We now expect technology to solve problems we never knew we had. But when it comes to our money, technology advances have been slower. That is until now. Whether it’s new ways to verify our identities, sophisticated banking apps, permission to share bank account data or faster payment solutions for people and businesses, technology is transforming how we pay and get paid. And it is helping us to better manage our finances while addressing one of the biggest risks we all face: security.

Sci-fi-style security is here

The combination of behavioural analytics and passive and physical biometrics reduces the reliance on passwords and security questions for user verification, which are both knowledge-based security tools no longer reliable in a world with nearly 20 billion records since 2013.

However, new solutions using behavioural and passive biometrics security could transform payments. We are already aware of physical biometrics; authenticating mobile payments with a fingerprint or our face is now commonplace in the UK. Combine that with behavioural analytics and passive biometrics and you have a potent combination where the trade-off between security and convenience no longer exists.

Passive biometric authentication relies on the way we use our phones, computers or tablets, which differs from person to person. Engines collect hundreds of datapoints on each user to build a picture of their unique biometric identity. For example, how fast do they swipe and type on the screen or keyboard?

The range of information expands with the behavioural analytics layer, which leverages the data from the passive biometric technology and collects insights, such as locations, how the device is connected to the internet, historic payment patterns or device and browser type. The vast data creates an accurate score for each user in real time. If an attempt to make a transaction is flagged as high risk, the financial service provider can automate rules to respond and transactions can be blocked, further verified with a physical biometric request or put forward for further investigation.

The success of open banking will rely on establishing trusted relationships, a brand promise, technology, processes, and security working seamlessly and in harmony

This approach takes security beyond user names, passwords, or other security measures bad actors are proficient at bypassing. This security doesn’t only apply at login or checkout as the user behaviour can be monitored across the customer journey, at moments such as creating an account or applying for credit, checking the balance on a gift card or asking for a password reset. This approach to user verification helps companies remove friction for their trusted users while weeding out fraudulent traffic.

Paul Stoddart, president of New Payment Platforms at Mastercard, says: “The impact of being able to analyse behavioural data is phenomenal. NuData Security¹ helped a Fortune 200 web retailer defend against a persistent attacker, with its cutting-edge behavioural analytics service. It tracked 77 million logins over 90 days, with 39.3 per cent detected as high-risk and blocked, and 100 per cent accuracy. The attackers modified their attack pattern and within an hour NuData had updated its modules to rebuff the new method.”

Innovation in emerging markets

Too many people are excluded from the financial system, lacking bank accounts or access to basic financial tools. This is true for all economies, but especially for emerging ones. It’s in these markets where we are seeing the greatest innovations in payments.

Take Thailand, where digital payments are challenging the dominance of cash. Despite a relatively high proportion of the population having a bank account, millions lacked access to banking and financial services, and almost half of all Thais paid in cash for internet purchases.

The government and central bank of Thailand approached Vocalink² to help them modernise its national payments system, to reduce fraud and risk in the system, reduce the use of cash and increase financial inclusion.

The result was PromptPay, a real-time payment platform that allows people and businesses to make and receive payments instantly into their bank accounts or digital wallets linked to their national ID, corporate ID or mobile phone number. This underlying infrastructure allows Thai people to make purchases in-store or online, pay bills and donate to charities, and send and receive money to other people securely from their digital banking app.

“PromptPay has made a significant mark on the country’s bid to address financial inclusion and support the expansion of Thailand’s burgeoning digital economy,” says Mastercard’s Stoddart. “Since launch, PromptPay has attracted 49 million subscriptions in a population of 69 million and processes an average of 4.5 million transactions a day.”

The Thai government is also using PromptPay to make tax rebates and social welfare payments. The Bank of Thailand credits PromptPay among the initiatives that have resulted in the 83 per cent rise in digital payments since 2016. The Thai economy has been transformed.

Additionally, 164 million³ migrant workers globally rely on traditional money remittance methods where payments can take five days to clear and often lack transparency. In the Gulf Co-operation Council region alone there are 35 million migrant workers, primarily from India, Bangladesh and the Philippines⁴. Transfast⁵, a company recently acquired by Mastercard, enables people to make cross-border payments to family or friends in more than 50 currencies nearly anywhere in the world. It’s fast, secure and transparent, and offers a variety of pay-out methods, including into a bank account, digital wallet or cash.

