“We are on a journey from data to information and from information to insight,” says Chris Probert, UK data practice lead at consultancy Capco. “We are trying to teach people a language they can use to talk about data so they can use it to drive value.”

Getting a faster or deeper understanding of a situation can enable a business to seize opportunities ahead of the competition. That level of insight resides within the data that a financial services firm collects. Yet without an adequate level of focus, businesses can struggle to realise that opportunity.

“Those people gathering data within banks have not necessarily thought of data as an asset to use for driving more sales or getting more insights around customers,” says Christer Bergquist, managing principal of Capco Sweden. “So an educational aspect falls upon the CDO to inform the wider bank about how data can be used to drive increased revenues. That is a cultural change.”

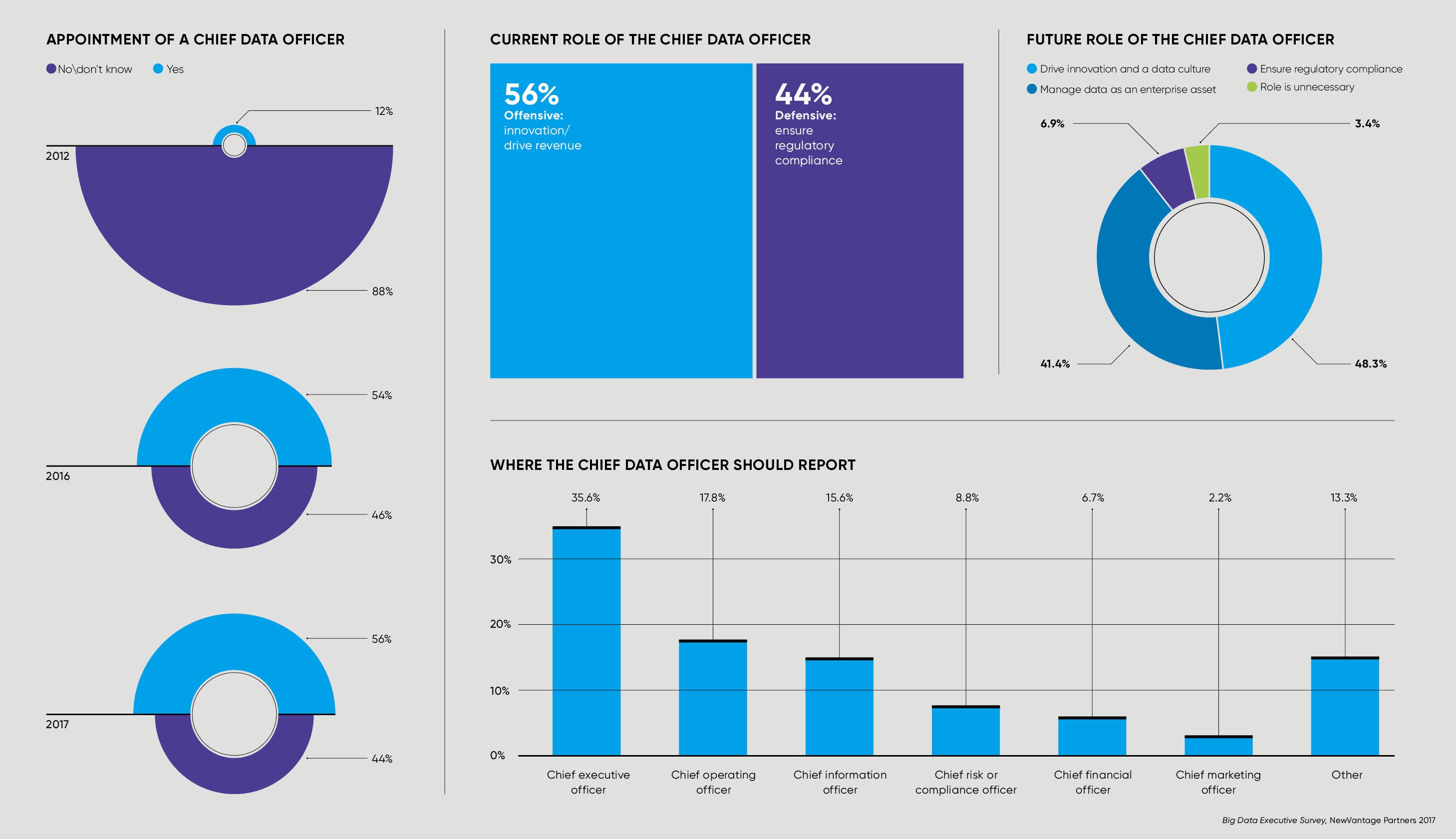

Making a cultural change of this nature is predicated upon the agenda of the CDO and their influence. Many finance houses first developed the positon as an offshoot of either their IT or business functions, depending on the relative strength of those two parts of the organisation.

