SPONSORED BY Openpay

What is Openpay?

We are a payment service which enables customers to buy the things they want and need now and pay later. Repayments are made in equal installments each month, normally from three to seven months. Let’s say you want to buy a new £200 coat. With Openpay this can be split into four equal payments of £50. Following an initial upfront payment, each payment is then debited automatically every month. At the end you’ve paid exactly £200, no more than before.

Why do consumers prefer it?

It’s a great way to manage cash flow. Even medium and high earners may prefer to spread payments to avoid getting into debt or running out of funds before pay day. Openpay is a hassle-free alternative to credit cards and overdrafts. Our model is so clean and simple. There’s no interest and no fees, if you repay on schedule. No complex paperwork. Consumers buy now and spread the payments over time.

We lend responsibly and we’re proud of it. We return merchant fees on any refunded items. That’s our point of difference

Why do businesses offer Openpay?

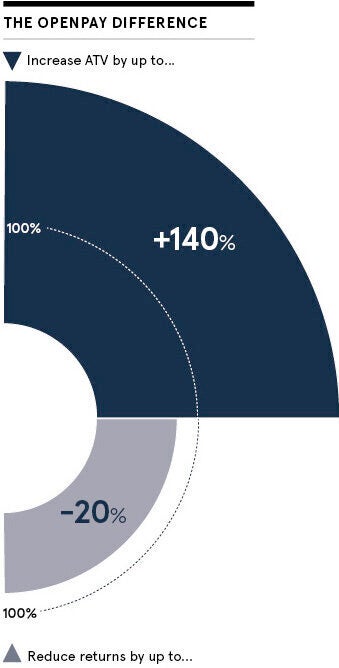

First, Openpay can significantly improve basket size by allowing consumers to overcome cash-flow bottlenecks. Second, it drives loyalty. Consumers value being allowed to spread payments and shop with brands that offer them the services they want. Third, is speed. Businesses get paid in full right away, unlike other finance products which dribble cash over time. And finally, is our impact on returns. We ask consumers to make the first payment up front. This cuts buyer’s remorse. In fact, returns can be cut up to 20 per cent this way. This is proving a game-changer for companies that offer Openpay.

Is it just for online retailers?

It’s for everyone. We work with JD Sports, Watch Shop, Fulham Football Club and others across fashion, home, beauty and lifestyle, so we can see how powerful Openpay is for retail brands. In Australia, where Openpay is headquartered, we are there for consumers across all areas of their lives. As well as retail we are also strong in automotive for MOTs, accessories and tyre changes, home improvement, and healthcare for dental services. Pet stores and vets offer Openpay too, and we have recently entered the education and membership verticals. Openpay is for all sizes, all sectors.

You charge consumers no fees or interest, so how do you make money?

You charge consumers no fees or interest, so how do you make money?

It’s true, we charge consumers no interest or fees if they pay on time, the final sum will be the same number they see at the checkout. Naturally, there are charges for late payment, but this is more about incentivising good behaviour and only issued as a last resort. We work with consumers to ensure they don’t get into trouble. Our revenue comes from a small percentage of the transaction from the merchant. It’s slightly more than a credit card transaction. The real value to the merchant is that we drive their key performance indicators higher, such as conversion and loyalty, but with average transaction value, or ATV, increases being the main one. Offering Openpay typically increases transaction value by 80 to 140 per cent.

What makes you different to other providers?

Our model is unique. Other providers tend to offer shorter repayment times of two months or less. We offer up to six months, which means each monthly payment is lower and the ATV increases are much higher. Repayments are monthly, whereas other buy-now, pay-later providers typically offer weekly or fortnightly payments. Frankly, I can’t see the point of weekly or fortnightly payments, when pay days in the UK tend to be monthly. We are also incredibly customer centric. If consumers struggle to repay on time we talk to them, support them and respond to their needs. Our Trustpilot score is 4.8 out of 5; that’s better than anyone else in our space.

How straightforward is Openpay to implement?

It’s not a complicated product and we have a lot of great technology to accelerate implementation. Our systems are cloud based and connect via an application programming interface, or API, to the retailer’s platform. We have been fully integrated into many of the leading ecommerce platforms in the UK, such as The Hut Group’s Ingenuity platform, Retail & Sports Systems and Venditan. We’ve also built software development kits for a number of other ecommerce platforms, such as Salesforce Commerce Cloud, SAP Hybris, Magento and others. We’ve had merchants integrate in days. Realistically, I would say it’s a week to ten days for a development team to plug in and solve backend reconciliation. And a bit of time to test and run analysis. So start to finish is probably up to a month.

We want to help consumers gain control over their finances. We believe that together we can improve the entire shopping experience

Who are Openpay?

We are an Australian company, listed on the Australian stock exchange (ASX:OPY). We were founded seven years ago, by a team who wanted to improve on the concept of a “lay away”, the old-fashioned notion of asking a store to hold a product for you and each week or month paying an instalment until you’ve paid in full. They asked why you couldn’t get the product straightaway and pay later. We were one of the first to launch buy now, pay later in Australia. Today we have merchants in Australia and New Zealand are fast expanding in the UK.

If a company wants to offer Openpay, what are the next steps?

Visit our website and get in touch. One of our sales team will contact you and talk about your needs, about what you are trying to achieve and how your business can adopt Openpay. Our website answers a lot of questions in detail. Our mission is to change the way people pay for the better. We want to help consumers gain control over their finances. We believe that together we can improve the entire shopping experience.

To find out more please visit openpay.co.uk or get in touch by contacting the team via [email protected]

We lend responsibly and we’re proud of it. We return merchant fees on any refunded items. That’s our point of difference