Thanks to advances in tech and bold new industry players, now is the time to reassess how you think about mortgages. In the last few years alone, there’s been a quiet yet significant shift in the international and domestic mortgage markets.

Since launching in 2015, fully online US lender Rocket Mortgages has grown rapidly, propelling parent company Quicken Loans to America’s number-one spot. Down Under, award-winning fintech Tic-Toc mortgages has reduced the start-to-finish mortgage application process to just 22 minutes.

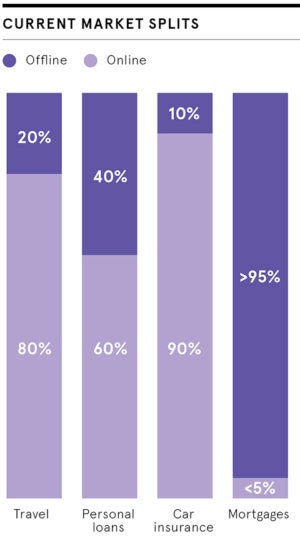

There’s indisputable evidence worldwide that the consumer market is hungry for change, even when it means stepping away from traditional lending. And here in the UK, we’re on the cusp of our very own digital mortgage revolution.

There’s indisputable evidence worldwide that the consumer market is hungry for change, even when it means stepping away from traditional lending

Developments in proptech, big data and the keen adoption of Open Banking in the UK have created fertile ground for the growth of new full-service, fully digital, straight-to-consumer lenders.

Where traditional lenders have adopted some digital elements into their offerings, most are restricted by red tape and ingrained processes. In contrast, new fintech players are able to design and mould their models as fully digital, user-friendly propositions from the off.

Bypassing obsolete practices and paper-based processes, these new models provide tech-savvy, time-poor customers with a simple, secure, transparent user journey, near-instantaneous decisioning and low rates.

Behind the scenes, data science and the emergence of big data has enabled reliable, fast assessment of borrowers. Access to credit bureau data, Open Banking and advances in biometric borrower identification, driven by application programming interfaces, or APIs, are revolutionising the execution of affordability and credit assessment.

Property valuation, conveyancing and legal models are also being disrupted for the better by tech. The Land Registry now accepts digital signatures on mortgage deeds and the Financial Conduct Authority is actively supporting the development and adoption of tech to make systems more accurate, efficient and consistent.

Property valuation, conveyancing and legal models are also being disrupted for the better by tech. The Land Registry now accepts digital signatures on mortgage deeds and the Financial Conduct Authority is actively supporting the development and adoption of tech to make systems more accurate, efficient and consistent.

The time of lengthy, manual processing is making way for real-time data validation and instant decisioning. No physical meetings necessary.

With many forces at work, it’s hard to predict exactly how the mortgage space will develop. However, it’s almost certain that intelligent automation of the value chain and fully digital lending will see a sharp uptake in an industry and consumer marketplace demanding change.

Greater transparency across the board with lower costs for both customer and lender will undoubtedly create a healthier and happier mortgage lending environment. Customers will have greater clarity, experience less stress and be able to act quickly to secure their desired property.

At Molo we’re proud to be leading the charge as the UK’s first fully digital mortgage lender, leveraging a proprietary tech platform to deliver fully online, paperless decisioning, with our 15-minute mortgage and residential offering on the near-horizon. Most exciting of all, this is only the very beginning.

Welcome to the digital mortgage revolution.

Get a decision in principle in minutes at molofinance.com