There has been recent speculation that banks will not survive the fintech onslaught. At Banking Circle we do not hold that view. While they may be hindered by historical systems, traditional incumbent banks also gain from the invaluable and unique benefits of their history: customer loyalty, trusted values, deep market knowledge and understanding.

There has been recent speculation that banks will not survive the fintech onslaught. At Banking Circle we do not hold that view. While they may be hindered by historical systems, traditional incumbent banks also gain from the invaluable and unique benefits of their history: customer loyalty, trusted values, deep market knowledge and understanding.

Banks have the appetite and the resources to reinvent themselves to meet new market needs. This means that when they do build new solutions they can utilise and pass on all these benefits, standing them in good stead for competition with the cohort of disruptors.

Reinvented for the new economy with a modern, progressive outlook, incumbent banks are in the strongest position to deliver solutions that meet the current and future banking needs of small businesses. But to be able to do that, with the flexibility most small firms expect, incumbent banks need good partners to underpin their financial infrastructure.

Building on a financial infrastructure

Banking Circle was launched to help businesses transact more efficiently in the global economy, facilitating international trade by providing fast and affordable payment solutions for businesses previously unable to expand internationally due to the high cost of cross-border payments.

Now, having been granted a banking licence, Banking Circle can deliver game-changing solutions, taking care of non-core activities so banks can focus resources on building relationships and delivering excellent customer service. Free of legacy systems, Banking Circle delivers financial infrastructure at low cost without compromising on compliance or security, providing access to real-time payments regardless of borders and size of operator.

Banking Circle can deliver game-changing solutions, taking care of non-core activities so banks can focus resources on building relationships and delivering excellent customer service

The next generation of banks is just that: the next generation, not an entirely new species. Working with Banking Circle, banks can reinvent themselves to meet new market needs, seizing opportunities in the new economy without significant investment in their internal infrastructure.

Big banking solutions for small businesses

Passionate about improving financial inclusion for small and medium-sized enterprises (SMEs), Banking Circle commissioned MagnaCarta Communications to research these issues. Published in a white paper, Circle of trust or out of the loop?, insights are provided by some of those working in the midst of challenges, as well as people delivering solutions to the challenges.

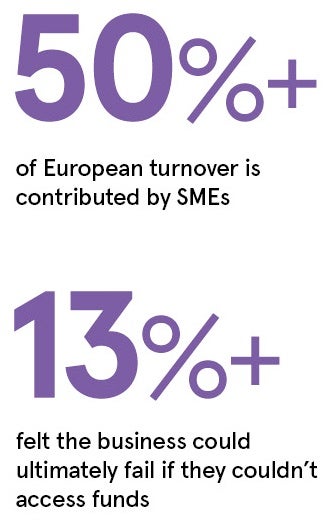

The research highlights an imbalance in support available to SMEs; just one in five SMEs have not experienced problems borrowing from a bank to support their business. Demonstrating the potential impact of financial exclusion, nearly a quarter of respondents believe struggling to access additional funds would lead to redundancies. More than one in ten feel the business could ultimately fail as a result.

Thankfully, providers are beginning to realise the potential of the SME banking market and are appreciating that if they get an SME on board, the business will be loyal and bring multiple cross-selling opportunities.

For SMEs and startups to be in the best position to compete and prosper they need full and fair access to global-scale financial services. This starts with access to bank accounts, offering the ability to transact in the business’s local currency as well as the currencies of the countries in which they wish to trade. The ability to transfer funds into these other regions is essential as is the availability of working capital to support growth.

Slow settlement cycles, especially through online marketplaces, can have a devastating impact on a business’s working capital, reducing its ability to restock, increase headcount, upgrade equipment or move to larger premises. Unable to advance and grow the business through these channels, SMEs stall and many ultimately fail.

Looking to the future of banking

The past 15 years or so have seen significant change in the market, yet comparatively little change in the payment process and timescales involved. If we look ahead 15 years, expecting the rate of change to continue or even accelerate, it is impossible to believe that current mainstream payment options will remain fit for purpose.

Digitalisation allows consumers to purchase goods from sellers anywhere in the world, without a second thought for details such as foreign currency exchange rates. Of course, when using traditional cross-border payment solutions, the SME seller takes a costly hit in transfer fees or slow settlement cycles, or both.

For an SME to keep up with the rest of the market, it must restock rapidly and expand to new markets and territories. That requires working capital, which in turn demands faster payment processing. To deliver this, financial services providers need to start working together more closely.

There is a real need to collaborate to deliver solutions which help, rather than hinder, SME growth. Real-time or instant payments are essential to allow SMEs to keep up with the pace.

To download a copy of the Banking Circle Insight Paper please visit www.bankingcircle.com/whitepapers/circle-of-trust-or-out-of-the-loop