Mobile network operators (MNOs) have seen the demand for voice and messaging services diminished by internet-based communication platforms such as WhatsApp and Viber. The GSMA, representing mobile operators, reports that traditional voice revenues have declined by 56 per cent over the last five years and, overall, ARPU (average revenue per user) is down 12 per cent. At the same time, other over-the-top online services such as Netflix and Spotify are selling entertainment services directly to millions of increasingly content-hungry consumers.

Mobile operators looking to build up their position and meet consumers’ appetite for digital services as new opportunities present themselves, should be especially focused on emerging markets. Close to one billion new mobile connections are forecasted over the next five years in these regions and, according to m-commerce technology firm Upstream, MNOs have the opportunity to capture a share from a potential $70-billion digital opportunity in emerging markets. Operators have unique assets, which put them in a prime position to engage with customers and boost their revenues. Only if these assets are utilised effectively, however, will they be able to make the most of this opportunity.

Brand equity

The GSMA has found that consumers are increasingly ready to trust mobile operators with their finances. In December 2015 there were almost as many active mobile money accounts as active PayPal users for the first time. Marco Veremis, chief executive and co-founder of Upstream, a leading mobile commerce platform, comments: “In emerging markets, mobile network operators deliver a crucial service, often providing consumers their only window to the world. Operators, as day-to-day consumer brands, are highly recognised and trusted.”

Research commissioned by Upstream found that consumers in emerging markets want more access to health (26 per cent) and financial services (23 per cent) on their mobile devices, as well as utilities and tools (21 per cent), such as battery or memory boosters and antivirus software.

Brand credibility is particularly essential when offering services such as micro-insurance or mobile antivirus software. The GSMA reports that 70 per cent of respondents in Ghana would rather purchase insurance from an MNO than from an insurer. Such services are in high demand in emerging markets.

Mr Veremis adds: “Consumers are ready to trust their operators for services such as micro-insurance or mobile utilities, a position that places them ahead of the curve when it comes to broadening their portfolio of services and ultimately increasing their ARPU. Given the weakening performance of traditional voice services, revenues from digital services are critical for forward-thinking mobile operators.”

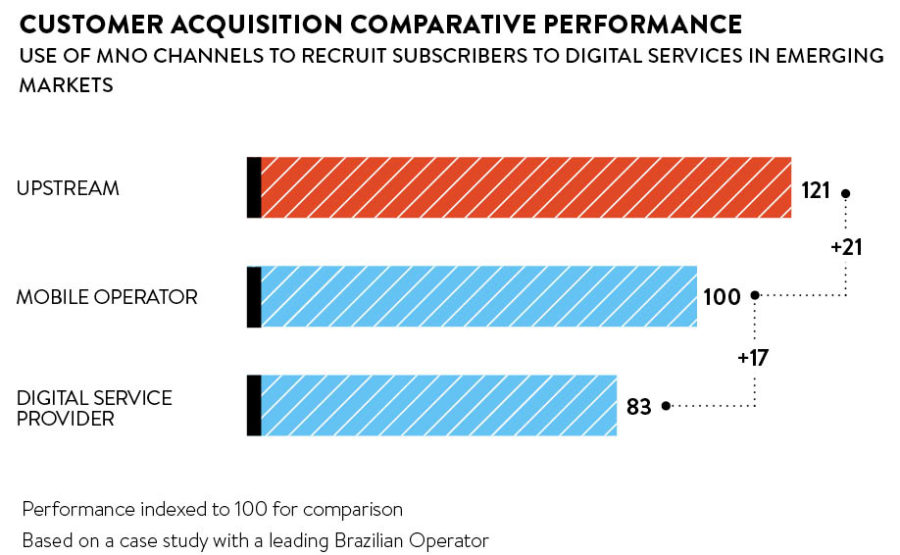

Consumer reach

Mobile operators enjoy unparalleled reach in emerging markets. Mobile device penetration in developing markets stands at 59 per cent, according to the GSMA. Moreover, operators typically own more than 20 marketing channels, such as SMS, USSD, SAT push, affording them a strong position when it comes to engaging customers. Owning the channels, however, does not mean they are necessarily utilised to their full potential.

Mr Veremis points out: “Every channel requires bespoke expert optimisation for each market and offering. Our experience shows that partnering with mobile marketing experts can improve the effectiveness of MNO channels in customer acquisition by more than 20 per cent.”

Operators also play a critical role with respect to providing internet access in developing markets. A recent Ericsson report found that in Nigeria mobile broadband infrastructure is used 70 per cent of the time when consumers access the internet, across any device.

