Imagine a dystopian future when access to the stock market has been restricted to institutions and the ultra-wealthy. Private investors, newly disenfranchised, have woken up to the scary reality that a small number of elite finance professionals now control the stock market.

In this imaginary world, perhaps some investors would simply keep their cash in the bank. But many would surely be furious at the removal of these basic democratic freedoms.

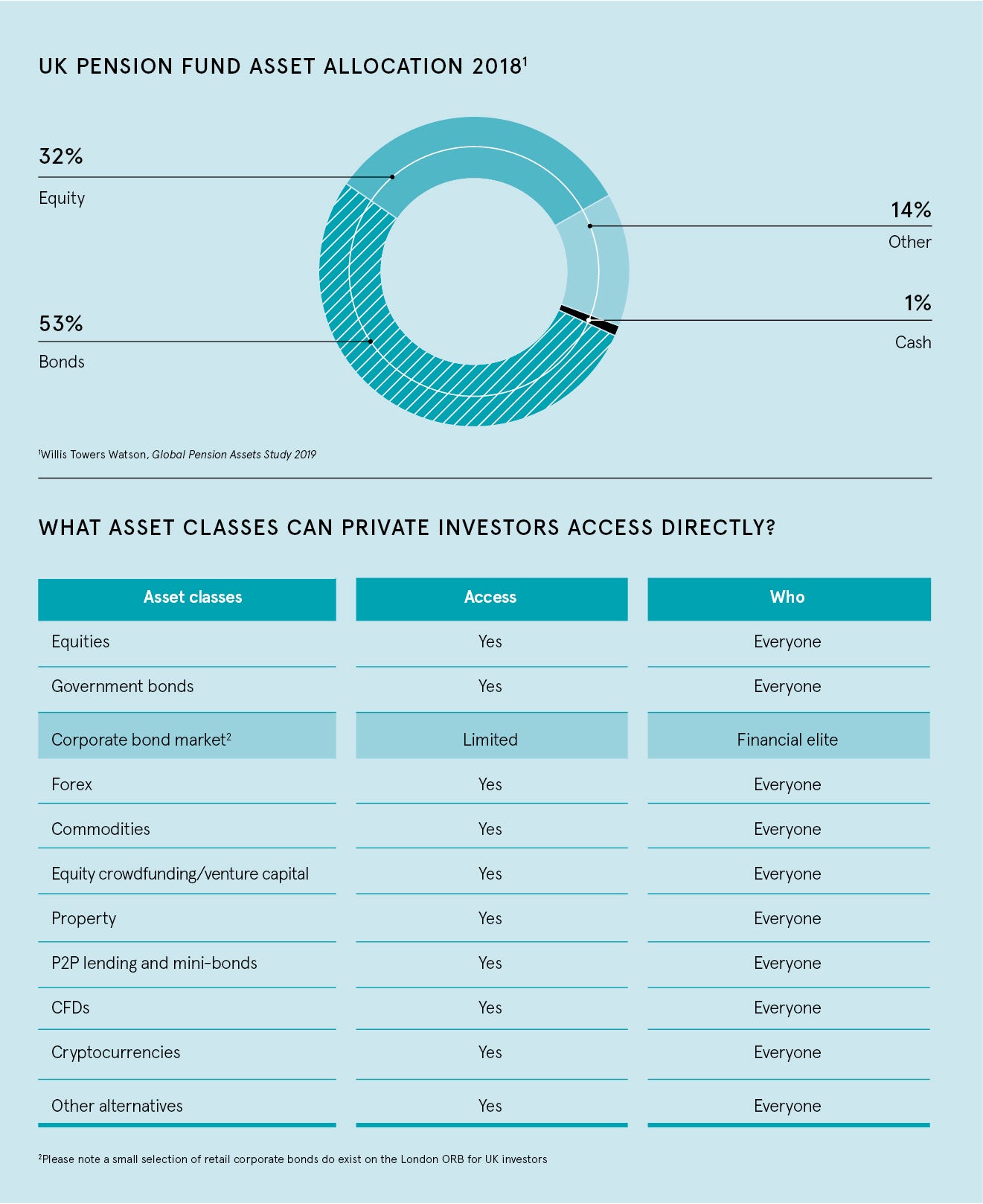

This scenario may seem far-fetched, but when most private investors look at corporate bonds this is what they see: an appealing asset class, restricted by a powerful elite. The institutional, club nature of the corporate bond market, limited online trading venues and minimum purchase sizes typically above £100,000 a unit immediately shut out almost all private investors.

There has been an increasing clamour for this to change. In an environment of persistently low interest rates and growing inflation, investors want better returns and greater reliability than the often volatile equity, commodity and currency markets.

