For many savers, the future looks bleak. Current calculations show that most people will struggle to maintain their lifestyles unless they save around £10,000 a year for retirement. Recent research points to a £318-billion annual pensions shortfall in the UK. Most people do not realise that an annual income (annuity) of £50,000 in retirement requires a pension pot worth in excess of £1 million.

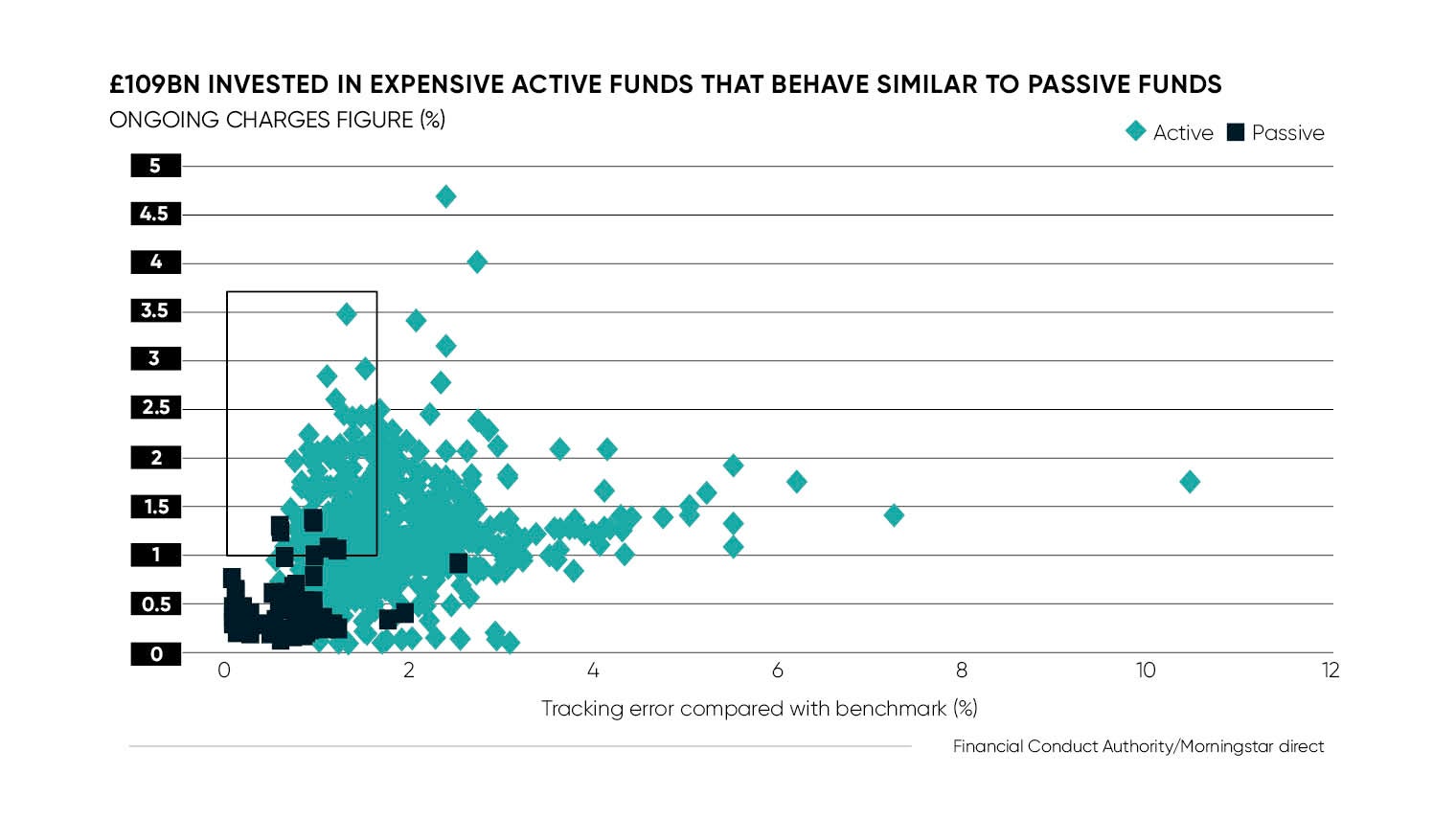

A number of factors are making it difficult for savers to achieve a large enough pension. Actively managed funds are expensive and many financial advisers demand customers have a wealth of at least £500,000. Managing investments on your own is daunting, and of those who brave the complexity of the markets alone, many soon realise that their emotional decisions and lack of professional tools hinder their performance.

