The marriage of financial acumen and internet prowess has promised to catapult lending from its dull analogue era into a bright future of digital financial technology.

Home Credit, a consumer finance lender established in 1997, hails from pre-fintech times. Judged simply on the year of its birth, the company may seem to need the same digital jolt as other traditional financial institutions.

According to Home Credit, which has served more than 130 million customers from Prague to Manila, that perception is wrong. “What sets us apart is our ability to take fresh ideas and rapidly test and scale them to our millions of clients. We are a global giant that thinks and acts like a nimble disruptor, and that’s a rare combination,” says head of Home Credit’s risk research unit Lubomír Hanusek.

“Our lending expertise and advanced tools let us reach more unbanked customers and offer them the speed and smooth customer experience as well as any fintech startup today can.”

A lot depends on how quickly and reliably the company can assess the creditworthiness of potential customers in a country lacking a centralised credit records bureau. Home Credit demonstrates how its robust technology helps structure anonymised big data using it for highly predictive credit-scoring. This allows the lender to include new customers into a regulated financial industry.

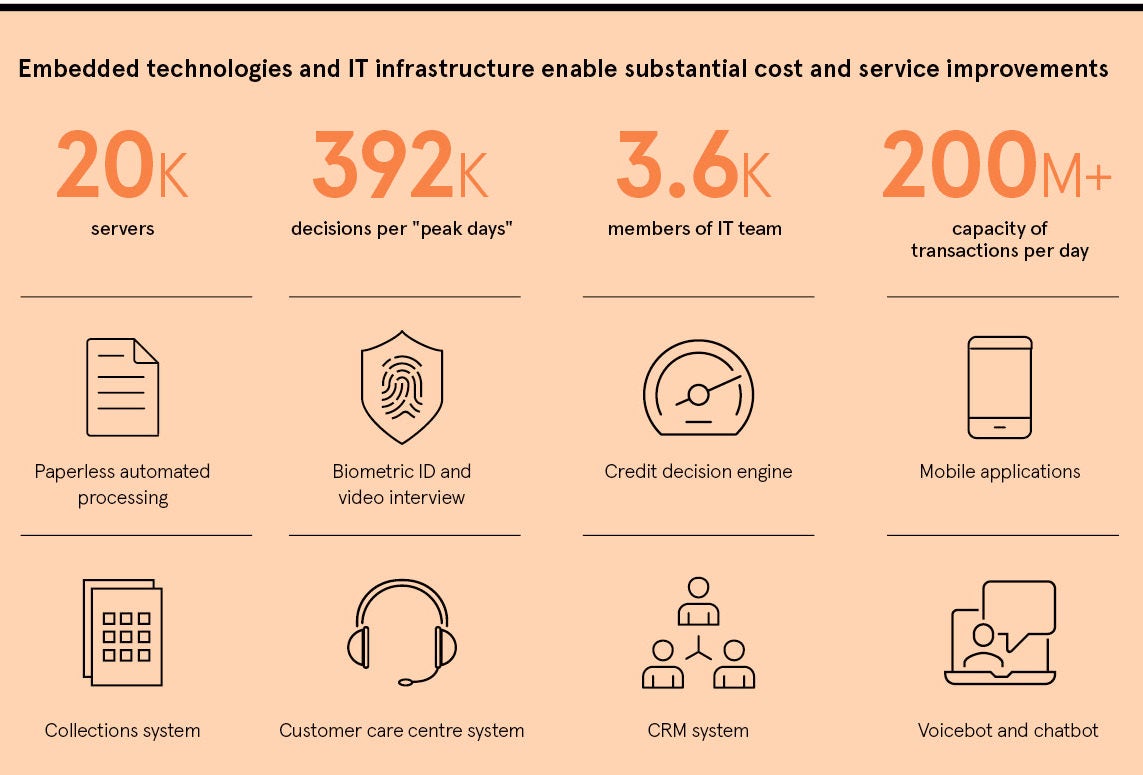

Home Credit uses its global technology and risk platform to manage strategy and credit approvals centrally across nine countries

“When we enter a new market, we need six months to collect enough data to feed our centralised approval models and make them work,” says Mr Hanusek.

The company is primarily using its technologies to cope with growing numbers of new consumers in large Asian markets. As their economies grow, an emerging middle class catches up with opportunities for a more comfortable lifestyle.

Home Credit uses the capabilities of its platform to manage its strategy and credit approvals centrally across nine countries. They include China, India, Indonesia, the Philippines, Vietnam and Russia. These countries have a combined population of almost four billion people or about half the world’s population.

“Our technology platform integrates in real-time data provided 160 different data sources, credit bureaus, telco operators and utilities, and other so-called alternative data. These are anonymised scores based on big data analysis of people’s behaviour processed by third parties,” says deputy chairman of Home Credit’s Russian unit Artem Aleshkin.

