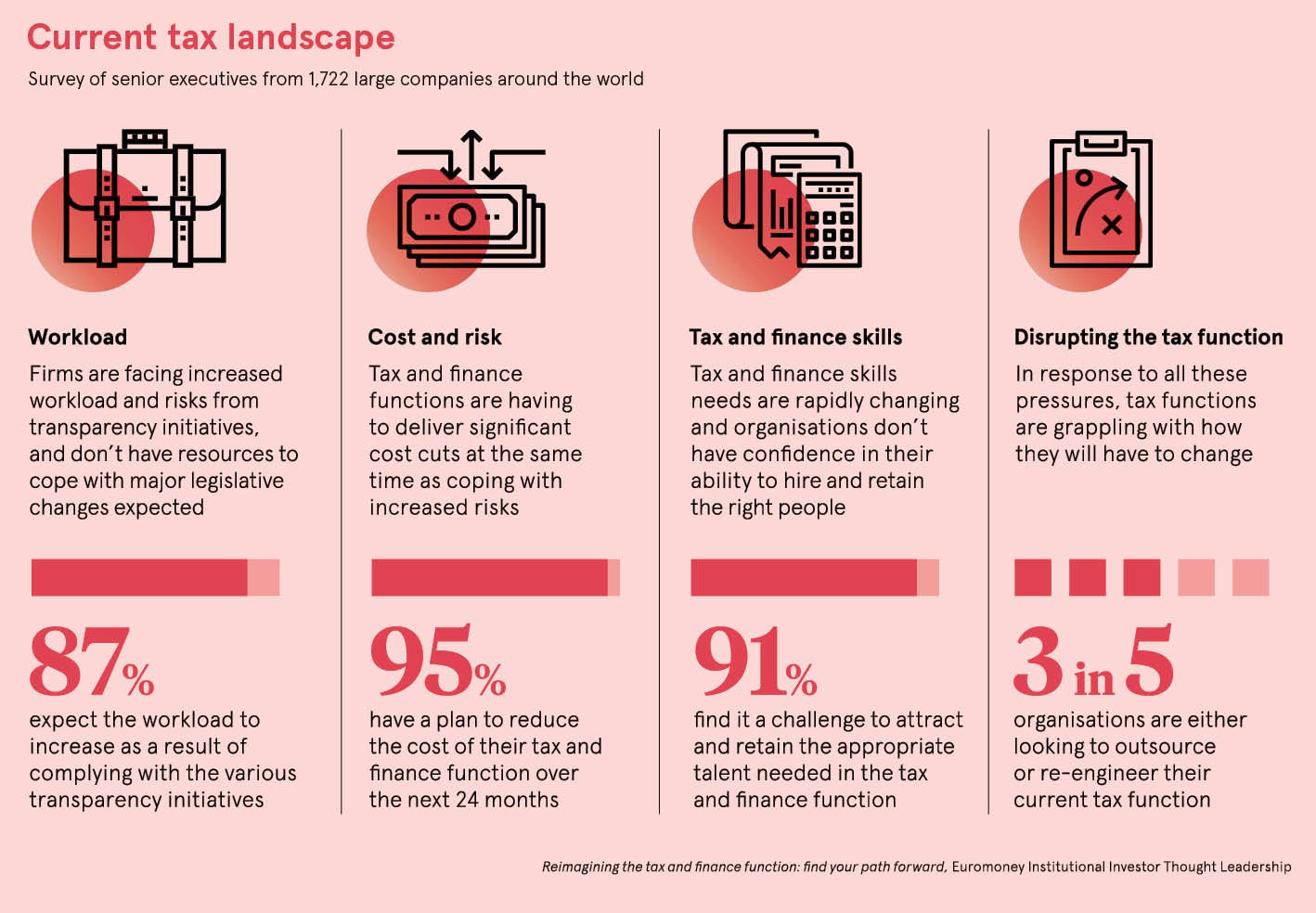

Advances in artificial intelligence (AI) in recent months, combined with increasing volumes of data and falling technology costs, are radically transforming the world of business. A survey conducted by EY with Forbes Insights shows 66 per cent of global companies are investing upwards of £4 million in analytics software and 78 per cent agree that analytics are changing the nature of competitive advantage. Leading companies reported a significant shift in their ability to meet competitive challenges by using data.

Advances in artificial intelligence (AI) in recent months, combined with increasing volumes of data and falling technology costs, are radically transforming the world of business. A survey conducted by EY with Forbes Insights shows 66 per cent of global companies are investing upwards of £4 million in analytics software and 78 per cent agree that analytics are changing the nature of competitive advantage. Leading companies reported a significant shift in their ability to meet competitive challenges by using data.