Due to these challenges, many of those wanting to grow their money have relied excessively on keeping it in cash, principally in cash ISAs, which are delivering only meagre returns. Meanwhile, the property market, long seen as a safe investment, is widely regarded as being “overheated”.

Due to these challenges, many of those wanting to grow their money have relied excessively on keeping it in cash, principally in cash ISAs, which are delivering only meagre returns. Meanwhile, the property market, long seen as a safe investment, is widely regarded as being “overheated”.

But the capital markets have continued to deliver long-term positive returns. “There is a huge market of people ready to invest a substantial amount of money here, but many of those people don’t know the best steps to take,” says Adam French, UK chief executive and co-founder of online investment manager Scalable Capital.

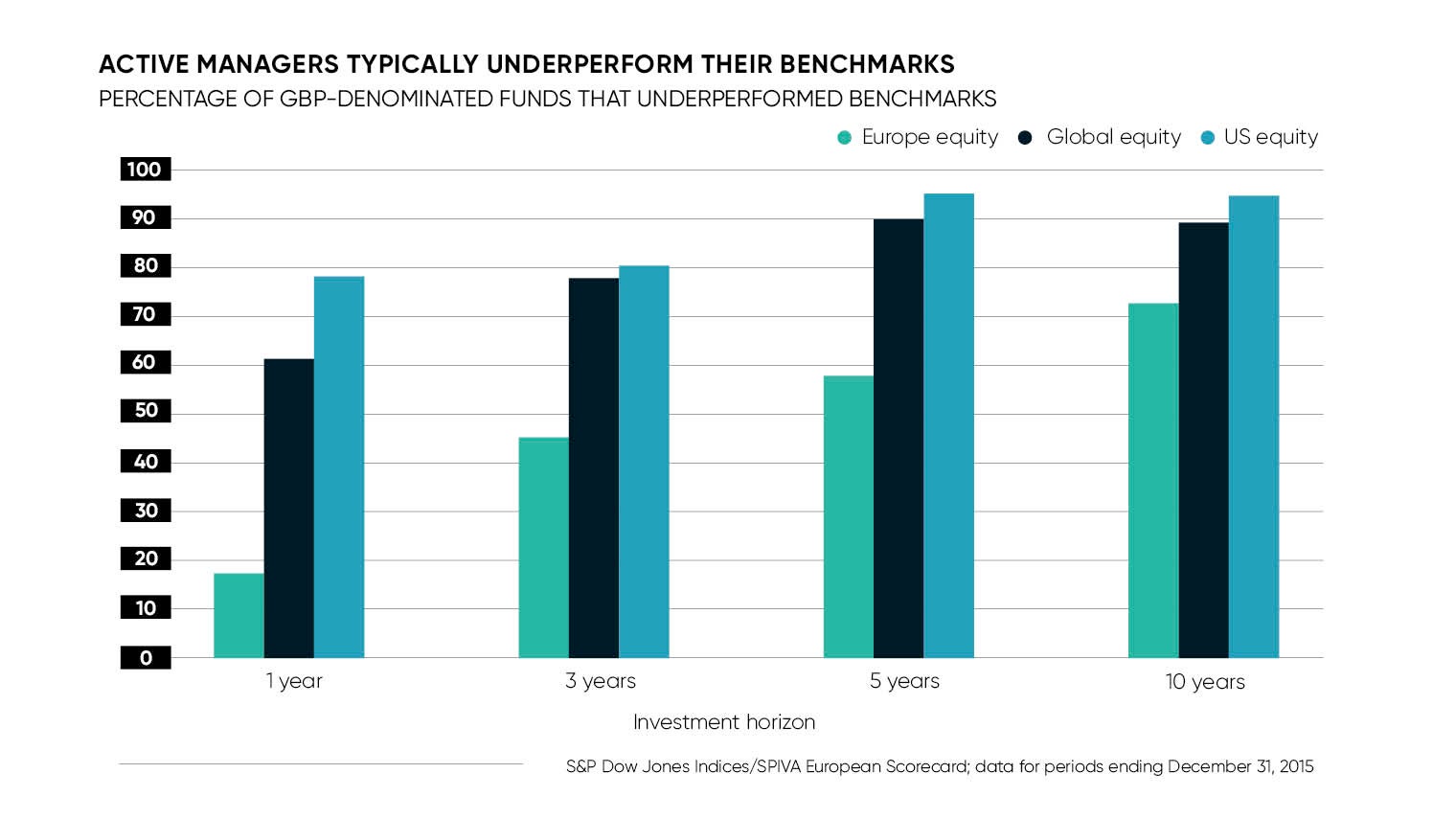

“Some 80 per cent of the ISAs opened each year are still in cash and are not generating much of a return. When people look to active funds, they find they are too expensive and, more often than not, underperforming.”

