Talent shortages, legislative change, technological transformation and disruption caused by the pandemic are some of the challenges placing unprecedented pressure on corporate tax departments.

The world has suddenly become difficult for in-house tax specialists as an growing set of requirements crowd their agenda.

These developments are increasing the workload for the same tax and finance functions that are facing budget cuts and unparalleled skills shortages.

In response to these pressures, many businesses are co-sourcing select tax affairs to tech-enabled tax specialists. The mounting complexity of modern tax systems is leading corporate tax departments to pass at least some of the responsibility for routine work to outside providers. Whether it’s value-added tax (VAT) filings or corporate income tax, co-sourcing routine tax tasks is a way to improve efficiency and give senior staff the breathing space to help develop answers to some of the big strategic questions facing businesses.

“We have never seen a time like this in the tax profession,” says Kate Barton, EY global vice chair – tax. “All of these issues are converging: talent challenges, the need to address environmental, social and governance (ESG) issues, a desire to drive long term value, unrelenting legislative and regulatory change, and cost pressures.”

Stuart Lang, EY EMEIA tax and finance operate leader, says data and technology are key enablers to help tax departments cope. “You can either automate basic tax tasks internally or undergo a tax transformation by working with an outside provider that has made significant investments in cloud technology,” he says.

Doing nothing is not an option. You might get your ESG wrong, you might over-pay on your tax bill, face a big controversy issue, or you might not understand all the legislative and regulatory change that is coming. The stakes are high if you don’t transform

Dave Helmer, EY global tax and finance operate leader, agrees: “Doing nothing is not a valid option. You might get your ESG wrong, you might over-pay on your tax bill, face a big controversy issue, or you might not understand all of the legislative and regulatory change that is coming. The stakes are high if you don’t transform.”

Dealing strategically with these important issues is difficult because core responsibilities of tax and finance departments have also been made exponentially complicated by an increase in digital tax filing requirements from governments. An increasing number of jurisdictions are demanding tax information daily, weekly or monthly, with transactions provided directly to the government in digital filings. This has forced businesses to focus on their own data and technology for day-to-day tax management, even as they try to respond to increasing demands.

As a result, today’s tax professional is having to become multiskilled, with the ability to process large amounts of new tax technical information while also mastering the technology and data needed to enable efficient and accurate filings with governments. For the tax industry, that means developing a whole new type of renaissance tax professional, as much a data analyst and tech specialist as a tax and accounting expert.

Hampering this process of professional transformation are the talent shortages that have hit the economy during the pandemic. Many employees have decided to change jobs, leave the job market all together or retrain in new fields. At the same time, many older professionals are reaching retirement age, just as the shift to digital technology has created a shortage of tax specialists with the right skills and qualifications to carry out the significantly more complex range of tasks at hand.

Tax was already getting harder for businesses before the pandemic came along. Led by the G20 and the Organisation for Economic Co-operation and Development, 141 jurisdictions have worked together to develop and agree a set of recommendations for significant alterations to the global framework for taxing international business income. This initiative has two main elements. The first pillar involves revisions to the historical approaches for how taxing rights over cross-border business income are divided among countries. The second pillar involves the establishment of a new system of global minimum tax rules for business income. These transformational changes will add to the complexity of global tax management.

The pace, volume and complexity of legislative change is increasing the pressure on tax and finance functions just as revenue authorities seek to recover approximately US$33tn in worldwide Covid-19 support measures. Moreover, the pandemic has had serious ramifications for tax departments, with remote workers often disconnected from their data centres and in some cases creating tax obligations for their own employers by their mere presence in new jurisdictions.

Digital transformation that enables innovative services in finance, accounting and tax is helping organisations gain more relevant and actionable insights for their business, often at a lower cost