The impact of AI on finance functions is well documented, but its ability to unlock value in today’s tax function less so. Nevertheless, its impacts can be just as dramatic. Machine-learning software, a form of AI, can read thousands of lines of business transactions and instantly assess whether an item of expenditure is tax deductible. Where once armies of tax accountants trawled through corporate accounts to work out tax liabilities, a single machine can do this work in seconds with improved accuracy and consistency.

Notwithstanding the impressive results of putting AI to work in tax, the businesses in our survey said they encourage data analysis to be carried out by someone who knows the organisation and is familiar with the business objectives. This highlights the importance of human oversight of AI processes and data analytics.

As a result, the introduction of AI is triggering a rethink of the responsibilities of the tax function and, by extension, those of finance departments in businesses. It is also fundamentally changing the role of the tax professional, freeing them from repetitive tasks to concentrate on higher-end strategic business partnering.

“Accounting and compliance work will be changed irrevocably by adopting these technologies,” says Charles Brayne, chief tax innovation officer at EY. “In common with other global organisations, we are going through a process of looking at our business and asking how we can apply machine-learning and AI in different areas. I foresee accounting compliance and diligence work, risk management and tax review being almost entirely automated, data driven or machine driven.”

As an example, tax compliance (be that corporate tax, VAT or employment taxes) for a business involves going through lists of hundreds of thousands of items of expenditure, from marketing costs to travel expenses, then deciding which items to tax effect. This is a huge volume of work for tax professionals to carry out. It requires deep knowledge of tax law and the ability to make informed judgments. The process is open to error given the sheer complexity and repetitive nature of the work.

Search tools and rule-based systems can speed up the process. If a description of a transaction contains a certain keyword, for example, it is automatically assigned to a tax category. However, it is impossible to capture the full complexities of tax law by simply setting up such a system.

This is where machine-learning approaches, such as text classification, are reshaping tax practice and is the basis of a new tool we have created at EY called the Automated Ledger Review Tool, or ALeRT. It is a machine-learning system that infers tax rules from data with which it is presented rather than being explicitly taught them.

ALeRT offers great opportunities for directing tax professionals to where their judgement is most needed

ALeRT is first shown “training data” from which it learns how the descriptions of transactions relate to tax treatment. It is language and alphabet agnostic, but it is data that has already been labelled or categorised by a human. For example, it could be a previous year’s accounts, where each transaction, such as an item of marketing expenditure or a travel expense, is marked up as being tax deductible or not. The machine figures out which features or words in the description help it to discriminate between the different categories. When it has observed certain patterns of words many times and in each case the answer was always “deductible”, it learns that whenever it sees a similar combination of words and letters, the answer should again be “tax deductible”.

Training is a vital stage in creating a machine-learning system. Before letting ALeRT loose on live corporate data, its accuracy, along with other key performance metrics, are validated against other training data. This is another essential feature of ALeRT; it states the confidence it has in every one of its conclusions and whether or not it is confused. Scrutinising these outputs is where the human mind and the tax professional’s craft are brought back into the process, and where true business advantage lies.

ALeRT offers great opportunities for directing tax professionals to where their judgment is most needed, as there may be just 200 out of 10,000 that merit a human review. Our experience of using ALeRT suggests that to create value from big data, you need to analyse, review and act on data findings intelligently, not apply them blindly.

A further benefit of AI and machine-learning lies in its accuracy. The machine is deterministic, so when it sees a description and gives a category, it replicates this exactly for each example. Humans are not so consistent, so there is a greatly improved consistency of output. The risk associated with transaction analysis therefore goes down as a result of using this technology. This can save businesses money as they often err on the side of caution and miss out on full tax reliefs due to their complexity.

According to Harvey Lewis, chief data scientist for tax, technology and transformation at EY, the growing use of AI and machine-learning means tax professionals will require a broader set of skills. “They will need their tax training and expertise, but they will also need other skills. They’ll have to understand how the software works and they will need to develop the art of storytelling and giving insights to clients about the data. The upshot of AI is that their skillsets will start to expand rather than contract. Businesses are realising that success in AI depends on a strong focus on people,” says Dr Lewis.

EY is looking at greater use of AI in future, for instance it is prototyping a chatbot that can answer questions about taxation from clients. Tax accounting will undergo huge changes over coming years with the application of AI. This will bring broad benefits to clients, to consultancies and to the accountants themselves.

For more information, please visit EY.COM/UK/ALERT

ALeRT offers great opportunities for directing tax professionals to where their judgement is most needed