Retail investors typically underperform the overall market by up to 3 per cent a year. Mr French says: “It’s a bit like trying to fix your own car – you shouldn’t really try it unless you know what you’re doing.”

INVESTMENT OUTCOMES

Companies such as Scalable Capital have made it their mission to offer savers a better alternative for investing their money for the long term. They are using technology to change investing fundamentally, delivering a service akin to a private wealth manager, but with much greater accessibility and far lower costs.

Scalable Capital uses technology to off er much greater transparency, with investors able to view the performance of their portfolios and their current value at any moment via their mobile apps or on their website

They employ a data-driven investment approach based on sophisticated algorithms that are constantly reviewed and tested by a team of data scientists and financial experts. While the use of such algorithms has gained considerable traction when it comes to managing large portfolios worth billions of pounds, until recently retail investors had been largely unable to capitalise on the advances.

Data-driven models help this new breed of money manager to deliver better returns for every unit of risk an investor is willing to take. Sophisticated quantitative models take the latest findings of capital markets research into account and model the complexities of the markets accurately. Using algorithms can therefore achieve fundamentally better investment outcomes, while the application of technology at every step of the process also lowers the fees for investors.

Scalable Capital is a well-known provider in this emerging field and is among the largest technology-based investment managers in Europe. The company has grown in its first year to the position of having more than £100 million of assets under management, overseeing in the process the portfolios of thousands of clients.

The company’s smart asset allocation model dynamically adjusts clients’ portfolios so they constantly match the individual risk tolerance of each client, in all market conditions, helping investors to stay invested even during periods of market stress.

Thanks to data-driven models, the risk relevant to each portfolio can be expressed as a clear annual downside risk instead of the traditionally used, yet ultimately meaningless, labels such as “moderate risk” or “low risk”. This means Scalable Capital’s clients can choose from an array of twenty three risk categories instead of having to content themselves with just five model portfolios that don’t provide sufficient transparency about their actual downside.

HUMAN TOUCH

HUMAN TOUCH

Humans devise and monitor Scalable Capital’s algorithm, which can crunch numbers at a rate no individual investment manager could ever replicate. Scalable Capital also uses technology to offer much greater transparency, with investors able to view the performance of their portfolios and their current value at any moment via their mobile apps or on their website.

“Previously, investors have had to wait six months for a statement, during which time they could have lost 20 per cent of the value of their portfolio with no one acting – now they can see their portfolio performance in real time,” Mr French points out.

Another selling point is the ease of getting set up and also delegating the investment process. Compared with the time needed to learn about and stay on top of the financial markets, customers need only go through a short questionnaire to create a personalised portfolio suitable for their individual risk tolerance. Scalable Capital’s team of financial experts carry out daily monitoring and performance optimisation of every client’s portfolio.

Our low fees and controlled approach to risk mean investors can grow their money efficiently and safely, and get ready for the retirement they deserve

The company’s fully managed service means investors can get in touch with the client services team at any time. In-person seminars and online webinars also help investors to find out more about their service and get investment insights.

While providing investors with a top-notch, personalised and modern investment solution, the company’s fees are set at just 0.75 per cent of a customer’s annual investments, making it “cheaper than three quarters of the other options in the marketplace, while offering a much more advanced investment solution”, says Mr French.

So how should cash-rich, time-poor people grow their retirement funds? Scalable Capital encourages investors to begin immediately and not be put off by the market’s complexity.

“Starting early and setting up a monthly savings plan gives investors the benefit of compound returns,” Mr French says. “Our low fees and controlled approach to risk mean investors can grow their money efficiently and safely, and get ready for the retirement they deserve.”

To find out more about investing with Scalable Capital please visit www.scalable.capital

With investment comes risk. You may get back less than you invest. Please note the risk warning on our website