Power of open banking

The UK has seen the birth of hundreds of creative fintechs thanks to its mandated open banking initiative. Open banking enables people and businesses to share access to their bank account data with other providers securely to access a range of new financial services. It has the power to revolutionise how we interact with our money by providing a wealth of services such as better budgeting, savings innovations, access to fairer credit and techniques to improve our overall financial wellbeing.

For example, when a person uses Venmo, a digital wallet that lets them make and share payments with friends, it’s open banking that allows Venmo to initiate those payments from the person’s bank account. Or when they use Emma, a budgeting and personal finance app, it’s open banking that allows Emma to aggregate recent transactions and balances from the person’s bank and/or investment accounts. The same technology also enables traditional banks to innovate their financial services; many already provide customers with a view of their finances across accounts at different providers.

As expected with any new initiative as large as this, there are challenges that lie behind the scenes. Overcoming them is critical to growing trust in open banking among people and businesses. They might never know their favourite financial services apps are enabled by open banking initiatives, but they expect the experience of using them to be safe and reliable, and expect any issues to be resolved quickly and effectively nonetheless.

Mastercard Open Banking Solutions™ support the banks, financial institutions and third party providers by connecting, protecting and resolving issues among ecosystem participants. Open Banking Connect provides a single, universal connection to financial institutions’ open banking functionality regardless of their application programming interface (API) standard or implementation. Open Banking Protect provides financial institutions with verification of third parties, fraud monitoring and alerts, while Open Banking Resolve provides a clear framework for resolving disputes, which is fundamental to securing people’s and businesses’ trust.

“The success of open banking will rely on establishing trusted relationships, a brand promise, technology, processes, and security working seamlessly and in harmony,” says Stoddart. “That’s why it’s key to address fundamental challenges such as fragmentation in API standardisation, fraud risk and dispute resolution.

We believe that by addressing these challenges, as we’re doing with Mastercard Open Banking Solutions, we can support the development of an open banking ecosystem that will revolutionise how millions manage their financial futures both locally and globally.”

