How are online payments changing?

It’s not uncommon to see an Alipay or WeChat Pay logo outside Asia as retailers realise they can win more customers by supporting their preferred payment method. “Buy now, pay later” payments have also shown high adoption, helping retailers to maximise basket size and allow access to premium products by spreading out or deferring the payment. Meanwhile, Payment Services Directive 2 imposes a requirement for strong customer authentication, or SCA. There’s confusion around exactly what that means with regulators across Europe differing on the enforcement of the regulations, and both retailers and issuing banks showing varying degrees of readiness. When coupled with emerging payment methods, it makes for a complicated landscape to navigate.

Can brands keep up?

Online brands want to focus on their core offering and customers, not get distracted by new payment methods or how to comply with new payment regulations. Of course, they know that offering the best checkout experience, including the payment method customers want to use, provides a competitive advantage, so they can’t ignore these changes either.

What are the benefits of improving the payment process?

With the right payments solution, retailers can improve conversion, reduce costs and curtail risk. For example, on risk reduction, some payment types have lower reversal and chargeback rates, reducing exposure to bad actors. Plus, as retailers become increasingly global and look to grow their customer base through market expansion, they must think about unique, local payments landscapes. Solutions that allow retailers to accept any type of local payment from any country can meaningfully support a company’s long-term growth, while streamlining internal payments operations.

How can online retailers and services stay up to date?

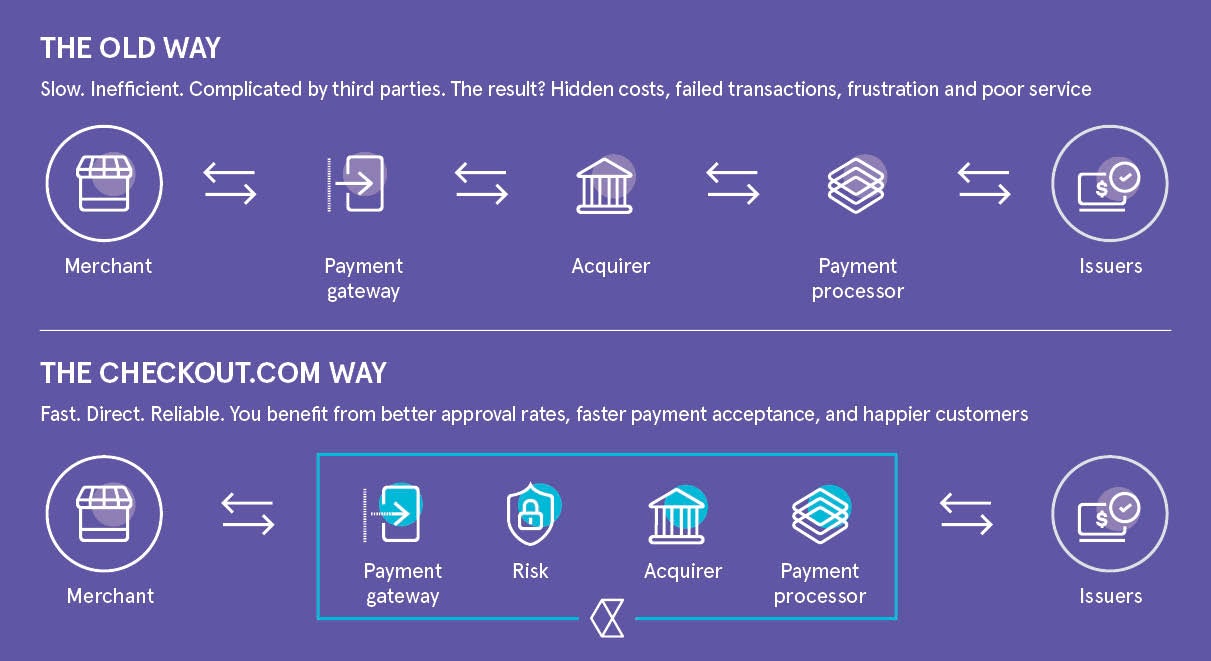

It’s critical to find a payments partner that can seamlessly and successfully support hundreds of currencies, any payment method and navigate nuanced regulations. Checkout.com offers a unified payment platform, so no matter what payment method you want to offer, it is a part of our repertoire. These include Alipay, Klarna, Union Pay, Visa, Mastercard, Apple Pay, Qiwi, iDeal and many others. In theory, a retailer could offer these by working directly with each payment service, but it’s an absurd amount of work. You could be looking at 20 payment methods in a region, each requiring integrations, unique reporting formats and settlement flows. Instead, we provide everything via one integration, with back-office and settlement services normalised irrespective of the payment method or market. We service both startups and established global giants, such as Samsung, Virgin, adidas and TransferWise.

What about stability?

Most payment systems run on technologies built before the first smartphone was available. As payments increase, so does the strain on these systems, leading to interruptions. The Financial Conduct Authority has been vocal about the negative impact of outages, noting that systems failures in the industry are increasing. This instability is unacceptable, but avoidable. We built our platform around a modern architecture, leveraging the latest technological standards. There are no finite limits on what we could process and stability is an asset when compared to the wider industry.

Finally, what is your advice for retailers when it comes to payments?

We’ll see new payment methods, new card processing features. This could make life harder for companies. But if you partner with a provider that can help you offer the payment choices your customers want, and with the agility to adapt and capitalise as the sector evolves, you’ll be at the forefront of online retail, no matter how the market changes. A payment partner can help your business cope with the torrent of requirements. Our model is based on our clients succeeding and the core reason why businesses choose us to help them enhance and expand their payment functions.

To find out more please visit checkout.com