It’s time for bond markets to enter the digital age and open up to all investors

It remains to be seen if European bond markets will become as developed as their US counterparts, where an estimated 19 per cent of corporate bonds are held by retail investors1. A recent European Commission study2 insists the market be enhanced, noting its importance to investors reducing equity exposure. Bonds already form a large portion of UK pension asset allocation3, so why is this different

for individuals?

In the UK, several projects have attempted to free the bond environment from its shackles. Most notable is the creation of the London ORB, a market open to private investors, but only containing a limited selection of corporate bonds at any one time, with typically lower yields, high cash prices, long maturity dates and ever-smaller corporates using it to issue.

The closed-off nature of corporate bonds is particularly conspicuous when we consider that between 2006 and 2018 they have outperformed the largest 100 London-listed equities. Barclays calculates that sterling investment-grade fixed income returned 5.2 per cent annually in the period, compared to the FTSE 100 at 4.5 per cent4. This is not to mention the superior performance of high-yield paper, which returned 6.9 per cent, according to Bank of America Merrill Lynch5.

In addition, with more than £3.1 trillion of bonds outstanding in the UK, the Bank for International Settlements notes the UK corporate bond market is larger than the London-listed share market6. According to McKinsey, the value of corporate bonds outstanding worldwide has nearly tripled in the decade since the 2008 financial crisis7. Many companies issue both equities and bonds in a bid to optimise their capital structures.

The barricaded nature of the bond market means that private investors have not been able to select from such instruments for truly diversified portfolios. While private individuals have been able to invest in company debt through small business peer-to-peer and mini-bond lending, this has been beset by numerous failures and concerns of default.

Corporate bonds, by contrast, are encouraged by the long-running purchase programmes of central governments and by the reassuring fact that each issuance receives a rating from the main agencies, Moody’s, S&P and Fitch, and offers valuable transparency given the openness of corporate reporting and associated press coverage.

Crucially, recent technological innovations have greatly opened up the potential for access to the bond markets. The concept of fractionalisation, or splitting into smaller sizes, has been employed for stocks with high prices and this is now being applied to corporate bonds, which means much smaller purchasing sizes and online trading.

“It’s time for bond markets to enter the digital age and open up to investors,” says Rezaah Ahmad, chief executive of WiseAlpha, which offers exposure to corporate and high-yield bonds to anyone with as little as £100 per investment. “In our opinion, the corporate bond asset class is the best mainstream risk adjusted asset class, and we believe greater access and choice should be available to all private investors.”

Typically, until recently, even funds wanting to invest in the mainstream fixed income markets would have to call a trading desk at an investment bank, with little price transparency. “Even though bonds are a multi-trillion-pound market, they are as antiquated as the stock markets were 50 years ago,” says Mr Ahmad. “Amazingly, this method of trading still accounts for 80 per cent of bond volume in the US and is higher in Europe.”

WiseAlpha has sought to open the market by fractionalising the bonds of FTSE 250-size companies, dividing them into affordable tranches and allowing individuals to gain exposure to bonds issued by household names ranging from Virgin Media and Thames Water to the RAC, Tesco, John Lewis and many others. People can choose the companies of most interest to them or use WiseAlpha’s robo-manager service to help diversify their portfolio.

“Our mission is to transform and rebuild the corporate bond market,” says Mr Ahmad. “We have started a big change and we expect policymakers and regulators to further aid the liberalisation of the market, as they look to support greater consumer financial welfare, and to introduce healthier fixed income choices, more electronic trading initiatives, greater transparency in corporate financial reporting and fewer systemic risks.”

Private investors are looking to establish more diverse portfolios and the opening of the bond markets will transform their options. The level of return on offer, given the risk profile, is hard to ignore.

To find out more about the corporate bond asset class please visit wisealpha.com

We do not offer investment or tax advice. We recommend investors seek professional advice before deciding to invest. As with all investing your capital is at risk. Please remember bonds are investments, not deposit-protected savings products. This financial promotion has been commissioned by WiseAlpha Technologies Limited, which is authorised and regulated by the Financial Conduct Authority (No 751087). “Private investors” is used in this article to refer to individual investors.

1Deloitte, The Corporate Bond Report 2018

2European Commission, Analysis of European Corporate Bond Markets

3Willis Towers Watson, Global Pension Assets Study 2019

4Barclays Sterling Investment Grade Index LC61TRGU FTSE 100 Total Return Index TUKXG

5Bank of America Merrill Lynch Sterling High Yield Index HL00

6£2.24-billion FTSE All-Share market cap (Bloomberg 2018). £2.6-trillion financial and £511-billion corporate bond market (BIS)

7McKinsey, Rising Corporate Debt