Insurance may be one of the world’s oldest industries, but it is as prone to disruption as any other. For the first time, consumers and businesses alike are demanding digitally enabled products with more transparency, flexibility and fairer pricing. To compete, insurance incumbents need to evolve their workforce and strike partnerships with both new entrants and adjacent players in a more open, collaborative ecosystem.

Historically, small and medium-sized enterprises have sought advice on insurance through brokers and intermediaries. In recent years, however, this has changed significantly, as small business owners have increasingly wanted to purchase insurance in the same way as they buy their own personal cover, on their mobile or desktop devices, with a digital experience. They want to make claims and get reimbursed in the same way too.

The situation is similar in the life insurance market, where independent financial advisers (IFAs) may still be a firm fixture, but a growing number of people are more comfortable transacting online. Closing the life insurance gap – half of adults have never bought life insurance, a recent PwC Currency of Collision survey found – and meeting the digital expectations of those that do, requires transformation in the front and back office of insurance companies, and automation of both servicing policies and processing claims.

Some new insurtech entrants have gained quick traction by capitalising on this demand for more customer-

centric and digitally enabled services. Having initially viewed them as a threat, insurance incumbents are now seeking to develop innovative propositions in collaboration with them. Manulife, for example, has partnered with Irish travel insurtech startup Blink, whose technology monitors global flight disruptions in real time on a suite of products that enable travellers to claim on their insurance policy without the inconvenience of submitting proof that a flight was cancelled or delayed.

There are clear benefits for collaborative insurtechs too, providing access not only to large customer groups, but also the brand equity that companies have spent decades building. In insurance, perhaps more so than any other industry, customers seek brands they know and trust. John Lewis and Marks & Spencer are examples of two companies that have leveraged their brand recognition to drive success in the insurance space.

“A lot of traditional players may have resisted this direction for a while, but they’re now seeing the need to collaborate. The pace of change required to survive and indeed thrive in the marketplace is rapid,” says Jim Bichard, UK insurance leader at PwC. “Most are only at the beginning of that journey. Even if they are several years in, fundamentally their business model is still pretty consistent with how it has been for a long time. But working with those new entrants and technologies can accelerate transformation.”