Home Credit approves about 200,000 loans every day and two-thirds are new customers. It tracks the growing financial needs of clients and helps improve financial literacy in countries where consumer borrowing is mostly still a novelty.

The company benefits from having started at bricks-and-mortar stores, providing finance for customers seeking to buy household appliances, mobile phones and furniture. As these shops went online, Home Credit followed. It also partnered with pure ecommerce companies throughout its markets, including local payment platforms, such as China’s WeChat and Alipay, India’s Paytm and Indonesia’s GoJek.

No matter where customers look for a loan – shopping malls, eshops or through Home Credit’s mobile app – the application process is paperless. The loan applicant gets a “yes” or “no” response in under a minute. At Home Credit’s business scale, automation is the rule. So far this year, the company has processed 96 out of 100 loan applications without any human interaction. It employs 3,600 IT personnel overseeing more than 20,000 servers and 28 datacentres.

Big data can provide better predictions about future behaviour of borrowers than some traditional questionnaires

The company has also automated some of the work at its telephone customer help desks. “Chat or voice bots currently handle about 200,000 customer calls in China each day and up to 80 per cent of simple queries in India,” says Milan Urbasek from Home Credit’s group operations.

The use of speaking robots is possible partly because clients usually call in with straightforward questions about their loan balances and payment dates. Customers’ behaviour, including interactions with bots, are recorded and fed back into predictive scorecard models. This data collection begins when customers apply for a loan and ends with full repayment.

Home Credit uses artificial intelligence (AI) tools to sift through these troves of big data. The goal is continuously to upgrade the predictive power of scorecards to minimise the likelihood of newly approved customers defaulting on their loans.

Big data is a trendy catch-all term to describe the vast volume of digital traces people leave behind as they go through their modern digital lives. Big data covers information from many external and internal sources, such as non-cash financial transactions, internet use, mobile devices and other digital sensors.

This data can be collected, organised and analysed to assist companies in discovering meaningful correlations that augment predictive behaviour models. Financial companies such as Home Credit can look for patterns to gauge the creditworthiness of their clients against the standard data from credit-

scoring registers.

By definition, big data must pass the four Vs test – volume, variety, velocity and veracity – for company managers to extract any value from it. The four Vs experiment, described by scientists at IBM, makes Home Credit a fitting big data user since it has extensive operations in two large countries, China and India. Both markets generate data input on an enormous scale (volume) in different types (variety) by streaming modes that permit online analysis (velocity) and in the proper, accurate forms (veracity).

Scoring provided by big data companies can outperform a human loans officer. “Big data can provide better predictions about the future behaviour of borrowers than some traditional questionnaires can,” says Mr Aleshkin.

However, some experts warn that big data may lead to biased findings and judgments. Although AI and machine-learning concepts are neutral in the way they function, it is the programmers who have to find the strongest correlation between data and behavioural patterns. Only then can big data and AI help predict the probability of, say, loan defaults by certain types of borrowers. Answering why data findings can show this is tricky and still puzzling.

“Imagine the autopilot of a driverless car,” Alan Winfield, professor of robot ethics at the University of the West of England, told the Scientific American journal. “If there’s an accident, it’s simply not acceptable to say to an investigator or judge, ‘We just don’t understand why the car did that’.”

Home Credit avoids falling into the big data bias trap when evaluating loan applications from people with minimal financial histories by using different weightings for scoring. “We primarily rely on our client and business data,” says Home Credit’s risk research manager Mr Hanusek. “First we look at causations, such as a clean credit record and sufficient earnings attesting to the high probability of problem-free repayment of the loan, and only then do we look at correlations. Big data may statistically show the probability that a customer may default.”

However, predictions based on big data analysis can be very accurate and outperform the decisions based on answers people provide in traditional loan applications. “A traditional loan application might have relied on checking personal income and payment histories, whereas big data can extrapolate alternative information to verify these much more accurately,” says Home Credit’s risk manager Václav Kozmík.

One field where big data science has meshed with AI and has progressed immensely in recent years is voice recognition and machine-understanding of spoken language. The most visible advances focus on major nations and languages spoken by many people. “It’s easier to find reliable voice bots speaking Chinese or Russian than Tagalog, one of the official languages in the Philippines,” says Pavel Dvořák, head of Home Credit’s loan collections in Asia.

For years, robots have helped manufacturers save workers from doing boring and numbing jobs on assembly lines. Voice bots are taking over the tedious work at customer call centres. For Home Credit, the benefits are twofold, the obvious one being reducing costs and the other decreasing the staff churn rate at its call centres.

The company has been able to cut its global headcount in call centres in China by about a third to 7,000 since implementing AI-powered voice recognition services for handling customer care two years ago. “We’ve also seen improvements in customer satisfaction. Customers react positively to robots reminding them to make loan payments,” says head of Home Credit’s loan collections Radek Janušek. “They may feel embarrassed if they hear the same from a real person working at the call centre.”