New payment methods can transform small businesses

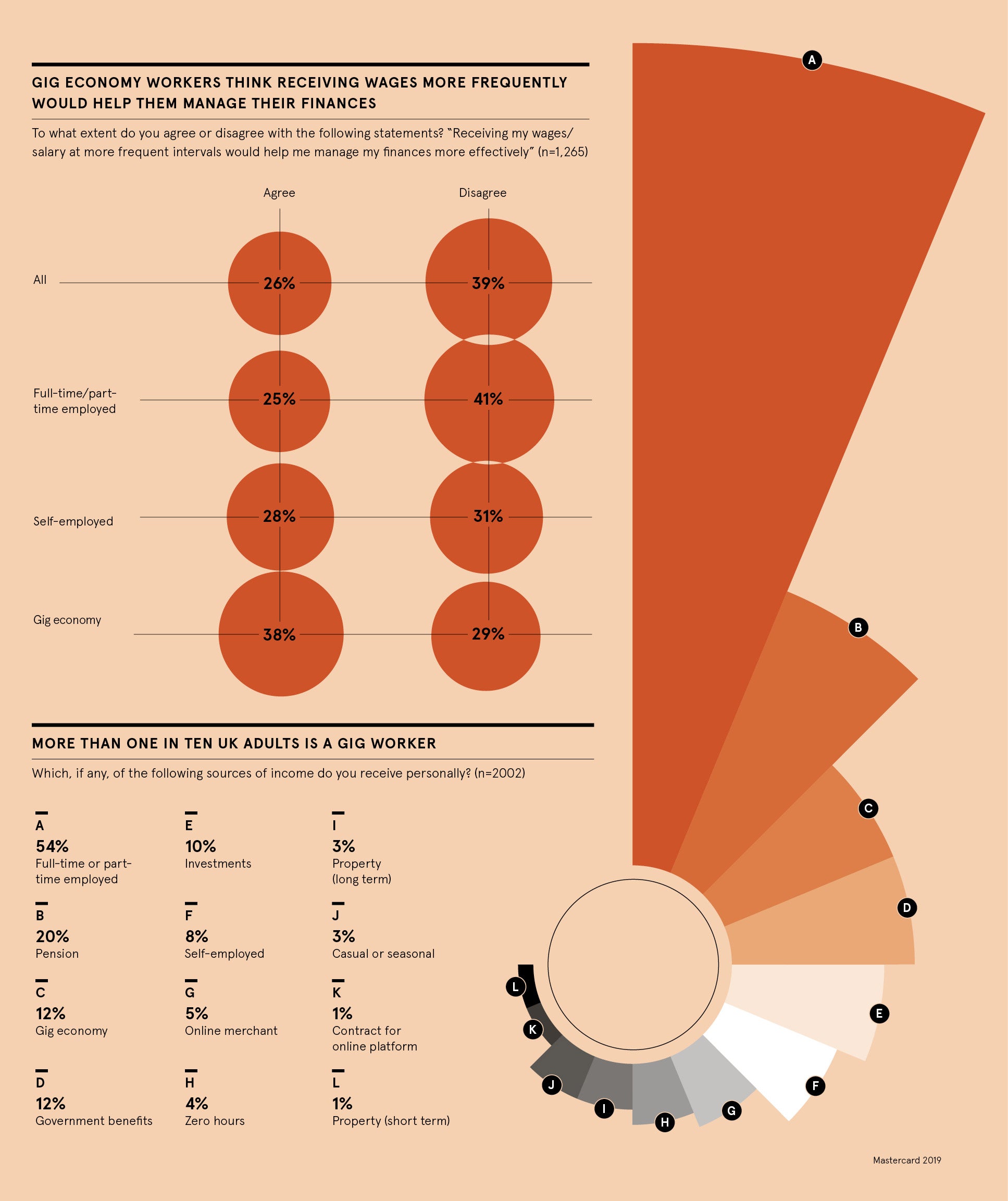

The gig economy is booming, but life as a gig worker can be challenging; the work can be volatile, there are often daily expenses, such as buying fuel for the car. For those who rely on gig work as their main source of income, any delay in receiving earnings can put a strain on personal finances. In a competitive landscape, gig workers will source work from platforms that allow them to access their earnings on demand.

For example, a popular ride-sharing app recognised that paying its workers weekly often wasn’t enough to meet their needs. It implemented a real-time payment

service powered by Mastercard Send™, enabling its workers to access and spend their earnings immediately.

Mastercard Send™ is just as beneficial to small businesses, which can face cash-flow issues. By leveraging the technology, small businesses can conveniently access their earnings on demand, helping them cover daily expenses, such as restocking their store, and helping their business grow.

“Real-time payments can be transformative for small businesses,” says Stoddart. “Research shows companies using real-time payments enjoyed a 16 per cent increase in transactions and spent 46 per cent more than a control group over four months.”⁴

Another key issue for businesses is payment risk. Companies need to monitor suppliers and customers to ensure trading partners are in a fit and proper condition. This is a huge job involving a vast number of credit risk reports, law enforcement lists and media sources.

A better approach is to use a single procurement platform, such as Mastercard Track™. This streamlines procurement by monitoring more than 4,500 sanction and enforcement lists. For suppliers it offers a single portal for credit risk ratings for customers. Preferred payment methods are managed by Mastercard Track™. Using a platform such as Mastercard Track™ ensures maximum compliance with legal duties and frees up staff to focus on core commercial activities.

And finally

Behavioural analytics, innovative new applications and faster payment solutions are all destined to change our financial fortunes as both individuals and small businesses. What’s interesting is how new partnerships are essential to deliver pioneering products, often partnerships that meet customer needs and would not have been thought possible just five years ago.

This era of collaboration will underpin further innovation as the financial sector is disrupted by new, creative ideas designed to boost both companies’ bottom lines and our own financial wellbeing. Technology is profoundly changing our relationship with our money at pace.

Discover more of our thinking on the frictionless future at mastercard.com/frictionlessfuture

1 NuData Security is a Mastercard company

2 Vocalink is a Mastercard company

3 www.ilo.org/global/topics/labour-migration/lang–en/index.html

4 www.mastercard.us/content/dam/mccom/en-us/documents/mastercard-send-debit-lift.pdf

5 Tranfast is a Mastercard company

Sci-fi-style security is here

Innovation in emerging markets

Power of open banking