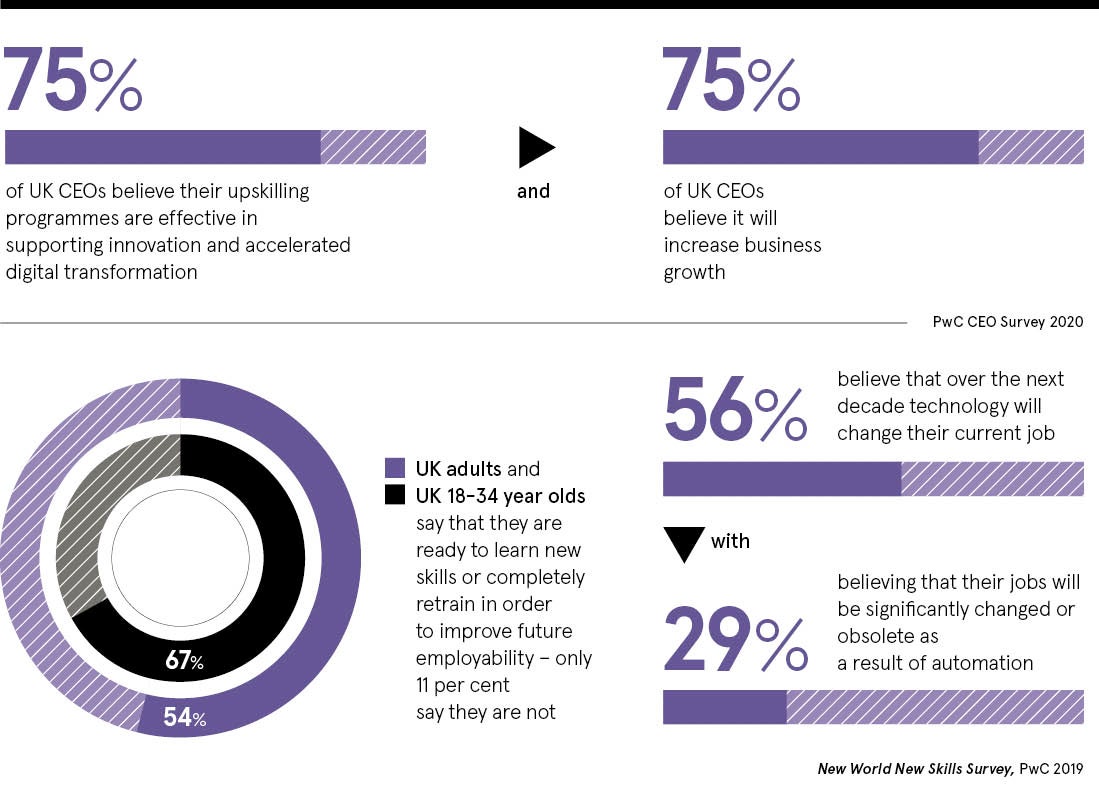

The outlook of insurers has arguably never been as positive, providing they can embrace the opportunity that disruption presents and evolve their workforce

While customer switching is not perhaps as prevalent in insurance as it is in banking, it’s still a major concern for companies. Certain areas of the insurance market, including life insurance, tend to be very opaque, making it difficult for customers to understand what they’re buying. Regulators are trying to drive more transparency and fairness. The Financial Conduct Authority’s recent review of home and motor insurance found that loyal customers can pay far more for the same risk than newer customers. The same review found six million customers could save £1.2 billion if they paid average premiums instead.

Savvy insurers are seeing an opportunity to get on the front foot to increase loyalty or take market share. Saga, for example, has launched a three-year fixed car insurance product, providing the clarity and simplicity consumers desire. Others are embracing flexible models such as pay-as-you-drive car coverage, and startups such as Anorak are releasing clear and tiered offerings with no hidden fees or charges. By responding to customers’ demands, companies are identifying ways to take a lead in sub-sectors of insurance, driving industry convergence and new opportunities for growth.

“Customers have previously been most influenced by price and while that’s still important, we’re seeing a significant resurgence of brand value and service quality in decision-making,” says Christine Korwin-Szymanowska, partner in PwC’s Strategy& business. “That’s good for some of the incumbents, but also adjacent players such as retailers or consumer brands. Differentiating based on claims service and after care is likely to be more important than pricing, so insurance firms need to prepare for that.”

While technology is vital to enhancing transparency, removing barriers to buying and enabling the experience that customers crave, transformation will not succeed unless it places people at its heart. However, keeping up with changing talent requirements is the most difficult challenge of all, requiring not only a willingness from staff to invest in themselves and embrace a different way of working, but also an understanding from companies of how to adapt their talent capacity and prepare a workforce for the future.

Companies that overlook the talent and mindset shifts needed to stay connected to their customers’ evolving needs risk being blinded by digital. This is where partnerships are providing further value to incumbents. Collaborating with startups brings more than cutting-edge products and services, it also brings the skilled people who can develop and maintain them and provide a fresh take on how to meet customer expectations.

PwC’s latest Global CEO Survey shows that, following an initial period of fearing digital disruption, insurance chief executives are increasingly positive about the future. Rather than feeling threatened by technology and worried about how they can work in harmony with it, they are now thinking about how they can work collaboratively with startups to increase their digital capability, as well as grow revenue and access new markets.

AIG, for example, has partnered with online mortgage broker Habito, recognising opportunity because getting a mortgage is a common decision point at which people also purchase life insurance. When applying online through Habito, customers are asked if they’ve considered getting life insurance and are posed nine simple questions to do so.

“The outlook of insurers has arguably never been as positive, providing they can embrace the opportunity that disruption presents, and evolve their workforce,” says Bichard. “Transformation needs to happen, but the crucial element is talent. How do you take your people with you? How do you think about digital upskilling and the workforce of the future? Using our knowledge of the global market, we help our insurance clients understand what transformation really means to deliver value; we support them from strategy all the way to execution.”

For more information please visit pwc.co.uk/currency-collision/insurance