Five years after the first stage of auto-enrolment was launched for larger employers, defined contribution (DC) pension plans now dominate the UK market in terms of member numbers with asset levels running into hundreds of billions of pounds. The government and the Pensions Regulator have responded accordingly with legislation providing flexibility for members and numerous regulations to protect the consumer. As a result, DC plans have become considerably more complex to run and the risks in doing so have escalated.

Five years after the first stage of auto-enrolment was launched for larger employers, defined contribution (DC) pension plans now dominate the UK market in terms of member numbers with asset levels running into hundreds of billions of pounds. The government and the Pensions Regulator have responded accordingly with legislation providing flexibility for members and numerous regulations to protect the consumer. As a result, DC plans have become considerably more complex to run and the risks in doing so have escalated.

While flexibility and choice have been increased, many employees still have little detailed knowledge of their pension arrangements and what benefit they might expect to receive. Research from Aon, the leading global provider of risk, retirement and health solutions, reveals that a third of the population have no idea what retirement income they can expect to get and four in ten high earners underestimate how much they need to maintain their standard of living.

Perhaps this is why a growing number of trustees and business leaders are starting to look again at how they run their company DC pension funds. In particular, they’re asking whether their delivery, investment and communication strategies, many of which were established in some haste to hit government deadlines, are really meeting the needs of their members.

“Today there are billions of pounds in schemes that were set up relatively quickly at a time when clients didn’t have many members or assets. If employers have a scheme that has been around for more than three or four years, they really need to take a step back and review it,” says Tony Pugh, Europe, Middle East and Africa DC solutions leader at Aon. “Given how much the market has changed in the last few years, there is likely to be a better solution available to them and their employees.”