Data management is an evolving industry, so banks and the industry are looking for vendors to partner with to develop tools and methodologies

In its early incarnation, the role was driven by the increased volume of data that businesses needed to manage and process to comply with the growing regulatory burden. The Comprehensive Capital Analysis and Review (CCAR), which was rolled out in 2013, required bank holding companies with US operations and more than $50billion of assets to reconcile risk and finance data to support consistent reports for management and regulation. The Basel Committee on Banking Supervision (BCBS) 239 regulation imposed principles for effective risk data aggregation on global systemically important banks and domestic systemically important banks from 2013 onwards.

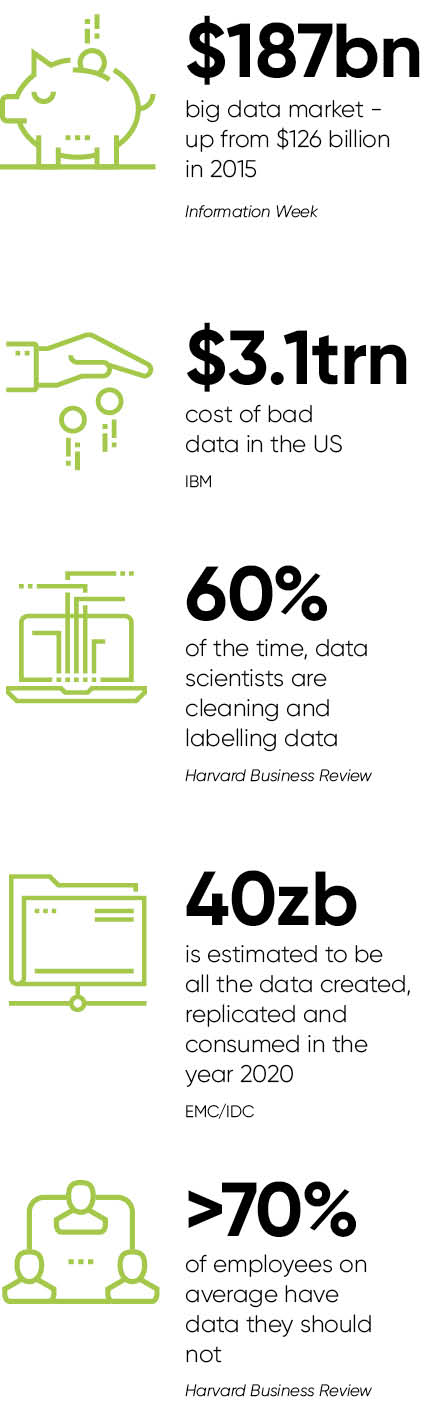

Poor data dogged the banking industry prior to the 2008 crash. A combination of revenue-chasing and firefighting that occurred post-crash left banks unable to focus on quality issues.

“People have been complying with regulation at such a pace that they have not had time to fix the data quality,” says Steve Hargreaves, partner for UK capital markets at Capco. “They have had to get reporting for the many deadlines that came one after the other. Now they are coming to a point where the data quality is incredibly poor and it’s patently costing them money. They are missing opportunities to save cash and capital, and drive revenue.”

REFINING THE BUSINESS

BCBS 239 and CCAR provided the regulatory impetus to take this issue seriously. The skewing of budget towards compliance projects allowed BCBS 239 and CCAR to function as Trojan horses in prioritising the understanding of, and resource allocation towards, data quality.

Building a picture of capital requirements, risk models and the accessibility of data gives banks an understanding of data throughout the enterprise to help them meet compliance demands. Naturally this information provides firms with a lot of information about their organisation that they could use to make strategic decisions.

Having gained insight, several top-tier banks have stepped away from major markets in recent years. Moreover, the domain knowledge around the data held within the firm and what it represents can be used to make both business and compliance decisions. This has naturally strengthened the CDO’s hand.

Nevertheless, there are technological steps that need to be overcome to give the CDO the flexibility to move along the chain from data to insight. Data management is an evolving industry, so banks and the industry are looking for vendors to partner with to develop tools and methodologies.

Many firms are reviewing their big data programmes, which have been very expensive and struggling to meet expectations on cost-savings. Some early adopters are now looking at developing data solutions, which treat the movement and storage of data like a supply chain, more akin to how Amazon looks at its stock than how banks have traditionally looked at data.

“People have started to realise their organisations, their people and their data are connected like networks, and that they should be using technology which is more akin to relationships and networks,” says Mr Hargreaves. “However, the technologists in banks are culturally very aligned to traditional solutions. So there is a lag as people get used to the new technology.”

Experience with those technology projects has made organisations cautious towards rapid change and the accelerated adoption of new types of technology. Yet this has improved the industry’s capabilities in rolling out new technology. It has also embedded the need for a strategical approach to investment.

“On technology, firms must not get ahead of themselves,” says Mr Probert. “The development of a strong data culture is core. However, smart CDOs are the ones who think and talk about four-to-five-year paths when deciding what to do. When they look to drive value throughout the chain and how to evolve potentially greater analytics, agreeing on clear data principles in their IT strategic roadmap is key to long-term success.”

