Why has engagement become an increasingly important metric in the pensions industry?

It’s largely been driven by the shift from defined benefit (DB) to defined contribution (DC) pensions, accelerated by the introduction of auto-enrolment in 2012 and then further regulatory changes in 2015 giving DC scheme members more control over their savings. In a DB scheme, engagement isn’t terribly important. As long as you stay employed until your retirement date, you can have a degree of certainty about what your retirement income is going to be. It is very simple to understand. DC schemes, on the other hand, are far more complex. As households invest in assets, which have a degree of risk and evolve dynamically, retirement income is less certain and influenced by personal investment decisions and the degree of risk taken on. If something is more complex and less certain, and it needs people to understand a lot more about what they are doing, it requires greater engagement.

Has engagement in pensions increased over the last decade?

Yes, but not by enough. We’ve been tracking engagement, at the highest level, since we first entered the workplace pensions market in 2011. In 2012, around 10 per cent of people viewed their pension online at least once a year. Now, it is just over 30 per cent, so a threefold improvement. While it is great that one in three people now engage with their pension digitally, at least once a year, that means two-thirds still don’t, so there is clearly a long way to go.

How is technology able to increase engagement further?

There are a number of ways, one of the most important of which is personalisation and answering questions that are meaningful to each person. Every pension scheme member should be able to visit a mobile app or website and immediately understand, in a digestible format, how much they’re going to receive as a retirement income based on what they’re currently saving and what products they’re saving into. In the DC world, we present this income as a likely range, along with educational information on how they can influence that. People now retire at different ages and in different ways. For example, some take early retirement or semi-retire, while others come in and out of retirement, so it is essential we help people to personalise their pension to their own specific needs. Technology is making this more interactive and it is also allowing people who haven’t traditionally been able to afford a financial adviser to access personalised robo-advice, which is becoming a really important service.

Technology has played a fundamental role in sustainable cost-reduction and access to growth investments for UK households

Are you finding that savers are also becoming more interested in the specific companies their money is invested with?

Increasingly so, but I think a lot of people still look at their pension fund and have no idea that underneath it they are probably invested in some very exciting businesses, which really interest them, such as Amazon and Tesla. Technology can increase engagement in the economy more broadly by helping people to understand they are directly participating in some of the greatest innovation taking place around the world. Equally, it allows them to directly influence issues that are important to them on a personal level. Without compromising the importance of professional asset management for their lifelong savings, they can influence the extent to which their pension has a positive social and environmental impact based on the particular companies it invests in. Technology can allow them to not just see the impact of their investments, but set constraints on certain things they care about as well. For example, if they don’t want to invest in companies which contribute adversely to climate change, they can set constraints around that. Half the world’s capital comes through pensions from median-income household savings, and technology is crucial to giving savers a direct role in how their money is allocated and the effect it has. By doing so, it not only boosts engagement in pensions, but helps direct capital towards companies helping to build a more sustainable future.