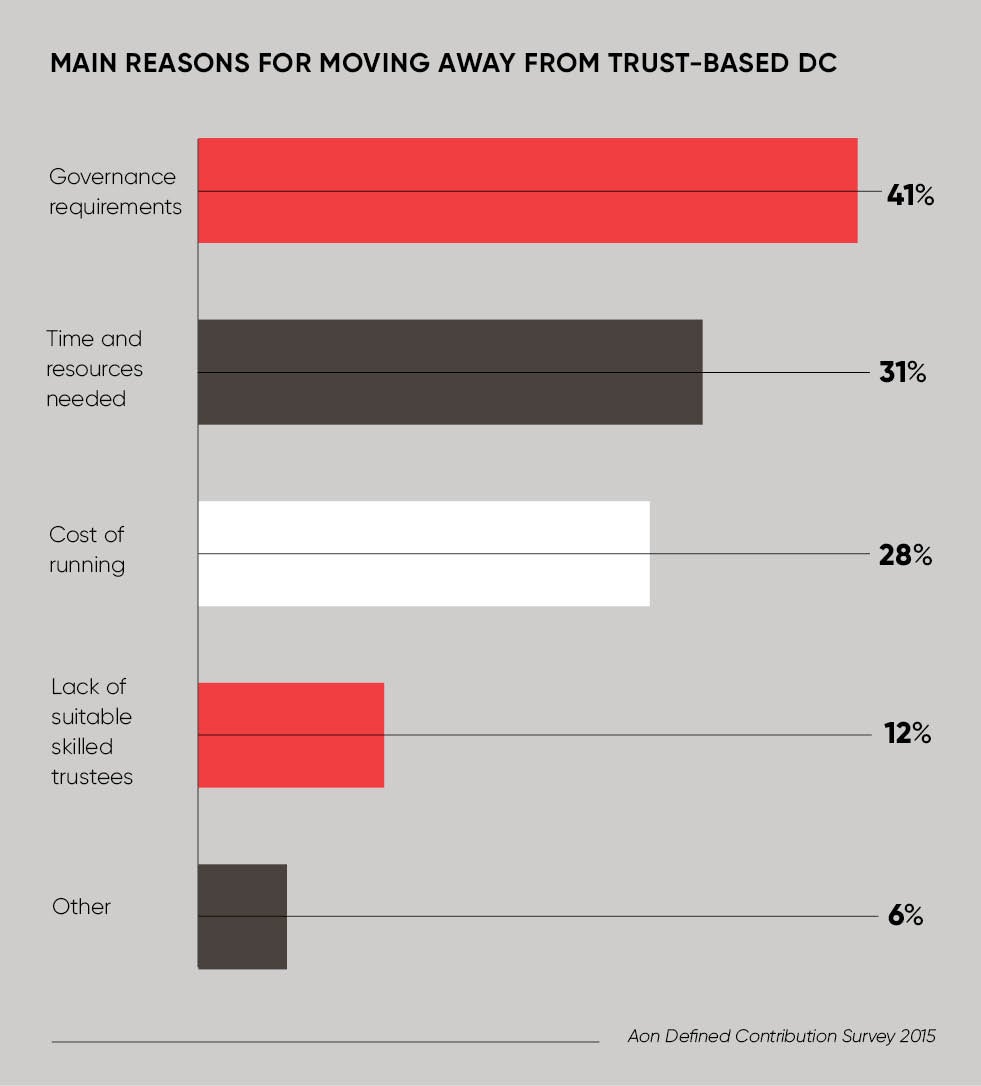

Pension funds and their trustees need to think about how they can become more efficient, according to Mr Pugh. They must ensure they’re not wasting time, money and effort on tasks that have a low priority or could be carried out more efficiently by delegating them to a pension provider. They also need to ask themselves whether every penny is being well spent as they manage issues such as increased regulation.

To ensure they’re doing the best for their members, more and more companies are now taking advantage of a new generation of master trusts and group personal pension solutions to cut administration costs. These delegated solutions combine the best thinking and are delivered in a streamlined, efficient way that allows pension fund members to gain access to the best investments and services at aggregated, scalable prices.

Delegated trust and contract-based solutions allow the employer or trustee to feel much more comfortable that their members are benefiting from the right investment decisions

“For example, a company employing a few thousand people will find that running a standalone trust-based DC plan might cost them around £300,000 to £400,000-plus a year,” says Mr Pugh. “If the average member may, at best, glance at their benefit statement once during the year, is that spend delivering value for money for the members or the company? They could move to a delegated proposition such as a master trust and bundle it all together to save on costs. The employer can then put the money they’ve saved into other areas, for example higher contributions or a wider financial wellbeing programme.”

Companies that choose a group personal pension plan now have, for the first time, access to the same type of cost-efficient delegated investments that will really deal with most DC pension scheme members’ concerns – “I am not an investment expert, so can’t someone do this for me?”

The last five years has seen the range of delegated trust and contract-based solutions grow significantly. These allow the employer or trustee to feel much more comfortable that their members are benefiting from the right investment decisions.

Delegated solution providers will constantly monitor the market and, where they identify what they believe to be a better investment, will automatically choose and implement it on behalf of the scheme.

We’re now seeing a new generation of master trusts that have been developed to serve larger-scale clients used to the highest quality of services. “Even organisations with supersized schemes of £500 million-plus have realised that their trustees were only meeting a few times a year and so it’s made sense for them to put their funds into a delegated solution where professionals can look after these funds day in, day out,” says Debbie Falvey, DC proposition leader at Aon.

The other advantage of these new generation solutions, which many trustees and corporates are now discovering, is that their scalability allows significant investment in new technology such as robo-advice and easy-to-access at-retirement solutions. Market-leading solutions can give members access to financial aggregation tools that enable them to see all their financial affairs in one place, including their debts and other savings products such as ISAs, alongside their pension. They are able to deliver intelligent communication “nudges”, prompting members into activity at a time when action would be appropriate for them.

Delegation can enhance the employee experience and provide a host of otherwise unobtainable opportunities. “There are so many new opportunities to make DC pensions more financially efficient and engaging – the time is right to take a fresh look at them,” Ms Falvey concludes.

To find out more about Aon’s DC Solutions please call 0344 573 0033 or visit aon.com/pensions