He notes that Capco believes that connected data drives business value. The implementation of programmes that by connecting data enable the CDO to drive a whole range of automation, customer services and offerings will transform the role. The CDO will move from building data management foundations to creating true value. The strength that many digital firms have access to good data and the capacity to run meaningful analytics across it will be a central element of the CDO role within financial services for the next five years.

“Looking at a diagram of their job today, the CDO is 80 per cent data definitions, lineage and quality,” says Mr Probert. “We will see that pivot to 20 per cent of the role, with 80 per cent being analytics and driving value from data.”

CDOs will need to find that middle ground between business and IT to engage effectively with the business, and be able to communicate effectively with them both.

“IT looks at the landscape and architecture, and how the systems are put together. The business focuses on parts that help them hit targets,” says Mr Bergquist. “I think the CDO needs to consider finding that common language around data and how it is shared within the organisation, so irrespective if you talk to IT or talk to the business side, you have a common understanding. Helping firms find this middle ground to drive true value is the big challenge we focus on helping our clients with.”

Mr Probert adds: “If CDOs can’t find this balance then they will quickly lose their unique position.”

For more information please visit: www.capco.com

Q&A: What makes an effective chief data officer?

James Arnett, partner at Capco, explains the key skills, structures and powers that enable a chief data officer (CDO) to build a new way of working

Where do you see the most effective CDOs?

Pharmaceutical, retail and some modern technology firms are more advanced in the way they use data than financial services. But the role of the CDO, in financial services, has risen significantly in importance over the last two to three years. Many firms are now starting to realise that they do need a CDO and are establishing this function within their companies. CDOs are already helping companies to use data more effectively. For example, they are creating data management functions, data ecosystems and linking these parts up.

How has the CDO’s position within business changed as that evolution progresses?

Legacy data management roles have typically settled in IT and have been misaligned, had limited scope or limited accountability. We are now seeing the new prominence of the data agenda is driving the CDO to a position in which they have their own mandate rather than operating at the behest of the chief technology, operating or risk officer.

So is it a transformation role?

It’s not a transformational role, it’s a foundational role to provide, inform and enable transformation. I think the CDO is going to be the powerful function that will enable the kind of transformation which was not possible in the past.

How has the pressure to report data to regulators contributed to this?

Understanding data front to back is enabling companies to make both business and compliance decisions. And it’s allowing them to have conversations with their regulators about what good data management looks like. It’s also helping companies to decide what business they do and do not want to do. So it’s given them more control. One of our clients has off-boarded and exited certain markets because they used data analysis effectively to analyse their business. Others have decided to push further into different business areas because they realise they still have the potential to expand or they are able to have a more sensible conversation with their regulator.

What tangible impact will a data-enabled bank have over its rivals?

Five or ten years ago, the high street banks had difficulty offering their whole product suite because data wasn’t shared effectively across the bank. Siloed technology and legacy information means, even today, this is still the case at many banks. New technologies and the need to serve clients digitally has made them realise the power of data, and the importance of sharing and managing data across silos to make effective business decisions.

How does that affect the customer?

From the customers’ perspective firms that get better access to data, or get real time data, can offer new digital platforms, new services and increase offerings across different markets. Anything that you as a customer might expect, everything from really personalised retail experience, to moving assets in a very straightforward way, to seeing wealth getting moved from one generation to the next is predicated on the financial services firms having really good data. Without good data, banks are going to struggle to meet your expectations. The role of the CDO will be a key enabler for the digital offerings that banks need to provide to keep relevant and survive in a modem economy.

Are incumbent banks at risk from newer rivals that are more data literate?

Yes and no. Newer banks are not limited in the same way as incumbents that tend to have longstanding legacy systems. This makes the transition to new technologies easier. However, even though incumbent banks were slower to move on the utilisation of data, we are now seeing adoption among some of the larger banks as well as the new challenger banks. They are now learning how to use different data sources, including datasets that are available out in the wider world, such as on social media. How they use that kind of technology to go to market and the market segments they offer in the digital space for banking are very interesting concepts.

Where are the larger firms in the process of adoption?

I think the use of different technologies, for example how to use cloud, how to use the processing power, is a journey. I know a certain number of banks that are trying different elements of new technologies in a private space. The biggest challenge I see with our client base is the deployment of these new technologies, which are in their infancy or are evolving in themselves, while competing with the wave of regulation. A lot of the solutions that are developing to handle capital market regulations are being driven around developing data lake concepts in which vast amounts of raw data are held in their original form. Deploying new technology solutions while delivering at the same time is a big challenge. It takes strong leadership and strategic thinking on the part of the CDO to walk the fine line between meeting short-term compliance milestones and doing what is right for their organisation strategically in the long term.

REFINING THE BUSINESS