we can’t save for the future in the future. Money put towards retirement should be regarded as deferred gratification rather than a sacrifice. If most of us could look into our future and see the choice between a happy retirement or one full of compromises and sacrifices, we would probably do more now to ensure we don’t let ourselves get into the latter position.”

Raising contribution levels is something that everyone can consider, whether employed or self-employed. It is something which auto-enrolment will do in two sharp steps over the next two Januarys to get people in the workplace up to a total contribution of 8 per cent of pay.

Auto-enrolment has brought millions more people into workplace pensions, which is a tremendous achievement. However, there remains the danger that employers and employees will feel they have done enough by enrolling, and will not take a step back to consider the hard reality that recommended combined contributions are closer to 15 per cent.

Many employers already have well-established retirement schemes, but they still have a crucial role to play in helping to provide for the retirements of their employees.

People tend to underestimate how much they need to set aside for retirement

They can make an immediate difference by increasing employer contributions, but they can also encourage smarter behaviour among their staff by offering to match employees’ increased payments.

In addition, Ms Finn believes the UK could learn something from US-style auto-escalation schemes such as Save More Tomorrow where employee payments are ratcheted up at regular intervals to ensure savings increase over time.

The next part of the equation – returns – is particularly important when interest rates are at all-time lows, dividend yields are low by historical standards and returns on government bonds look set to be weak for some time.

In workplace DC schemes, a lot of work is put into building a robust default investment approach. The reason? Typically, nine in ten of us keep our money in our scheme’s default fund, so the duty falls to the custodians of the pension scheme to provide us with something which broadly fits all.

However, a focus on cost can often drive these trustees and advisers to the cheapest investment offering, even if these are not the most fit for purpose. Although BlackRock is a market leader in low-cost index funds, Ms Finn believes most clients are best served by a blend of investments which target a specified outcome within cost constraints.

She says: “In an era of low returns, getting a good rate of return is much more important than shaving a small amount off costs. The key question is ‘have I selected a good blend of investment approaches to reach my goal?’”

Sophisticated investment approaches have been made more accessible and affordable by competition and innovation. These help to reduce the reliance on raw market performance for returns. Examples include multi-asset funds, which hold a combination of shares, bonds and cash, or alternative investment funds covering the likes of private equity, property and infrastructure.

Another option is smart beta, which screens shares by different criteria such as dividend payments or how volatile the stock has been over different time periods.

“Schemes need more tools in the kit,” adds Ms Finn. “What worked well when interest rates and returns on equity were higher will not work in an environment of low returns.

“Your typical woman or man in the street doesn’t wake up in the morning thinking about their pension, but it’s something everyone will have to pay more attention to, whether that’s the individual giving themselves a better chance of a comfortable retirement by increasing contributions or schemes finding the best balance between returns and costs.”

For more information please visit www.blackrock.com/institutions/en-gb/solutions/defined-contribution

Issued by BlackRock Investment Management (UK) Limited, authorised and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL. Tel: 020 7743 3000. Registered in England No 2020394. For your protection telephone calls are usually recorded. BlackRock is a trading name of BlackRock Investment Management (UK) Limited. Past performance is not a guide to current or future performance. The value of investments and the income from them can fall as well as rise and is not guaranteed. You may not get back the amount originally invested. Changes in the rates of exchange between currencies may cause the value of investments to diminish or increase. Fluctuation may be particularly marked in the case of a higher volatility fund and the value of an investment may fall suddenly and substantially. Levels and basis of taxation may change from time to time. Any research in this document has been procured and may have been acted on by BlackRock for its own purpose. The results of such research are being made available only incidentally. The views expressed do not constitute investment or any other advice and are subject to change. They do not necessarily reflect the views of any company in the BlackRock Group or any part thereof and no assurances are made as to their accuracy. This document is for information purposes only and does not constitute an offer or invitation to anyone to invest in any BlackRock funds and has not been prepared in connection with any such offer. © 2017 BlackRock, Inc. All Rights reserved. BLACKROCK, BLACKROCK SOLUTIONS, iSHARES, BUILD ON BLACKROCK, SO WHAT DO I DO WITH MY MONEY and the stylized i logo are registered and unregistered trademarks of BlackRock, Inc. or its subsidiaries in the United States and elsewhere. All other trademarks are those of their respective owners. All financial investments involve an element of risk. Therefore, the value of your investment and the income from it will vary and your initial investment amount cannot be guaranteed. Overseas investment will be affected by movements in currency exchange