The banking landscape as we know it is changing. A new wave of technology is revolutionising the way customers engage with their finances. From social to mobile capabilities, banks are having to rethink the way they do business to deliver a better customer experience and remain competitive.

The recent introduction of open banking and the Payments Services Directive 2 (PSD2) regulation is accelerating this transformation by placing power in the hands of customers. Banks must now allow customers to share their financial data, such as spending habits and regular payments, with authorised third-party providers if customers wish to do so. To navigate this unchartered reality, banks must ensure their digital offering is fit for purpose.

Dan Jones, partner and head of Capco’s UK Digital practice, says convenience, speed and flexibility are no longer considered attractive add-ons, but have become a standard expectation of the rapidly changing customer-bank relationship. According to Mr Jones, successful organisations will be those that can keep pace with customer needs and demands, and embed appropriate services into the wider ecosystem of digital products.

Agile approach

Banks traditionally operated in silo channels, with different business areas operating independently of each other. Although they accumulated vast amounts of data about their customers, such an approach could not provide specific insight into customer activity, needs and preferences from which to develop new products tailored to the individual.

For Mr Jones, the pace at which regulation and digitalisation is developing means banks need to adopt an agile, iterative way of working to remain competitive. They need to put the customer at the heart of the design process and take new products to market quickly.

“The introduction of open banking and PSD2 will see a new way of banking emerge,” he explains. “It will allow the industry to innovate and enhance customer service, and help new entrants gain a share of new financial products and services. But banks will only stay ahead of the game if they embrace an agile approach and view the changes as an opportunity rather than an obligation.”

Of course, the move to this new way of working does not come without its challenges. Large banks have built their technology and data around individual products and channels, and are beholden to legacy systems.

Banks need to reach a point where they understand the needs of the customer, without taking any direct feedback

To overcome this, banks must invest in technological capabilities that allow them to become more intelligent about customers’ needs, says Mr Jones. They must incorporate the right architecture to respond quickly and drive an agile culture throughout all the corners of the business.

Chris Probert, Capco partner and head of UK data, explains: “Both top and bottom-line growth depend on banks overcoming the challenge of large and costly legacy infrastructures. As transactions and services continue to move from the physical to the purely digital, banks will find speed to market and flexibility invaluable.”

Smart data

Tech-savvy customers are increasingly seeking a user experience nuanced to their particular needs. Central to a bank’s success in the digital economy is therefore the data they accumulate about customers and intelligent ways of processing it.

Digitalisation and data are so tightly entwined, one could not function without the other. You only need look at the phenomenal success stories of Amazon, Facebook and Google to understand the impact customer data has on customer experience.

While challenger banks have the distinct advantage of being agile and customer centric, legacy banks potentially have the upper hand due to the sheer volume of data they hold, as well as being trusted, long-established brands.

Mr Probert says: “Legacy banks have a huge challenge in implementing digital strategies, but if they harness the data they have and maximise the effectiveness of its uses, they could develop successful client-orientated products. What they must not do is sleepwalk into the future and be leapfrogged by the challengers.”

For both legacy and challenger banks, the operative word is “harness”. Captured data is only useful if banks can use it effectively. Banks must ensure they have easily accessible, high-quality data. This is where technology such as data virtualisation has a key role to play.

“It’s not about volume; the true game-changer will the application,” says James Arnett, Capco partner. “The future is real-time, data-driven services. By gleaning meaningful insights, they can create audience segmentation and deliver innovative, customised products in a way that appeals to customers.

“Banks need to reach a point where they understand the needs of the customer, without taking any direct feedback.”

