Speakers

Karl MacGregor (KM) CEO and co-founder, Vyne

Adam Calladine (AC) Head of products, Kinetic

Benjamin Canova (BC) Global payment manager, worldwide omnichannel luxury retailer

Andy Sale (AS) Head of partnerships and alliances, CellPoint Digital

Russell Curzon (RC) Vice-president and head of sales, UK and Europe, Nium

How has the payments landscape evolved in recent years?

RC It has undergone tremendous transformation, with digital payments becoming the new normal. The pandemic has accelerated digital adoption further, with consumers becoming used to the benefits and convenience brought about by digital payments. The key barrier facing merchants is that global payments have been complex and disconnected, making it harder and more expensive to manage online payments. Various intermediaries are needed to process international transfers across currencies, and changing regulations mean rising card acceptance fees are also absorbed by merchants.

KM User experience and the desire to convert more online store browsers into paying ongoing customers is driving a lot of innovation in alternative payment methods. Consumers have incredible experiences on their mobile phones when consuming digital content and now expect the same when it comes to purchasing goods and services, which is increasing focus on the payment event and how that can be made super slick as well. Along with huge online growth during the pandemic, we also saw consumers adopt the use of QR codes when shopping, something already popular in markets like China and Japan.

What role is regulation playing and how is this impacting the ecommerce sector?

KM Regulation is a significant driver of change and has been a huge area of both pain and opportunity over the last five years, particularly with respect to PSD2. For ecommerce businesses, PSD2 is a massive pain point because it’s introducing things like two-factor authentication and secure customer authentication for credit card transactions, which breaks the user experience. For us, it has provided an opportunity to create a faster, simpler and fairer payment method that solves some of the inefficiencies that exist around credit and debit cards, which you could argue are a bad fit for consumer expectations today.

For merchants, there’s no chargeback risk, the costs are much lower and they only have to deal with one party

AC In the higher education sector, within student accommodation PSD2 is a problem. We see infrequent payment schedules – three instalments a year, rather than monthly rent – and PSD2 introduces a lot more challenges for recurring card payments of this type. Direct debits are also very admin heavy. We’ve already seen with our Irish customers, since PSD2 came into force there in January, a much higher decline rate on those recurring transactions because there is not a recognisable pattern on the payment. Payment is a huge drop-off point in the booking process anyway, particularly in the student accommodation sector because it’s usually mum and dad paying. Our customers are knocking on our door saying we need to do something.

How is open banking helping to remove the middlemen in payments, enabling a more direct experience?

