The power and popularity of wearable technology as a generator of health data and the developing potential of genomics are well-discussed issues in the insurance industry. The sharing economy and shifting social factors also mean people visualise risk in new ways.

Insurers want to offer security in ways that appeal to these emerging customer demands. But they are faced with myriad potential practical steps they could take.

The idea of having individuals generate useful health and activity-related data, through wearable technology, is already established in insurance. However, the scale at which highly personalised data is being generated by consumers, whether deliberately or unwittingly, has been growing at a remarkable pace.

Deciding how best to handle issues around data privacy is among the industry’s key questions. Some people will not wish their personalised data to be put in the hands of insurers making decisions about policies, while others will want their data to be used to drive down insurance costs.

To understand how the insurance industry, “insurtech” startups, innovation labs and accelerators view these challenges, we spoke to some 75 thought leaders from around the world in a project we called the Incredibly Curious Adventure.

The results of the research are fascinating. Many of those interviewed saw a real opportunity for the insurance industry to evolve from life protection to life enrichment, firstly through more consumer-centric product design, and secondly through the dynamic use of predictive data that wearables, supercomputing power and artificial intelligence make possible.

However, legacy systems present a real challenge to insurers in the adoption and integration of these new technologies. Many insurers underestimate the readiness of the market to embrace the new opportunities and even to take advice from machines.

Another essential issue for the insurance industry is genomics, particularly with regard to its relevance in creating life insurance policies. In spite of early discussions on the subject, in the last couple of years it has been parked mainly out of view and the insurance industry has voluntarily agreed not to use much of the data that is available.

People are increasingly engaged with the details of how best to manage their health with the help of the digital data they create

But our collective understanding of genomics and its potential relevance to risk assessments has been expanded very significantly in recent years, and it offers the opportunity to do things better with individuals’ consent. Personal genomic information is increasingly being taken into consideration by doctors as they prescribe medications and by the pharmaceutical companies who create those products.

For individuals, the deepening of the information about their own bodies, which they can now access and refer to, is radically different from what it once was. People are increasingly engaged with the details of how best to manage their health with the help of the digital data they create. There is no doubt that a time is coming when consumers will wish to see this information made relevant to their insurance.

Given these changes, there must be genomic-themed conversations across a full spectrum of stakeholders around what kind of information should be made accessible to and deemed relevant for insurers.

The rich intelligence on everyday health knowledge gained from consumer genomic tests and much wider use of genomics in medicine could mean people are much better equipped to make personal decisions about their insurability than insurers can. While recognising the ethical responsibility of getting it right, this potential asymmetry of information is especially relevant in a voluntary insurance setting.

There are certainly moral questions that need to be asked before insurers are given a full regulatory go-ahead in this context. But it is clear there are significant potential benefits for consumers who open up access to data on their lifestyles, activity patterns, medical history and their genetic make-up. Importantly, insurers would be able to offer much more personalised insurance policies.

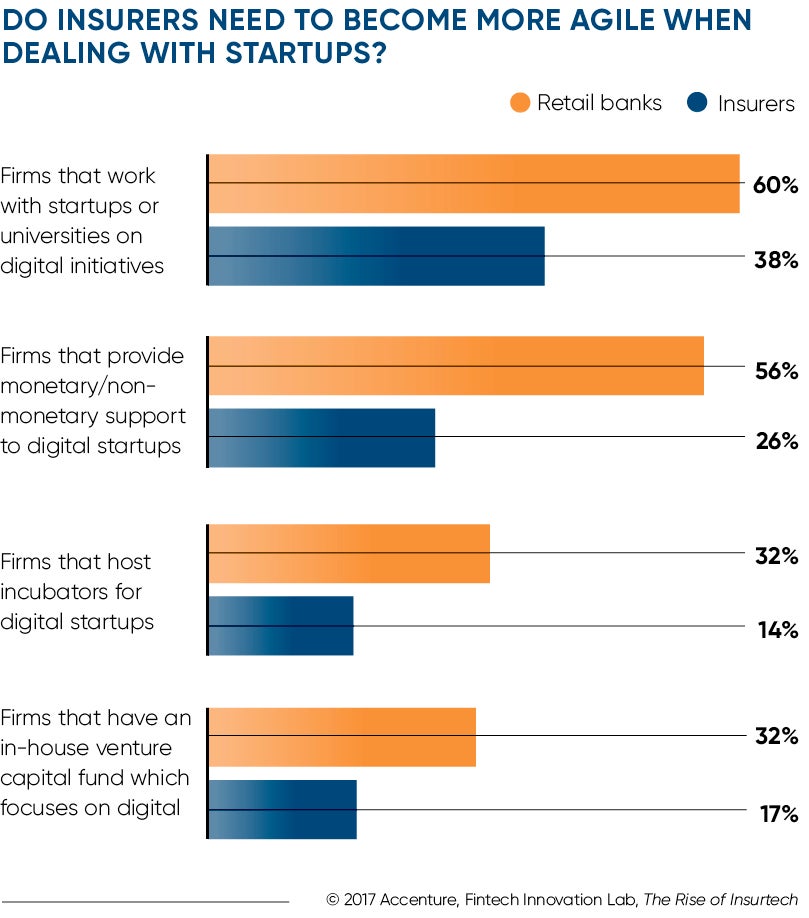

Making the most of data and genomics poses a serious technological challenge. To stay ahead of the competition, insurers must look towards startups to provide support and technical expertise.

Some insurers are in a position to acquire and absorb startups. Many others are not. The chief executives we interviewed said it is collaboration with startups that offers the potential to add value through insight and connection.

At Gen Re, our focus is now on nurturing relationships with startups whose innovations have real potential. We partner with those whose ideas can help insurers be more responsive to the changing dynamics within their industry, whether that is in relation to data analytics, mobile health, artificial intelligence or wearable technology.

Large-scale insurance companies are typically enthusiastic to adapt to change, but are operationally less agile. Insurtech startup companies are helping to change fundamentally the insurance industry and enabling it to meet emerging demand among consumers for greater personalisation.

It is our view that insurers must embrace the changes happening and be part of the conversations going on around these fundamental issues. Now, more than ever, the future is wide open. Our aim as a reinsurer is to be part of that global discussion about what the insurance industry can be and what it should offer.

To find out how to harness the huge changes relating to data and digital technology, and to work with smart startups, visit www.genre.com/futureofinsurance