The prevalence of mobile broadband in emerging markets opens up opportunities to use MNO infrastructure such as header enrichment for marketing purposes. This technology enables user authentication over an operator-provisioned mobile broadband connection. Working with digital marketing experts can help operators leverage their infrastructure to optimise customer acquisition flows.

Upstream experience shows that the steps consumers need to take to subscribe to a service can be reduced from nine to two, thereby reducing sign-up time by up to 80 per cent. Even better, customer acquisition costs can be reduced by up to 90 per cent when using an optimal digital flow with header enrichment.

Payment capabilities

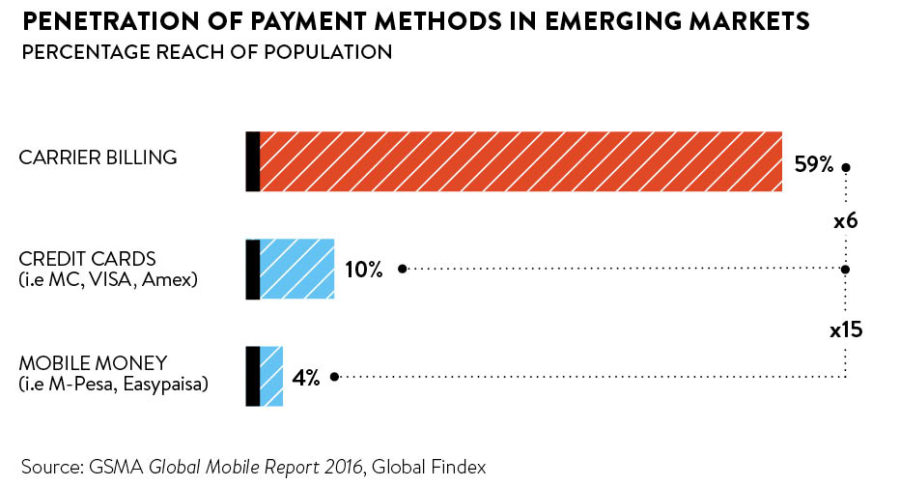

Some 87 per cent of consumers in emerging markets state they are willing to pay for high-value digital services via mobile devices, according to an m-commerce report commissioned by Upstream. With 80 per cent of people in emerging markets being unbanked, mobile operators are able to provide the ubiquitous solution for consumers paying for digital services.

It helps a great deal to partner with a company that has deep mobile-commerce expertise and can help maximise revenues in developing markets

“When it comes to payment cards, the combined reach of Visa, MasterCard and Amex is currently at 18 per cent of the population in Sub-Saharan Africa. While M-Pesa was a runaway success in Kenya, mobile money payment options only reach 11 per cent of mobile phone users in emerging markets. That said, the most trusted and preferred payment method is direct operator billing, with 45 per cent of consumers in these markets expressing a preference for this payment method. It is available to anyone who has a mobile phone and it utilises a consumer’s airtime balance as a reliable form of digital currency,” says Mr Veremis.

The majority of mobile consumers in emerging markets are on prepaid plans, with an average airtime balance of often less than $2. Hence, offering the right kind of billing plan to suit their top-up frequency habits and corresponding income is critical. The most appropriate way to monetise consumption of digital services is the subscriptions-based, micro-payment business model.

Responding to this, Mr Veremis puts forward his view: “A subscription model works well, but to really make it effective, the payments have to be small and occur more often, more commonly known as micro-payments. Working with a technology partner who really understands the needs of consumers in emerging markets, and who can provide the right platform and consumer data, typically can increase the percentage of successful charge rates by up to 50 per cent.”

Customer data

On top of all this, mobile network operators have access to a wealth of data from their customers, from spending patterns and habits to their browsing preferences and demographics. Mr Veremis says: “The right use of operator customer data can really help unlock improvements in payments, customer acquisition, and better targeting of digital services and offers.”

In conclusion, mobile network operators are exceptionally well placed to secure a significant share of the $70-billion digital opportunity in emerging markets. Trust in their brand is strong, they have unparalleled consumer reach and they hold the key to payment offerings for unbanked consumers. However, as Upstream’s Mr Veremis concludes: “These unique assets are not always leveraged to their full potential. It helps a great deal to partner with a company that has deep mobile-commerce expertise, and can assist in maximising revenues and place operators at the top of the digital pyramid in developing markets.”

For more information please visit www.upstreamsystems.com

Brand equity

Consumer reach