Through leveraging machine-learning, countless business systems that once required a great deal of manual labour can be automated. For example, pioneering fintech startups are able to create effective systems from the ground up as they don’t face the same complex legacy systems that traditional financial institutions are hindered by.

These new systems have the potential to gain truly relevant insights into their existing customers and then provide a more timely and personalised service, especially in the world of finance.

Established banks and financial institutions are increasingly understanding the importance of both embracing technological solutions that can benefit their customers and ensuring they select the right partners to achieve a higher level of customer engagement and innovation, which has previously not been possible.

“The rise of innovative technologies in financial services provides a huge opportunity for fintech firms like us to work together in tandem with banks and large organisations, specifically around domains where there hasn’t been a lot of innovation, including financial advice and retirement planning,” says Fahd Rachidy, founder and chief executive of ABAKA, a fintech firm offering an AI-based enterprise platform that helps financial institutions power digital retirement advice and customer engagement solutions to their retail customers.

Even relatively simple product features can take many months and millions of pounds to implement at traditional banks due to their complicated existing technology and systems. The additional challenge of a complex organisational structure can slow down the speed of innovation too.

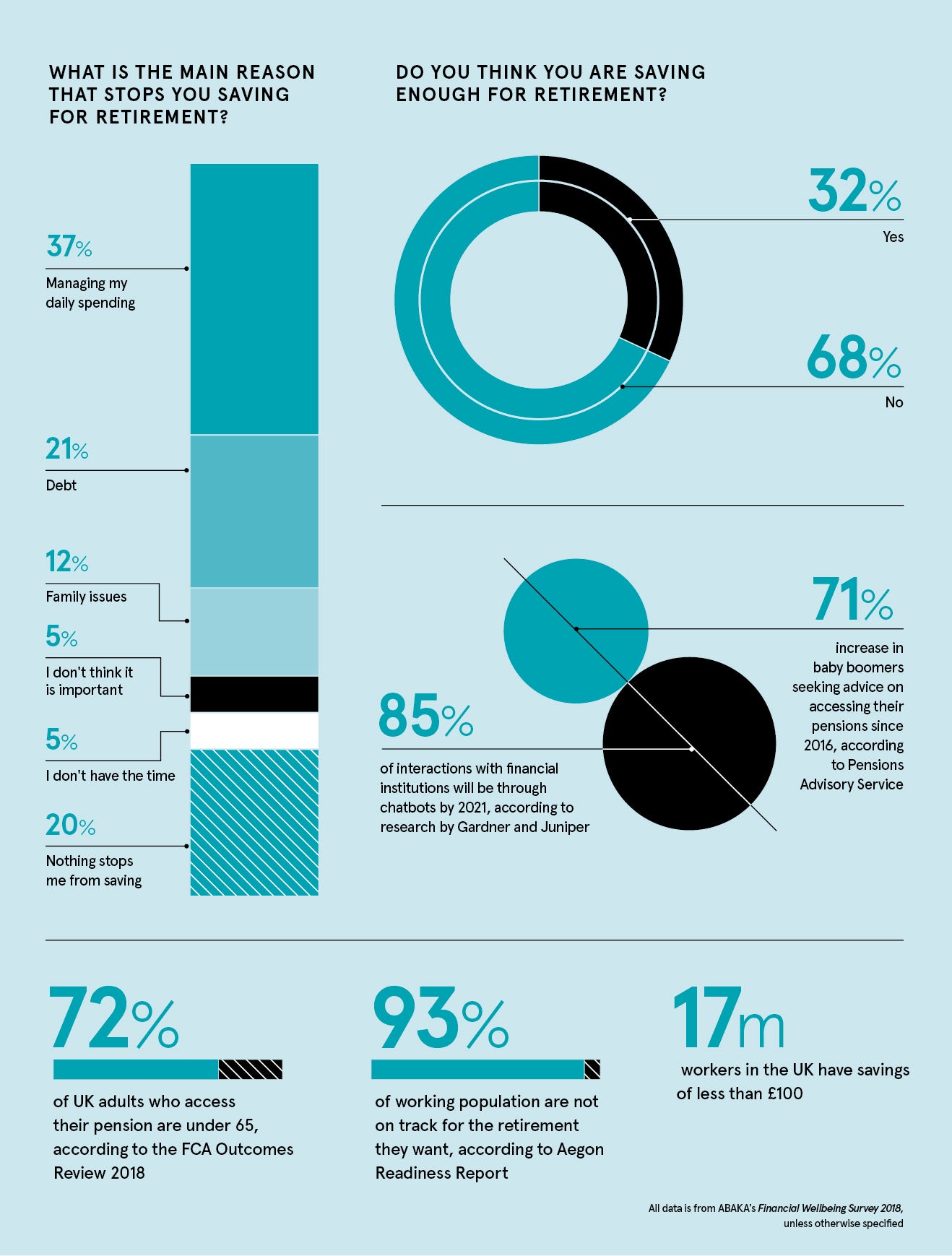

ABAKA is in an ideal position to support major financial institutions by offering digital advice powered by the UK’s first conversational AI on pensions, savings and investments

By collaborating with fintech firms, banks can utilise the more agile work process and ensure outdated ways of working can be bypassed to get things done quickly. Innovative fintech companies also draw skilled staff that are attracted to working in a less formal environment, which can help complement the internal bank talent when working on projects that require up-to-date technical skills.

“At a time when 30 million workers in the UK are at risk of running out of money in their retirement, our financial-advice-as-a-service solution can provide players in the finance industry the ability to offer help, which was recently only reserved to wealthy clients due to its high cost, to all customers at scale and at an affordable price,” says Mr Rachidy.

AI-powered financial-advice-as-a-service can help banks and other financial institutions improve how they educate, engage and empower their customers as they can use innovative communication methods to reach clients where they actually are most comfortable. For example, instead of forcing clients to use unintuitive web-based forms, customers can ask for advice and support through chat-based interfaces, easy-to-use devices like Amazon Alexa or conventional mobile texting.