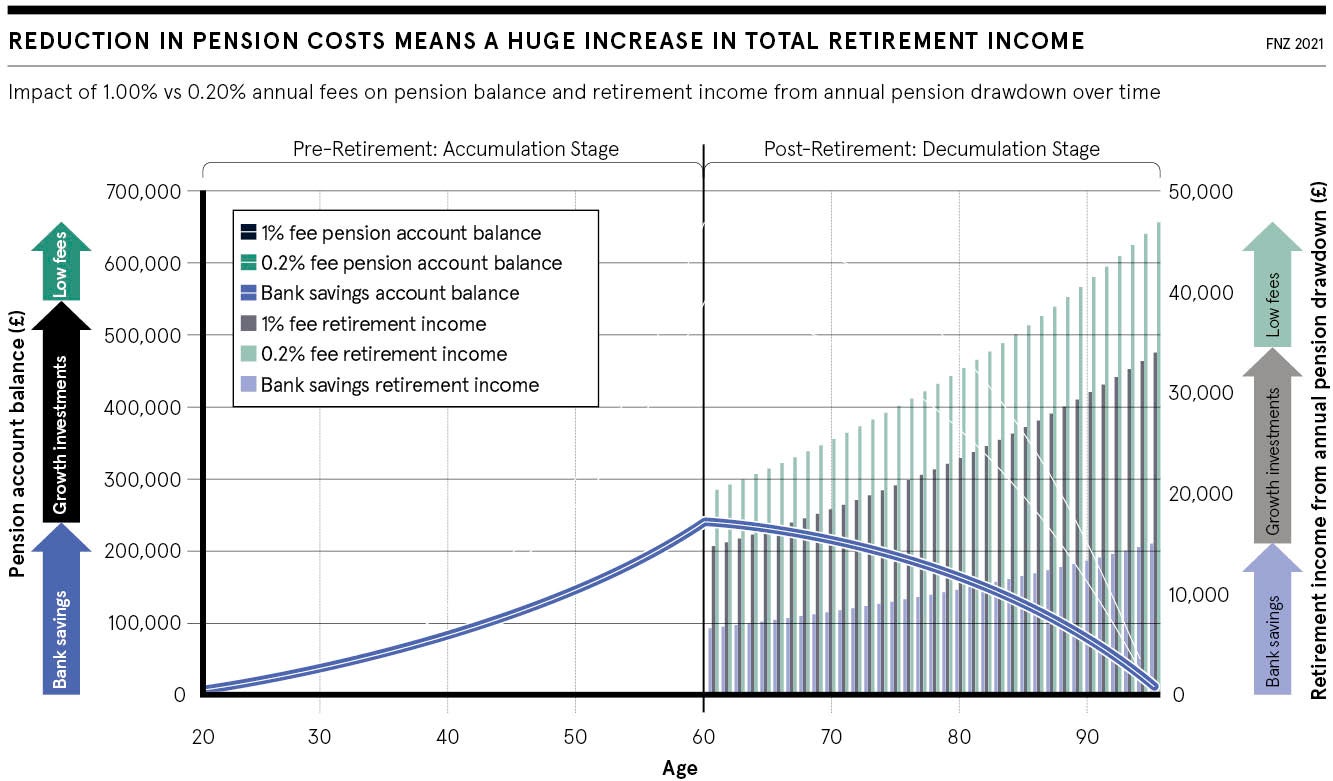

Automation is most commonly associated with cost reductions; is this also the case with pensions?

Undoubtedly, and it’s more closely linked to engagement than you might think. At the simplest level, technology removes the need for paper, which has historically featured heavily in workplace pensions due to the number of forms that needed to be completed. If every time I want to do something I have to fill out a piece of paper, that makes me less likely to do anything. By taking it further and automating the entire end-to-end process, the impact is transformational. Ten years ago, pension admin and investment costs ran at 1 per cent a year or more. Today, certainly in a large UK employer, it is around 0.2 per cent. That reduction over 30 to 40 years of retirement savings actually increases your median household retirement income by about 40 per cent, which is huge. That situation is even more transformational, if households consistently save and allocate their investments over the long term into growth assets, rather than bank deposits. Technology and automation have played an absolutely fundamental role in both sustainable cost-reduction and access to growth investments for UK households.

What is your vision for the future of pensions?

Our ultimate vision is everybody has a personalised pension that is tailored to how and when they’re going to retire and their individual preferences around how their funds should be invested, according to their interest in key themes, such as sustainability and diversity. Pensions will be accessible entirely through mobile and will help people, with virtual personal financial advisers, not just in the workplace, but as they transition into retirement or some form of flexible retirement. Clearly, delivering that kind of personalisation and engagement to ten to twenty million households requires sophisticated technology and algorithms. FNZ and the industry at large is about a third of the way to delivering this vision and we are firmly focused on getting there as quickly as possible. We are also investing heavily in bringing the savings, retirement and wealth management platform, which we have successfully built here in the UK, to other key international markets.

Sponsored by

Why has engagement become an increasingly important metric in the pensions industry?

It’s largely been driven by the shift from defined benefit (DB) to defined contribution (DC) pensions, accelerated by the introduction of auto-enrolment in 2012 and then further regulatory changes in 2015 giving DC scheme members more control over their savings. In a DB scheme, engagement isn’t terribly important. As long as you stay employed until your retirement date, you can have a degree of certainty about what your retirement income is going to be. It is very simple to understand. DC schemes, on the other hand, are far more complex. As households invest in assets, which have a degree of risk and evolve dynamically, retirement income is less certain and influenced by personal investment decisions and the degree of risk taken on. If something is more complex and less certain, and it needs people to understand a lot more about what they are doing, it requires greater engagement.