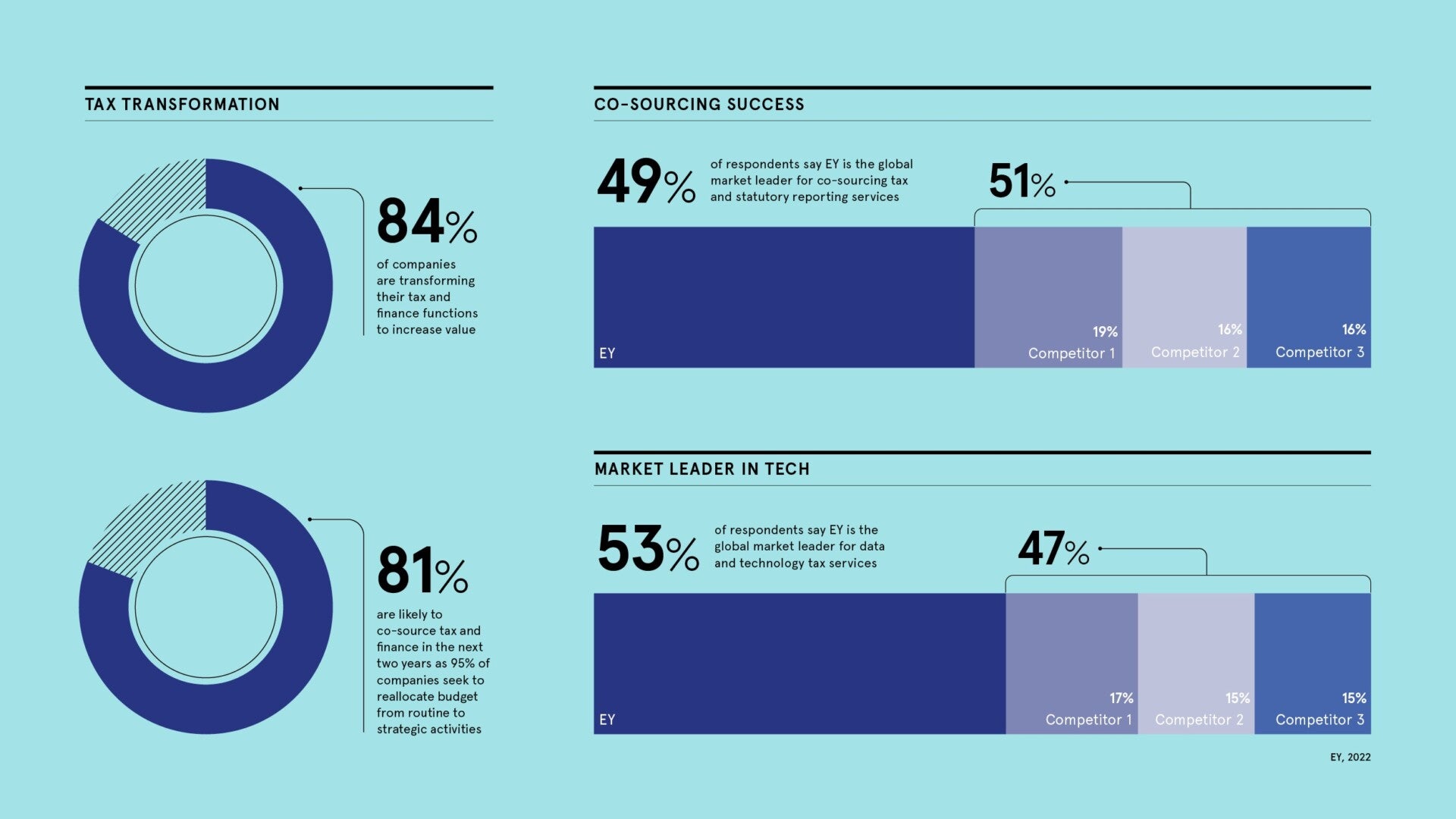

A survey carried out by EY and conducted by Euromoney Thought Leadership Consulting found that 84% of companies are transforming their tax and finance functions to get more value while 81% are more likely than not to co-source their activities in the next 24 months. The survey, released in January, questioned some 1,650 executives in more than a dozen industries, across 40 jurisdictions. It found that 87% of all companies surveyed plan to reduce the cost of the tax and finance function in the next two years. This demonstrates the dual pressures on tax departments, as they struggle to achieve more with tighter resources.

Many businesses have decided that the only way to cope with these pressures is to co-source some of their tax and finance activities to third-party providers. These are typically professional services organisations that have developed cloud-based solutions to managing routine tax operations.

Even data and technology companies including Microsoft and SAP SE have co-sourced tax activities with EY. Kirsten Birnbaum, head of global tax for SAP, says: “Working with a global network of specialists, jointly utilising our technologies has enabled us to considerably increase our efficiency in delivering tax compliance. We have more room to focus on strategic activities – and that’s a great benefit for the company.”