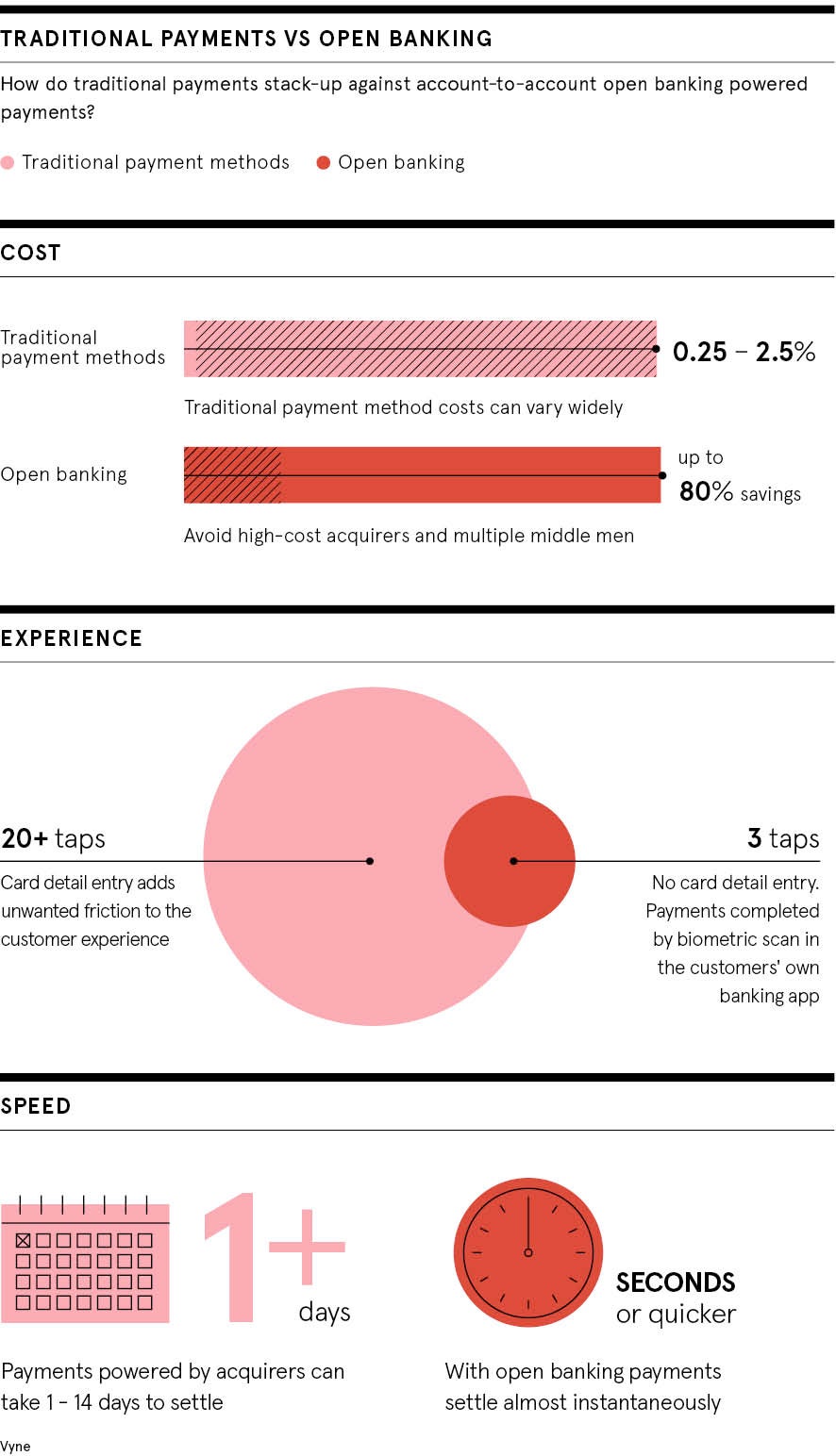

KM Open banking gives us the tools to build a solution that simplifies the flow and reduces a lot of the risk. It gives us the ability to create a push payment. A consumer buying something from a website or in a store can go to their bank account in one click or scan of a QR code and push the money directly to the merchant. That moves everybody out of the middle, supported by a technology solution like Vyne which wraps it up with all the features and functionality that a business needs to make it viable. Consumers get greater transparency and reduced risk because a bad actor can’t steal their card details. For merchants, there’s no chargeback risk, the costs are much lower and they only have to deal with one party.

AS They also get paid right away, which is particularly important for sectors like travel where the risk that’s built into card payments means businesses are sometimes having to wait weeks or even months to get their money. There are some horror stories during the pandemic of very reputable travel businesses that have been either switched off altogether by their card acquirers because they don’t fit a new revised risk profile or have had very stringent terms and conditions forced onto them, including holding onto all money until a flight has flown. It has a dramatic effect on their cash flow.

BC With instant payments, no personal data is handled, so that’s another risk eliminated. It’s also cheaper, there is no friction for the customer and we have the funds immediately. It makes a lot of sense. In the past year, Apple Pay has increased, PayPal has exploded and the instalment payment enablers are getting stronger and stronger. We started using new alternative payment methods in specific countries and, within two days, 20% of all of our business within these countries was going through it. There are benefits across the full chain so it’s very easy to get validation here.

Does instant payments, powered by open banking, signal the end of credit cards?

AS I don’t think cards will be replaced entirely but the move towards non-card-based payment methods is inexorable. One size does not fit all payments. Whether that’s a type of payment or an individual payment provider, the days of supporting a global business with just one provider and just supporting cards are well and truly gone. You need to have the flexibility to contract with who you want, get paid where you want to get paid in whatever currency you want, and support the payment methods that your customers really want.

AC Cards were invented before the internet and it’s important to remember they have been adapted to use online. I don’t think they’re the best solution for online payments anymore. The customers we speak to want to offer a much wider choice of payment. It’s not just fraud that stops card payments, it’s the number of people in the mix. You’re going through the gateway, the acquirers, the issuing bank, and then you’ve got the 3D Secure element in an iFrame in the middle. I spend a long time on the phone, on behalf of customers, trying to work out where it broke down and I get sent round in circles from the bank to the acquirer to the 3D secure provider. In the end the answer is always to just tell them to try again, which I don’t think is acceptable in this day and age.

BC We don’t need the customer to type in their credit card credentials. We don’t need the customer to have to go to their smartphone to enter a code or anything. We don’t need authentication drop-offs. We don’t need a lot of dropouts due to fraud checks or due to issuer declines. We don’t want to have chargebacks either, we just want a direct relationship with a customer, handling any incidents directly, and if we can have nobody in the middle then that’s a bonus for everyone.

For more information please visit payvyne.com

Promoted by Vyne

Speakers

Karl MacGregor (KM) CEO and co-founder, Vyne

Adam Calladine (AC) Head of products, Kinetic

Benjamin Canova (BC) Global payment manager, worldwide omnichannel luxury retailer

Andy Sale (AS) Head of partnerships and alliances, CellPoint Digital

Russell Curzon (RC) Vice-president and head of sales, UK and Europe, Nium

How has the payments landscape evolved in recent years?