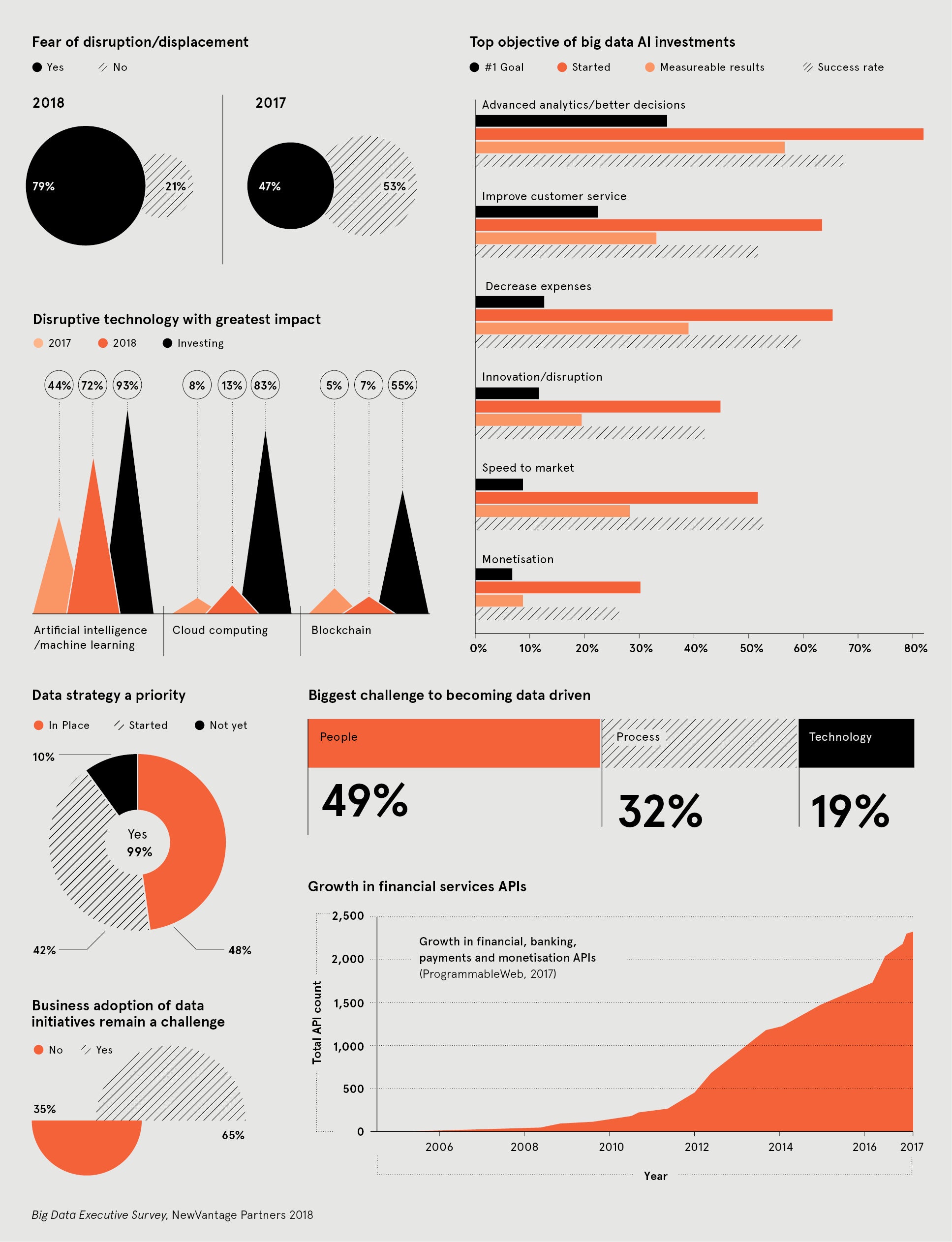

(click to enlarge)

Digital collaboration

While we have come to expect driverless cars and robots will be part of our not-so-distant future, it should be equally straightforward for us to envisage a future banking system with its own form of artificial intelligence (AI).

If there is one thing we can bet on, it’s that time waits for no bank

Many banks have already taken advantage of AI-enabled tools such as chatbots to interact with customers, but that is just the cusp of what is to come. From virtual financial assistants to automated credit scoring and predictive analysis, AI has the potential to refashion organisations on an unprecedented scale.

Mr Jones explains: “From a customer point of view, machine-learning is starting to enhance their experience in smart ways, quickly and efficiently resolving their problems.