Although banks traditionally hold a great deal of information about their users, it’s usually held in disparate silos that are extremely difficult to bring together. Thanks to the growing power of big data solutions, more customer data than ever can be analysed to extract actionable insights that enable banks to provide tailored and contextual advice to consumers to help coach them throughout their life and overall financial journey.

“With the open banking initiative, a number of technologies have been developed to allow banking institutions the ability to aggregate all the data from a client into a single, intuitive dashboard. For example, it’s not unusual for a person to have a current account with one bank, a savings account with another and a retirement account elsewhere. Before open banking, this often resulted in banks seeing a very fragmented picture of their customers finances, especially around retirement pots where customers can have several different savings accounts of this type,” says Mr Rachidy.

As the pension industry as a whole has done very little in recent decades to create a more intuitive and engaging user experience, ABAKA is in an ideal position to support major financial institutions by offering digital advice powered by the UK’s first conversational AI on pensions savings and investments.

“As opposed to most of the providers in the fintech space, whether it is in financial management or savings, we’re not providing information direct to consumers, we’re only providing our services directly to financial institutions. What we provide is a unique way to deliver digital advice on the topic that is of increasing importance, retirement advice,” says Mr Rachidy.

For a long time, the pensions landscape in the UK has been hard to navigate for many consumers who just don’t have the time or knowledge to seek out the best solutions for their individual circumstances. By offering ABAKA’s solution, financial institutions can support a revolution in how people retire and enable their clients to gain personalised advice that will help them plan their retirement journey as effectively as possible.

Most people are not saving enough for their retirement and are urgently looking for a simple solution that allows them to navigate an extremely complex industry. Unfortunately, many providers still rely on paper-based manual processes and don’t have the capacity to offer this type of product to their clients, unless they partner with innovative fintech firms such as ABAKA.

The financial-advice-as-a-service solution they’ve developed enables big financial institutions to leverage their trust and credibility, alongside the innovative user experience offered by ABAKA.

“ABAKA is in a very unique position as the only fintech firm in the UK that is able to provide an AI-backed conversational digital advice service that really helps to facilitate both traditional players and new market participants in creating customer journeys and delivering experiences, which are a lot more exciting than they’ve been doing for the past 30 years,” Mr Rachidy concludes.

For more information please visit www.abaka.me