The vast majority of people work hard for most of their adult lives in the hope of building up sufficient income for themselves and their families. Yet many, including some of the very wealthiest in society, are failing to ensure the proceeds of that work are passed on effectively to the next generation.

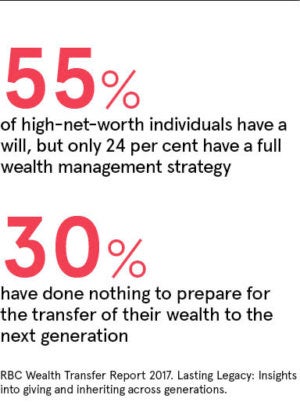

In the UK, some 55 per cent of high-net-worth individuals have a will, according to research by RBC Wealth Management, but only 24 per cent have a full wealth management strategy in place. Worryingly, 30 per cent admit to having done nothing to prepare for the transfer of their wealth to the next generation.

Given the sums of money involved, which could extend into millions in some cases, this is extremely concerning, says Alan Binnington, a director of the Fiduciary Specialist Team at RBC Wealth Management. “It’s surprising that people who are in that high-net-worth category and have access to advisers haven’t got around to dealing with one of the most important issues that families face,” he says.

There are a number of reasons why this may be the case. There can be misconceptions over the amount of wealth required to justify such planning, says Mr Binnington. “You don’t need to be fabulously wealthy to have a justification for putting a plan in place that will help with that transfer,” he says.

There can also be a reluctance in families to discuss inheritance with younger generations. “I’ve found in some instances that older members of the family are reticent to talk about their own death,” says Julie Kleis, fellow director of the RBC Wealth Management Fiduciary Specialist Team. “There may be other family members who are much more willing to talk about it, but find it hard to start the conversation.” Advisers can help to bring the matter up, she adds, but ultimately families have to be prepared to confront the situation, and have an open and honest dialogue.

As people become more mobile and go abroad for personal or professional reasons, or have family members based in other countries, the wealth management process can become more tricky, as different countries will have different legal and tax systems.

Equally, another complicating factor is “blended” families. “Where there are children from previous relationships, people are keen to make sure all family members are treated equally and that can be quite difficult to manage,” says Ms Kleis. Often such families tend to be less prepared, despite having the greatest need for planning, she adds.

None of these issues are insurmountable, but do underline the need for effective planning. The most obvious solution for some families would be a discretionary trust, says Mr Binnington, where assets are placed into the hands of the trustees who manage them on behalf of the beneficiaries. “The major benefit of this is that it avoids all the problems you get in obtaining probate on the death of the wealth creator,” he says. “Trusts have always been seen as a very useful vehicle because the trust doesn’t die.”

In the case of business owners, often much of the wealth is tied up in a family business, which can also require specific solutions. One option is to set up a family charter, which can identify the family’s philosophy and attempt to create a system that is fair for all members of the family. “Some members of the family may want to work in the family business; others may have no interest or may not have the necessary ability,” says Mr Binnington. Here, different classes of shares can be awarded to different family members, separating ownership from control and enabling those who work in the business to benefit from bonuses in addition to dividends.

Other measures can also be put in place, says Ms Kleis, including allocating some family members an amount of money to start up their own business or even to help them pursue philanthropic aims through charitable initiatives. “That’s something that often appeals to millennials, who don’t tend to measure success in terms of financial wealth, but the contribution to the wider community,” she says. “That shift from one generation to another means we need to come up with structures that satisfy those objectives.”

Preparing to transfer wealth is an emotionally fraught subject, but people need to start thinking about what they would want to happen and then take appropriate advice

Basing arrangements through a provider in an international financial centre can help smooth some of the potential difficulties, says Mr Binnington. “They tend to be stable jurisdictions and are experienced in dealing with complicated family wealth planning,” he says. “They are also well located in terms of access to international markets, which is how they developed in the first place.”

Inevitably, everyone’s situation is different, but the important message is that this is not something that can be ignored. “Preparing to transfer wealth is an emotionally fraught subject but people need to start thinking about what they would want to happen and then take appropriate advice,” says Kleis. “As someone prepares to put a wealth transfer plan in place, they can take solace in that there are lots of people who can help them. But ultimately they are the ones who have to make the decisions so they have to start the conversation with their families or beneficiaries. While it may be off-putting, preparing to transfer wealth needs to be a very important part of people’s lives, perhaps equally as important as earning it.”

To talk to us please contact:

Julie Kleis on +44(0)1534 501809 or [email protected] or

Alan Binnington on +44(0)1534 602401 or [email protected]

*Calls may be recorded.

RBC Trust Company (International) Limited is regulated by the Jersey Financial Services Commission in the conduct of trust company business. The Private Client Fiduciary Services terms and conditions are updated from time to time, and can be found at www.rbcwealthmanagement.com/global/en/terms-and-conditions. Registered Office: Gaspé House, 66-72 Esplanade, St Helier, Jersey JE2 3QT, Channel Islands; registered company number 57903.

®/™ Trademarks of Royal Bank of Canada; used under licence.