Asked about skills shortages, 95% of the survey respondents believe their tax and finance personnel need to augment their tax technical skills with data, process and technology skills in the next two years. Many are concluding it’s easier to work with outside providers who specialise in developing people with the right skills.

Meanwhile, three in four businesses say they are struggling to keep up with the pace of legislative and regulatory change and 83% expect to pay an average of US$11.1m to comply with emerging digital tax filing requirements over the next five years. An outside provider more likely has the right resources dedicated to help.

The area of ESG is especially challenging for companies, as historically few businesses have volunteered information on their tax affairs. But in the current environment where the general public and politicians are demanding greater transparency on corporate tax, businesses are getting ready to open up their books and reveal more.

Over half the companies in the survey said they were going to make voluntary disclosures about their tax governance frameworks (51%), and 45% on corporate income tax. Other areas they’ll be publishing include excise taxes, direct taxes paid by employees and employer-paid payroll tax. All the companies interviewed said they would disclose at least one of these while 70% said they would disclose at least three. This new environment of social awareness adds to the need for the co-sourcing of routine activities to free up time for strategic thinking.

In order to create value while addressing these changes and recruiting tax-tech talent means technology is needed to drive a range of solutions. It must have the ability to collect data from multiple sources; gather, clean and deliver it into systems that fit all uses; prepare reports that meet the demands of multiple jurisdictions and multiple government agencies; update processes and numbers for accurate compliance; and analyse options for smarter planning and to help mitigate risk. Each of those tasks requires the most advanced technology platforms and cloud-based storage possible. However, implementing and maintaining such systems can be costly and half of the largest companies in the survey agree that a lack of a sustainable plan for data and technology is the biggest barrier to achieving their tax and finance function’s vision.

“Digital transformation that enables innovative services in finance, accounting and tax is helping organisations gain more relevant and actionable insights for their business, often at a lower cost,” says Daniel Goff, Microsoft corporate vice-president, worldwide tax and customs. “But transformation looks different to different companies. Some want to build internal capabilities. Some prefer to co-source with a provider. Often, a hybrid approach is the best approach. Companies that undertake such transformations are better positioned to redirect resources to focus on the most strategic finance and tax issues.”

Where businesses may have been able to get by in the past, the convergence of so many acute challenges piled on top of one another means many corporate tax departments will only be able to survive through co-sourcing. They need to find a specialist that is up to speed with all the legislative changes globally, that can help plan and deliver controversy advice and deliver routine services at scale.

We have never seen a time like this in the tax profession. All of these issues are converging: talent challenges, the need to address environmental, social and governance issues, a desire to drive long term value, unrelenting legislative and regulatory change, and cost pressures

In working towards a successful co-sourcing process, the tax and finance departments should first analyse and re-evaluate the existing operating model to identify areas that could be improved. Next, the company should determine which activities to keep in-house. This helps with the next stage which is to decide exactly which activities should be co-sourced. Finally, the company should consider a hybrid approach in which some activities are retained and others are outsourced.

The best-planned hybrid approach can improve both effectiveness and efficiency while empowering staff to become value-added partners to the business with the focus firmly on activities that improve the bottom line. The result of this should be the creation of a team with a single mindset. However good the in-house team is, working with a co-sourcing provider allows the tax and finance function to go even deeper and further with its analysis.

Many benefits are open to businesses that adopt the co-sourcing model. Employing a specialist to take care of routine tax activities can improve processes and accuracy, helping companies to better manage a range of emerging challenges from ESG reporting to controversy issues. Shifting to this model will allow the tax and finance function to fulfil its role as a value-added business partner engaging in high-level strategic tax issues.

Co-sourcing tax and finance allows CFOs to show their corporate boards that they are getting to grips with three significant challenges facing every business today – creating value, managing risk and reducing cost. No wonder so many businesses large and small are looking for a piece of the action.

To find out more, visit www.ey.com/TFOsurvey

Promoted by EY

Talent shortages, legislative change, technological transformation and disruption caused by the pandemic are some of the challenges placing unprecedented pressure on corporate tax departments.

The world has suddenly become difficult for in-house tax specialists as an growing set of requirements crowd their agenda.

These developments are increasing the workload for the same tax and finance functions that are facing budget cuts and unparalleled skills shortages.