“Perhaps more importantly, AI and machine-learning will allow banks to spot patterns and solve customer problems at a fraction of the current speed in a very cost-efficient manner. It’s about making informed assumptions about the future that will drive customer value.”

This second wave of disruption will have a powerful impact, transforming the banking industry and with it the customer journey. Now is the time for banks to seize the opportunities technology presents to shift to the next gear. Because if there is one thing we can bet on, it’s that time waits for no bank.

Q&A: Open banking revolutionises the face of financial services

Lance Levy, Capco CEO

How have banks responded to the launch of open banking?

This is the beginning of what is shaping up to be a very exciting new chapter for the financial services industry. Around the world, the digital revolution means customers are looking to transform the way they bank and manage their money.

In Europe, the Payments Services Directive 2 is setting application programming interface (API) standards for payments and the same is happening across the UK. These regulations have been designed with increased competition in mind and to offer

customers greater control over their money. However, the emergence of a new API-enabled market is a game-changer. It has the power to fragment products and services that large banks have historically owned, on an unprecedented scale. It will allow new providers to enter the market and transform banks into open platforms.

Until now, these banks have largely focused on becoming compliant with open banking regulation. However, I believe we will see a wave of technological innovation, especially through the latter half of 2018, as banks and new providers alike look to unlock revenue streams we haven’t yet imagined.

There is a huge potential for banks to transform their products and services, but the key is to focus their attention in the right way. Open banking requires banks to think beyond their own needs and business growth; they must meet untapped customer needs and prove invaluable to distributors.

Is the customer ready for open banking?

In recent years, we have seen the boom in technology bring about a shift in consumer expectations. Today’s digital-savvy customer views apps and websites as an eco-system, so yes, customers are ready and the financial services industry must keep pace.

This is particularly the case for millennials and generation Z, who have grown up in an era where efficiency, speed and interconnected devices are the norm. Older generations, however, tend to have stronger ties to their financial providers, so may be slower to embrace the change.

Open banking offers consumers lots of tangible benefits, including new insights to help them better manage their money, access to products that may not have been previously available and the opportunity to obtain a single view of their finances.

The younger consumers are looking for services that are tailored to their “money milestones” and they’re prepared to put their trust in third parties that may not be banks. They have grown up during a period of financial turmoil and slow economic recovery; there is less loyalty to the big banks. They want lower prices coupled with better quality service and the introduction of open banking will help them achieve that.

Will we see significant changes in the banking business model?

While open banking presents an unrivalled opportunity for startups and fintechs to move into unchartered territory, it also allows existing organisations to improve their offering; it is challenging banks to raise their game.

Banks need to remember that they do not have a captive audience. Times have changed and some clients will migrate where the best services are, regardless of where the underlying product sits. For example, customers could use a new fintech app, banking website and customer service model, but the current account that sits at the heart of it is held with an existing large bank that the customer will no longer interact with directly.

First and foremost, banks must decide if they want to continue to own the customer relationship. Banks hold a huge amount of raw data and information, but they need to be smarter in the way they utilise it for the benefit of the customer. Digital-first services offer greater value to consumers and banks need to work out how they will tackle this. They can either form partnerships with aggregators to take ownership of the user interface or they could choose to retain ownership through building their own platform.

I believe organisations are becoming much savvier about building collaborations to deliver best results for customers. We’ve already seen some fantastic examples of partnerships in this space and, going forward, I expect we will see the emergence of new and exciting collaborations, tools and services as banks seek to find their way in the new market.

How can banks monetise the data they have?

You need only look at companies like Google and Uber to see the vast benefits of being smart with data. Banks are in a uniquely powerful position with the volume of data they possess, and we are a seeing a global shift towards not only capturing and analysing data, but monetising it.

Developments in data analytics have allowed financial institutions to obtain a 360-degree view of the customer, enabling them to improve the range of services and enter new markets. Open banking will lead to a rise in data exchange between banks and third parties, and I think we will see banks increasingly recognise the value of offering free services in return for data. Ultimately, if a customer feels they are being offered a relevant, tailored product, they are far more likely to buy it.

For more information please visit www.capco.com

Agile approach

Smart data