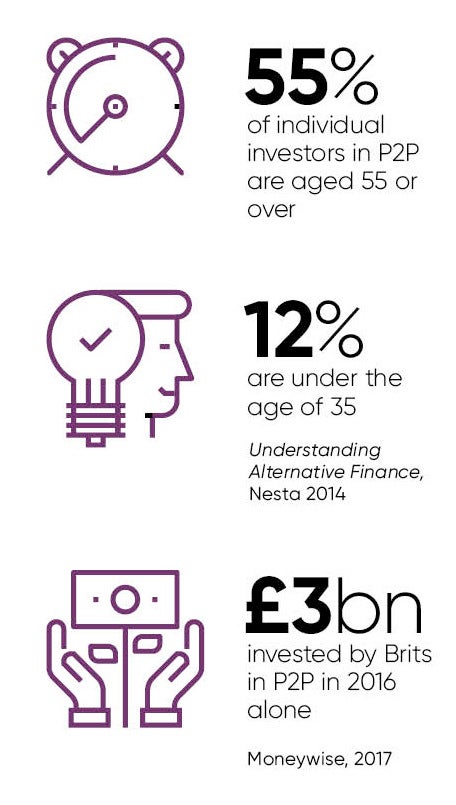

While it’s fair to say the sector still represents a drop in the ocean of the broader UK investment landscape, the amount lent through P2P platforms has grown dramatically since the turn of the decade, with Brits investing £3 billion in 2016 alone, according to Moneywise.

While it’s fair to say the sector still represents a drop in the ocean of the broader UK investment landscape, the amount lent through P2P platforms has grown dramatically since the turn of the decade, with Brits investing £3 billion in 2016 alone, according to Moneywise.

This new generation of investment products pride themselves on simplicity, speed and ease of use. But tempting though it is to assume that P2P is a craze for tech-savvy millennials, it seems the opposite is true. Research conducted by Nesta in their 2014 Understanding Alternative Finance report revealed that more than 55 per cent of individual investors in P2P are aged 55 or over, with only 12 per cent under 35.

And now that investors can include eligible P2P investments within their ISA, the sector’s mainstream popularity might well grow still further. P2P looks to be growing up.

Even financial advisers, a justifiably cautious audience, seem to be coming around to the idea of P2P as a useful diversifier away from the volatile stock market, perhaps buoyed by the entrance of more established players into the sector.

Take Octopus Investments. A 17-year-old investment company, last year it began distributing a P2P product, Octopus Choice, designed for both retail investors and financial advisers. It has already seen more than £75 million invested on behalf of over 4,000 investors, among them 500 financial advisers and their clients.

Of course, it’s important investors and advisers research the options before deciding if P2P is right for them. P2P lending is clearly not for everyone. Investing in loans places your capital at risk, investments aren’t protected by the Financial Services Compensation Scheme and instant access to your money can’t be guaranteed.

What’s more, the sector is as diverse as it is fast growing and each product will carry a different level of risk.

Take property lending, for example. Though there’s still a risk you could get back less than you put in, investing in loans that are backed up by a security like property arguably carries less risk than lending to individuals on an unsecured basis.

That’s because, if the borrower fails to repay, the property can be sold and used to fund some or all of the debt, though this could mean it takes some time to get your money back.

This sort of property-backed lending constitutes one of the oldest asset classes around. And for those investors looking to avoid the ups and downs of the stock market, it could provide an answer.

In the case of Octopus Choice, all loans are secured against property at conservative loan-to-value ratios of at most, 76 per cent, so the value of the asset would have to fall significantly before an investor would lose any of their capital. What’s more, Octopus even invests 5 per cent of its own money in every loan, which is at risk ahead of investors’.

P2P is not without its unique risks. But in today’s environment of low interest rates, rising inflation and ever-present stock market volatility, property-backed P2P in particular could play a useful role in the investor’s portfolio.

To see if you could benefit from property-backed P2P lending please visit www.octopuschoice.com

We do not offer investment or tax advice. We recommend investors seek professional advice before deciding to invest. This financial promotion has been commissioned by Octopus Choice, a trading name of Octopus Co-Lend Limited, which is authorised and regulated by the Financial Conduct Authority (No 722801). Issued by Octopus Investments, which is authorised and regulated by the Financial Conduct Authority (No 03942880).