The relationship between banks and fintechs has evolved significantly over the last two decades. Disruption is increasingly giving way to collaboration, moving the industry past the now outdated narrative that pitted new entrants directly against incumbents.

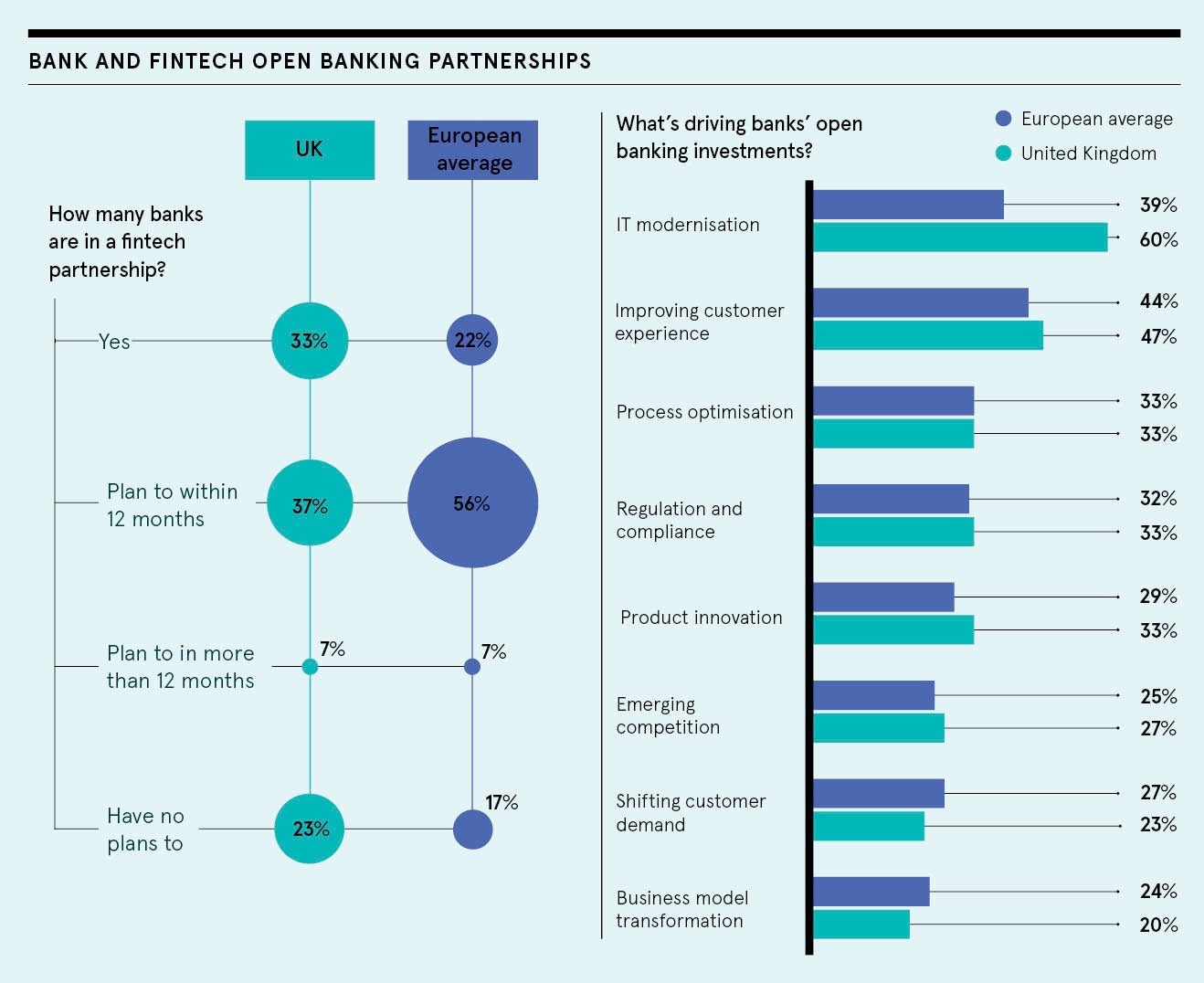

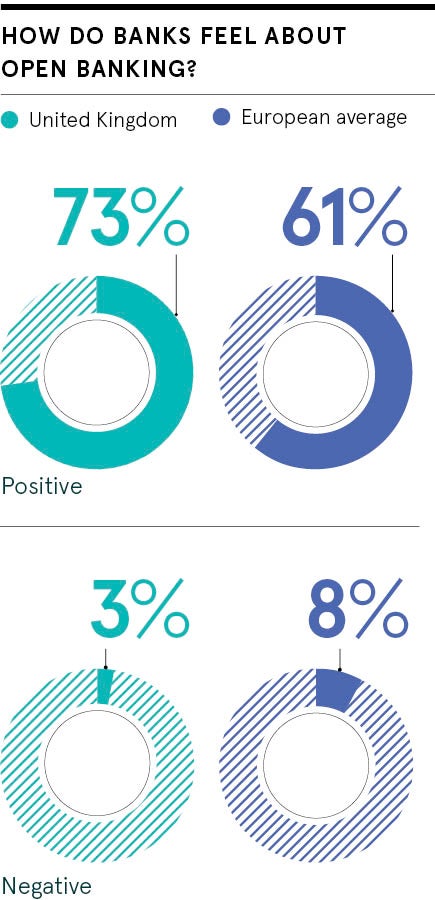

Banks are not only now partnering with fintechs, but also fostering them through accelerator programmes and venture arms, while the UK leads the way in open banking to facilitate valuable collaborations. In a study by Tink earlier this year, three quarters of UK financial executives had a positive attitude to open banking, compared to 48 per cent in 2019.

