Consumers have multiple payment options, from cash and cards to phones and mobile wallets, QR codes and peer-to-peer (P2P) payments. Cards and digital payments focus on convenience, yet PIN codes and passwords often slow down transactions and frustrate buyers, and contactless payments can only be made up to a certain value which varies by market.

People are looking for faster, easier purchasing, yet at the same time they are also becoming much more discerning about security. This has been perceived by the industry as a problem; convenience and security have often run at a tangent. By better securing fast contactless card purchases, the payments industry can solve the challenge and they can also raise transaction limits.

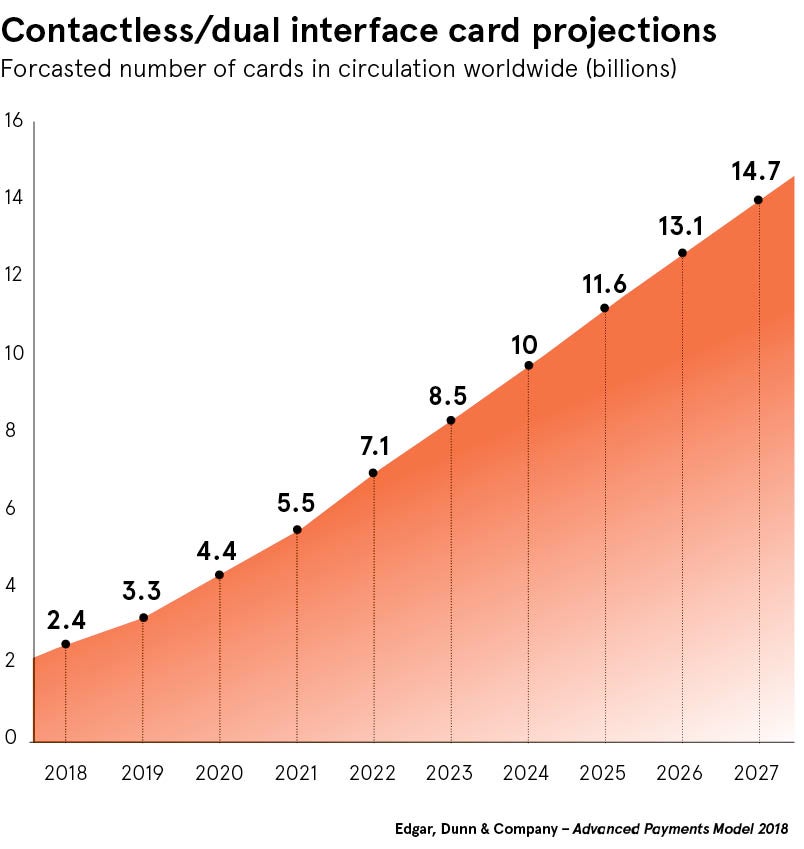

Contactless adoption, which has lagged in markets outside the UK, has become a core part of card and bank strategies that attempt to improve the purchase process. An A.T. Kearney report forecasts US banks alone could generate $2 billion in extra earnings over five years with the technology, aside from the huge benefits to retailers.

Biometrics is transforming this area, by identifying consumers and enabling the elimination of passwords, PIN numbers and low transaction limits. Simple fingerprint recognition allows consumers to touch the sensor on the card and instantly conduct the transaction the same way they are used to with their contactless card, without worrying about any transaction limit except their own credit allowance. At the same time, they have the peace of mind that others cannot take their card and go round stores using it.

Consumers are accustomed to biometrics technology, already using it to log on to their smartphones or make payments on them, and they are demanding this functionality on other common devices, including their debit and credit cards. In addition, governments and regulators are promoting biometrics as reducing fraud and identity dangers.

Such increased use of biometrics in everyday life is normalising the technology and reducing any consumer concerns about changing habits. Card issuers such as Visa and Mastercard see the technology as the next generation of security. A Visa survey found in the United States 67 per cent of consumers are interested in fingerprint recognition for payments because it is easier and more secure than passwords and PIN numbers.

As cards overtake cash as the most prevalent form of payment in many markets, biometric cards are expected to take centre stage. This will happen in part in the context of smartphone payment apps, smartwatch transactions and P2P taking some time to achieve critical mass, and then when widely adopted creating further consumer desire to use similar technology on all their cards.

Banks, card issuers and retailers have begun a number of biometric payment card tests. “Initial feedback from the pilots is positive and now there is a race among many firms to be first in offering the product,” says André Løvestam, chief executive of biometric authentication firm Zwipe. More pilots are expected in the coming few months, with a wide rollout of the cards from 2019.

According to analysis undertaken by Edgar, Dunn & Company, the total available or addressable global market opportunity for biometric cards is projected to be around a billion cards by 2023-24. Biometric payment card growth is likely to be fuelled by markets in Asia followed by Europe, Latin America and North America. The addressable or available market opportunity represents the total number of cards that could potentially be converted to biometric payment cards.

Issuers can increasingly see the opportunity to generate more revenue, with increased transaction volumes and reduced losses from fraud, as well as improved customer experience, according to the analysis. “The core elements of having a mass market-ready biometric payment card are that it can be compatible with the existing payments infrastructure, work in both contact and contactless mode, and function without the need for a battery or fixed power supply,” says Mr Løvestam. “Our unique technology platform is at the heart of this innovative mix.”

As work progresses among banks and card manufacturers to develop biometric payment cards in collaboration with Zwipe, biometric sensor manufacturers see the huge opportunity on offer. Faced with increasing competition and price pressure in the mobile phone marketplace, they have refocused their efforts to offer sophisticated sensors for payment cards.

“For all parts of the payments ecosystem, the value proposition of biometric payment cards is simple: eliminating the unnecessary trade-off between convenience and security. Banks, card issuers and retailers can see how these cards will further cement such confidence,” says Mr Løvestam.

There is also the opportunity for banks and card firms to build more sophisticated custom products, a particularly important aspect in developed markets where differentiation is evermore important.

Examples of this already exist, with challenger banks in Europe developing services that combine personalised banking with unique cards that consumers can pick and choose themselves, and each has different costs and pricing models.

Meanwhile, in developing markets the fast growth of cards offers a major opportunity to leapfrog older cards and move straight to biometric technology, similar to systems already widely used by governments to deliver services more efficiently.

Competition among banks and card issuers has never been more intense, and biometrics offers a strong route to success. And with banks increasingly moving away from physical branches, making the most of consumer touchpoints with improved experiences has ever higher importance. Biometric payment cards offer a resilient system that can enable card issuers to establish a top-of-wallet, top-of-mind position among consumers.

To find out how biometrics enable fast, secure, high-value contactless card payment please visit zwipe.com