Banks rarely step into the API (application programming interface) economy to power emerging use-cases in the ways fintechs do. Yet, while fintechs are often born with agility and a pace of innovation that banks struggle to emulate, banks have something fintechs know will take them a long time to achieve: trust built over decades or even centuries.

Trust capital resides in large institutions, as does vast behavioural data around customers, presenting a strong incentive for fintechs to partner. Recognition of their complementary qualities has brought a new dimension to the classic build-versus-buy conundrum that banks have long deliberated.

“It’s a very important decision, because banks will live with the consequences of that decision for quite some time,” says Rafa Plantier, country manager, UK and Ireland, at Tink, which is powering the new world of finance by allowing banks to quickly build smart and personalised financial services.

“Banks used to do everything, but have been gradually outsourcing more things over the last 20 years. They are largely designed to work on projects and once a project is complete, those resources come back to do something else. That’s fundamentally different to fintechs, which have highly specialised, small and sprawling teams who take care of more narrowly focused engineering problems.

“While a bank will typically have a team who looks after all digital channels, fintechs work at a much more granular level, looking at things like onboarding conversion. Banks will see mortgages as a product. Fintechs will see the onboarding experience as a product. There is a very fundamental difference in how they approach technical problems. Institutions increasingly prefer to have it as a service so they can focus on their core business, fuelling partnerships for services powered by open banking.”

By establishing the right partnerships, banks can focus on what they do best, which is serving end-customers with their product vision

By enabling people to have the fundamental right to own their own data, open banking is equally important for society as it is for fintechs, financial institutions and how they ultimately work together.

“Open banking takes what is available in the high end of finance and brings it to the masses,” says Plantier. “Just like a developed treasury knows where every single pound resides, people will one day be able to see every single piece of their financial puzzle in one place in real time and across all financial institutions in Europe and soon globally. They will have the ability to share that information and move funds by simply granting consent. We are already there for most of the ‘transactional’ assets – current and payment accounts – and are now moving on to include high-value, low-frequency financial assets, like mortgages, pensions

and investments.”

Founded eight years ago, Tink has been trailblazing the open banking path. As Europe’s leading open banking platform, Tink enables banks, fintechs and startups to develop data-driven financial services.

Through one API, Tink allows customers to access aggregated financial data, initiate payments, enrich transactions and build personal finance management tools. The open banking platform connects to more than 3,400 banks, reaching over 250 million bank customers across Europe. Tink’s technology is transforming customer experiences across Europe, enabling businesses to help their customers make smarter financial decisions.

“Early on in our trajectory, we won some of the largest partnerships that have been signed in this industry, including SEB, ABN AMRO, NatWest and BNP Paribas,” says Plantier. “We help our clients come to market with data-exchange applications, streamline their user experiences and help them take more valuable financial services to their customers.

“The data exchanged on these APIs, from the industry perspective, is quite raw. We make the data more readable for the end-user, but also more machine readable for our clients. By making sense of transactions from sources within the bank, as well as accounts held externally, a bank can get a single overview of a customer’s economy and create insights that are easily actioned by the user.

“In the future, I imagine every large British bank will ultimately have a handful of very large fintech partnerships. There are things happening in digital identity, consumer finance and payments, merchant acquiring and open banking that are advancing so rapidly on a technical level it would be very difficult for any leading bank to develop and then manage in-house. By establishing the right partnerships, banks can focus on what they do best, which is serving end-customers with their product vision.”

When NatWest wanted to integrate a new feature in its digital banking service, it gravitated towards a fintech to help do the job. The bank wanted to give its mobile app users a more frictionless, time-efficient and intelligent way of managing their money. That amounted to a spending feature that tracks and categorises customers’ spending habits and provides insights to help them meet their savings goals. Finding a partner that could align with its values was a priority and Tink’s “imagine, build and iterate” philosophy sealed the deal.

Since launching last November, the spending feature has empowered millions of NatWest’s customers to take control of their finances. Around 4.6 million customers use it on a consistent basis, approximately 53 per cent of the bank’s active mobile banking customer base. In July 2020, a personalised and actionable news feed was added to the app, which has delivered 6.8 million insights to customers, 1.6 million of which people have acted on to save money.

Wendy Redshaw, chief digital information officer at NatWest Retail Bank, says: “We look to partners to work with us collaboratively and bring in fresh perspectives. Tink brings a wealth of experience in open banking, personal finance management and getting insight from data, alongside deep connectivity. When you add that to what NatWest Group brings – more than 200 years of financial expertise, close relationships with customers and a deep understanding of their expectations – you get a cauldron of innovation that has real value.”

For more information please visit tink.com

Promoted by

The relationship between banks and fintechs has evolved significantly over the last two decades. Disruption is increasingly giving way to collaboration, moving the industry past the now outdated narrative that pitted new entrants directly against incumbents.

Banks are not only now partnering with fintechs, but also fostering them through accelerator programmes and venture arms, while the UK leads the way in open banking to facilitate valuable collaborations. In a study by Tink earlier this year, three quarters of UK financial executives had a positive attitude to open banking, compared to 48 per cent in 2019.

Banks rarely step into the API (application programming interface) economy to power emerging use-cases in the ways fintechs do. Yet, while fintechs are often born with agility and a pace of innovation that banks struggle to emulate, banks have something fintechs know will take them a long time to achieve: trust built over decades or even centuries.